403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Solid UK Jobs Report Will Keep Bank Of England Moving Slowly On Rates

(MENAFN- ING)

The fall in the unemployment rate looks weird

Source: Bank of England Decision Maker Panel Wage growth should fall but the hawks are worried

Having cut rates for the first time this month, the Bank of England is facing the question of how rapid and how far rate cuts need to go over the next few months. And on the face of it, there's nothing in the latest UK jobs data that's likely to speed things up. A pause at September's meeting looks likely, before rate cuts resume in November.

Curiously, these latest numbers show the unemployment rate is down by two-tenths of a percentage point to 4.2%, against expectations of a rise. That's particularly striking given that this is based on three-month moving averages, which means it tends to be less volatile. This will only heighten the BoE's scepticism of the data and its reliability, given the well-publicised issues with response rates and potential bias in the survey. And in any case, the Bank had felt the jobs market was a bit stronger than the headline figures had been suggesting, so if anything this latest drop in the unemployment rate helps vindicate that view.

If unemployment is indeed less worrisome, then that will only increase the Bank's wariness of wage growth. This is still proving much stickier than many had expected. And while private sector regular pay growth is down to 5.2% in the latest data, this is largely down to base effects – or in other words, it tells us more about a sharp rise in pay this time last year. The latest run of month-on-month numbers – a better gauge of the current momentum in pay – still point to stubborn annualised rates of growth of around 5-6%.

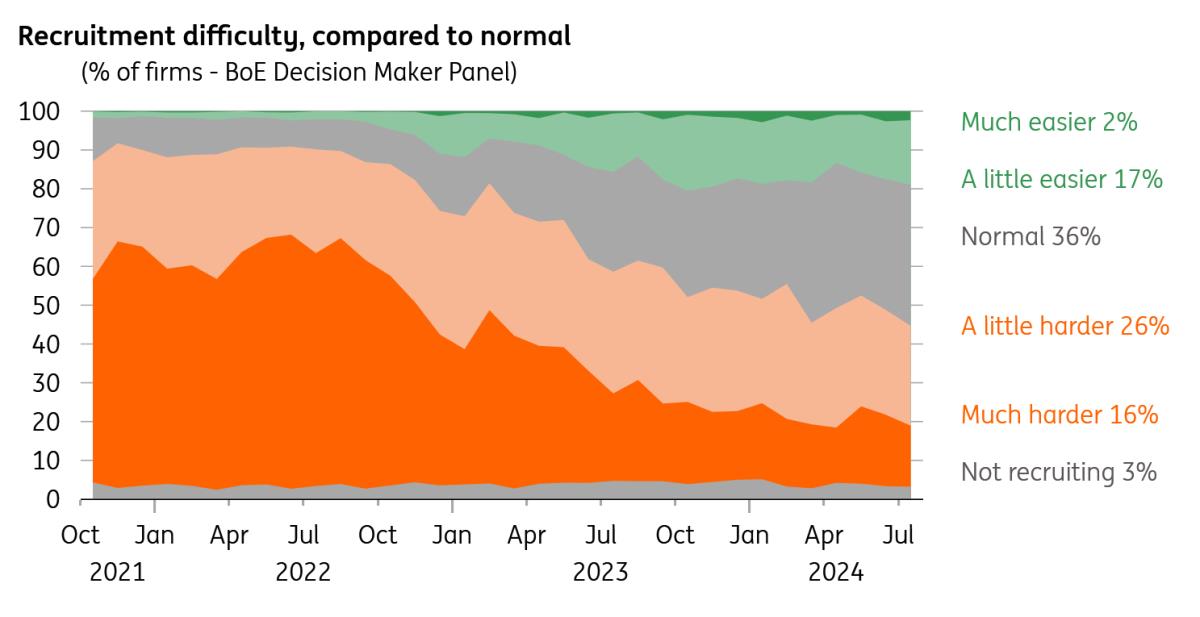

Bank of England survey shows recruitment difficulties have easedSource: Bank of England Decision Maker Panel Wage growth should fall but the hawks are worried

On paper, wage growth should ease as the year wears on, not only because actual inflation is lower, but also because the number of job vacancies continues to fall.

But the Bank's hawks are worried that wage growth will continue to prove stickier than the textbooks suggest. They argue that the ability of workers to recoup some of their lost disposable incomes of recent years is greater than it was pre-Covid. Catherine Mann, perhaps the committee's most hawkish member, told the Financial Times this week that she's worried recent high rates of pay growth for low-income workers could translate into faster growth higher up the pay scales.

These are valid concerns, but in an economy where formal wage negotiations or collective bargaining is relatively unusual, the jobs market needs to be sufficiently tight for those things to unfold. And away from the unemployment rate, there are plenty of signs that the jobs market has cooled down. The Bank's own surveys show that recruitment difficulties have eased considerably over the past year or two, and the expected rate of wage growth among corporates is down to 4% from 5.5% at the start of the year.

Today's data will do little to shift this debate among committee members. In the short term, we think the stickiness in wage growth will keep the Bank moving cautiously on rate cuts. But assuming there is further progress on both that and services inflation over the next few months, we think the Bank will accelerate the pace of cuts beyond November. We expect Bank Rate to fall to 3.25% by this time next year.

Author:James Smith

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment