403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Korea: Industrial Production Rebounded While Construction And Retail Sales Weakened In February

| 3.1% | Industrial Production %MoM, sa |

| Higher than expected |

All industry production rose 1.3% month-on-month sa in February (vs 0.4% in January). Manufacturing and service activity advanced, partially offset by the decline in construction. Together with the latest survey and other hard data, we expect manufacturing to lead the growth, while construction and consumption will weaken further in the near future. Overall GDP growth for the current quarter is expected to moderate slightly to 0.5% quarter-on-quarter sa from 0.6% in the fourth quarter of 2023. Our main concern is that the growth driver is quite narrowly focused on semicondcuctors only. And excluding AI demand, overall global demand is cooling, especially as we see signs of a slowdown in car production, which was a backbone of growth last year.

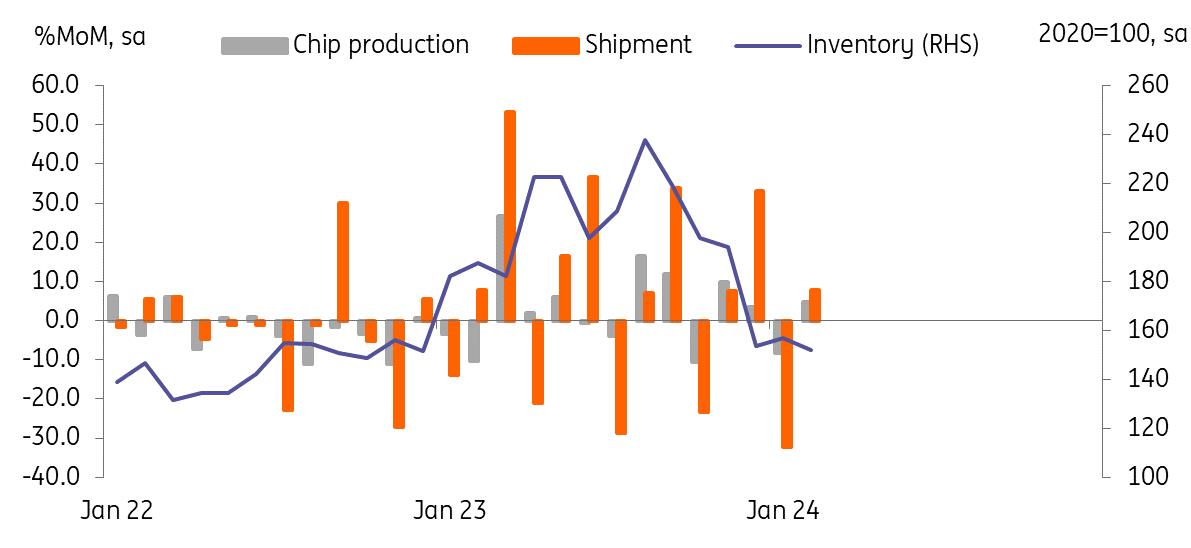

Semiconductor output grew strongly in FebruaryIndustrial production increased 3.1% MoM sa in February, more than offsetting the previous two months' declines, and it was stronger than the market consensus of a 0.5% gain. Semiconductors (4.8%) and related equipment (10.3%) rose the most while telecommunication (-10.2%) and video/audio equipment (-7.6%) declined. Another strong point was that inventory for semiconductors continued to fall, suggesting that semiconductor production is likely to remain firm with a favourable inventory restocking cycle.

Semiconductors rose firmly in February

Source: CEIC

Service activity also rebounded with a 0.7% MoM gain February (vs -0.2% in January). We believe that the Lunar New Year holiday may have boosted accommodation/restaurant (5.0%) and transportation services (1.6%).

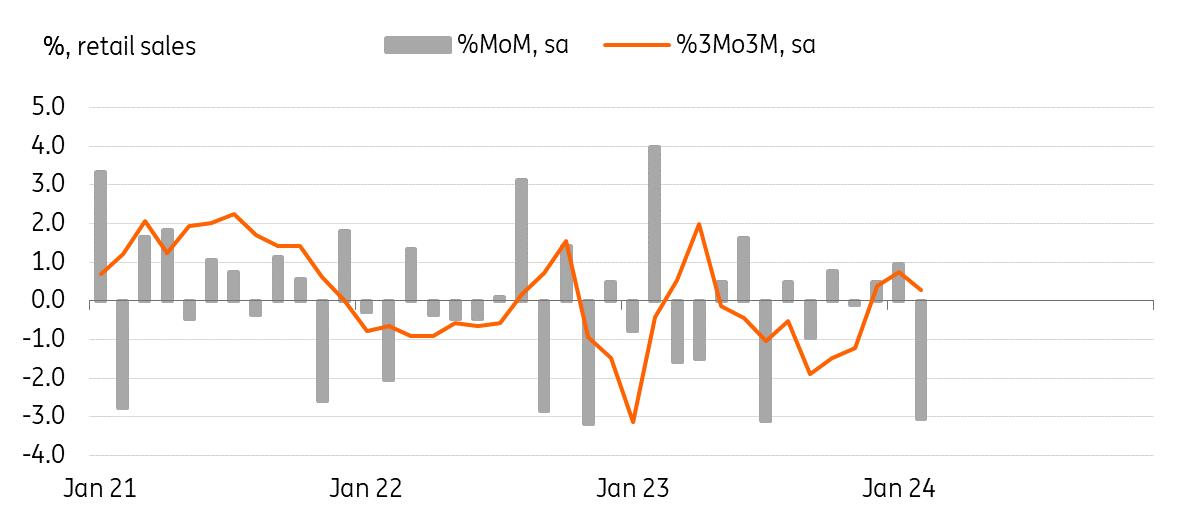

Retail sales and investment weakened in FebruaryRetail sales plunged -3.1% MoM sa in February (vs 1.0% in January). As we have long argued that high inflation and debt servicing burdens would hurt household consumption, we believe that sluggish consumption will continue. In addition, several consumption stimulus packages expired at the end of last year, which should also contribute to weak retail sales this year.

As for investment, it was a bit mixed. Facility investment jumped 10.3% MoM sa in February as chip-making equipment investment (6.0%) rose firmly, but monthly volatile vessels investment (23.8%) boosted the headline figure. Thus, we think the underlying trend of facility investment should have been more modest than the headline suggested. The biggest concern for investment was construction. Given the sluggish real-estate market and ongoing project financing issues, construction completion declined -1.9% MoM sa. With forward-looking orders data remaining in a contraction zone, we don't expect contstruction to rebound anytime soon.

Retail sales declined in February

Source: CEIC Bank of Korea watch

In our view, today's data was fairly neutral to the BoK's policy decision. Manufacturing activity was stronger than expected but retail sales and construction showed domestic growth continued to slow. Given that overall growth is determined by exports rather than domestic demand, the Bank of Korea's concerns shouldn't deviate too much from its current projection. However, we found that there are more clear signs of a slowdown in consumption and investment, and thus the Bank of Korea will shift its policy focus to domestic growth conditions later this year.

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment