403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Cooling UK Jobs Market Bolsters Chances Of Near-Term Rate Cut

(MENAFN- ING)

Macrobond, ING calculations

The UK jobs market is cooling and that's gradually translating into lower wage growth. This is the main takeaway from the latest UK labour market figures and is broadly consistent with the messaging from the Bank of England last week.

It's worth remembering from the outset that the headline jobs figures – employment, unemployment and inactivity – are still believed to be pretty unreliable, owing to an ongoing fall in the survey's response rate. The unemployment rate notched up to 4.3%, but it's hard to say how much weight we should really be putting on that (potentially not a lot).

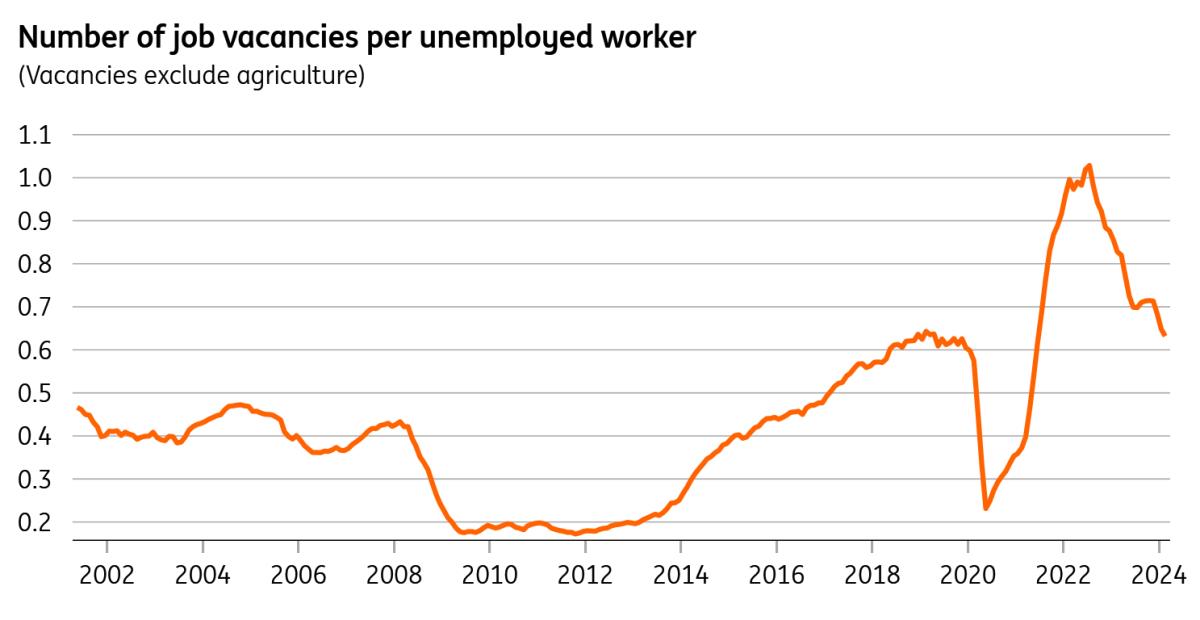

But it's a message that's echoed elsewhere in the report. Vacancies are down further and if we look at these job openings as a ratio with the number of unemployed workers, that is now within spitting distance of the 2019 average. And if we look at an alternative measure of employment using official payroll data, then that has been flat to slightly negative so far this year.

Vacancy-to-unemployment ratio back at pre-Covid levelsMacrobond, ING calculations

That easing does appear to be resulting in some gradual decline in wage growth. Admittedly, the headline regular pay measure came in a tad above consensus this month – but that appears to be accounted for by the public sector, which the BoE has signalled is of lesser significance to monetary policy decisions right now. Private sector pay is down to 5.9% in annual terms from 8.4% last summer.

Even here though, there are concerns about reliability. It seems that wage growth was artificially boosted in 2023, after one-off cost of living payments were wrongly accounted for as permanent increases in pay. Those payments weren't repeated this winter, and it seems that this may now be exaggerating the fall in wage growth. And while the pay data doesn't share those issues of dwindling sample sizes, it is ultimately presented as a worker average and therefore it's possible the issues in the labour force survey are indirectly injecting some extra volatility.

For those reasons, the Bank is telling us that it's now putting less weight on wage growth than it was a few months ago. That means next week's services inflation figures are going to be the single most important determinant of whether the BoE cuts rates in June. Services CPI will fall back in year-on-year terms, but we think the risk is that this fall will be slightly less dramatic than the BoE expects. If we're right, then that slightly favours August over June as the start date for rate cuts. But in all honesty, we think it's looking pretty 50-50 right now.

Author:James Smith

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment