403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Concrete And Cement Market To Expand By USD 438.3 Billion From 2024-2028, Driven By Construction Growth, AI's Impact On Market Dynamics- Technavio Report

| Concrete And Cement Market Scope |

|

| Report Coverage |

Details |

| Base year |

2023 |

| Historic period |

2018 - 2022 |

| Forecast period |

2024-2028 |

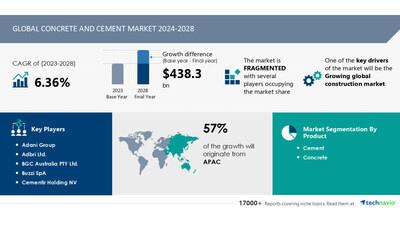

| Growth momentum & CAGR |

Accelerate at a CAGR of 6.36% |

| Market growth 2024-2028 |

USD 438.3 billion |

| Market structure |

Fragmented |

| YoY growth 2022-2023 (%) |

5.98 |

| Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

| Performing market contribution |

APAC at 57% |

| Key countries |

China, India, US, Russia, and Indonesia |

| Key companies profiled |

Adani Group, Adbri Ltd., BGC Australia PTY Ltd., Buzzi SpA, Cementir Holding NV, CEMEX SAB de CV, China National Building Material Co. Ltd., CRH Plc, FCC SA, Fletcher Building Ltd., Heidelberg Materials AG, Holcim Ltd., JK Cement Ltd, Mitsubishi Cement Corp., NIPPON STEEL CEMENT Co Ltd, PPC Ltd., Sumitomo Osaka Cement Co. Ltd., Taiheiyo Cement Corp., Titan Cement Group, and UltraTech Cement Ltd. |

Market Driver

The economic advancements in countries like India, Vietnam, Malaysia, China, and Qatar have resulted in a significant increase in consumer disposable incomes and rapid urbanization. This economic growth has led to a rise in purchasing power, which in turn, will boost spending on residential and non-residential infrastructure projects. According to The World Bank Group, China's GDP per capita grew from USD9,976.68 in 2018 to USD10,261.68 in 2019, while India's GDP per capita increased from USD2,005.86 in 2018 to USD2,099.60 in 2019. The global construction market is expected to grow due to the increasing demand for infrastructure projects in these regions. Concrete is a popular choice for construction due to its ability to reduce shrinkage and cracking tendencies of cement, increase resistance to weathering, and minimize volume change from drying. With an anticipated urban population growth from 4.19 billion in 2018 to 4.27 billion in 2019 and an additional 2 billion people expected to live in urban and semi-urban areas by 2050, the demand for concrete and cement is poised to increase significantly.

The concrete and cement market is experiencing significant trends in sustainable construction practices, infrastructure resilience, and digitalization. Advanced concrete solutions, such as smart concrete and rapid-hardening cement, are gaining popularity for their operational efficiencies and improved load-bearing capacity. Sustainable cement manufacturing processes, including the use of alternative fuels and raw materials, are also on the rise. Infrastructure projects demand high resilience, leading to increased demand for fire-resistant, acoustically improved, and high-strength concrete. Digitalization in construction is revolutionizing the industry with remote monitoring, predictive maintenance, and automation of processes like grinding mills and kilns. Cement and concrete remain essential building blocks for residential and non-residential construction. Aggregate, sand, gravel, concrete pipes, bricks, and paving blocks are integral components of these structures. Low-interest loans and government incentives are driving investment in bridge girders, wall panels, and other large-scale construction projects. Cement manufacturers continue to innovate with products like low-heat cement, white cement, hydrophobic cement, and colored cement to meet diverse customer needs.

Explore a 360° Analysis of the Market: Unveil the Impact of AI. For complete insights- Request Sample!

Market

Challenges

-

The construction industry relies heavily on various building materials, including cement, concrete, steel, bricks, and aggregates. Cement and steel account for approximately 19% of the total construction cost each. The availability and pricing of these materials can significantly impact construction costs, as a rise in the price of one material increases the overall cost. In Europe, economically stable countries like the UK, France, and Germany can manage price hikes. However, volatile economic conditions in countries like Nigeria and Namibia make it challenging to cope with price increases. White cement, a premium type of cement, is popular for its clean and consistent designs. However, its production requires 40% more energy than regular gray cement, leading to higher operating costs. High taxes and manufacturing site costs in developing countries like India further increase white cement prices, potentially hindering the growth of the global white cement market and, consequently, the concrete and cement market.

The cement and concrete market faces several challenges in supplying essential building materials for urban development. Aggregate sources, including sand, gravel, and crushed stone, can impact availability and pricing. Manufacturing concrete pipes, bricks, paving blocks, and other structural components requires a consistent supply of cement. Cement production is energy-intensive, relying heavily on coal supply and the burning process. International standards for concrete quality, such as those for ready-mix concrete and batch plants, must be met. Urban centers, particularly those with high-rise buildings and infrastructure investments, have increasing demands for concrete and cement. Threats include regulatory standards and competition from alternative building materials. Drivers include the construction boom, infrastructure investments, and urbanization in developing markets. Opportunities lie in the production of specialized cements like rapid hardening, low heat, white, hydrophobic, colored, and Portland pozzolana cement. Wholesalers and donations can help bridge gaps in supply and demand. However, the industry must address energy efficiency and sustainability concerns to remain competitive.

For more insights on driver and challenges

-

Request a

sample report!

This concrete and cement market report extensively covers market segmentation by

-

1.1 Cement

1.2 Concrete

-

2.1 Residential

2.2 Non-residential

-

3.1 APAC

3.2 Europe

3.3 North America

3.4 South America

3.5 Middle East and Africa

1.1

Cement-

The concrete and cement market is a significant sector in the construction industry. Producers manufacture and sell cement, which is the primary ingredient in making concrete. Cement is used extensively in various construction projects, including residential, commercial, and infrastructure developments. Demand for concrete and cement remains strong due to ongoing construction activities worldwide. Market growth is driven by population growth, urbanization, and infrastructure development projects. Producers focus on increasing production capacity and improving efficiency to meet demand. Exports also contribute to market growth. The market is competitive, with major players including LafargeHolcim, Cemex, and HeidelbergCement.

For more information on market segmentation with geographical analysis including forecast (2024-2028) and historic data (2017-2021) - Download a Sample Report

Research Analysis

The Concrete and Cement market is a significant player in the construction industry, supplying essential raw materials for various applications. Sand and gravel are the primary sources of aggregate, while concrete pipes, bricks, paving blocks, and buildings are common end-use products. Ready-mix concrete and batch plants facilitate the production of concrete on-site, with various types such as rapid hardening cement, low heat cement, white cement, hydrophobic cement, colored cement, and Portland pozzolana cement catering to diverse needs. Urban centers, residential and commercial buildings, urban areas, high-rise buildings, and developing markets are major consumers. Infrastructure investments, regulatory standards, and sustainable construction practices are key drivers, while threats include competition from alternative materials and regulatory challenges. Planned skyscrapers, construction boom, and infrastructure resilience offer opportunities. Digitalization in construction and advanced concrete technologies are shaping the future of the market. Steel beams and other construction materials complement the use of concrete and cement.

Market Research Overview

Cement and concrete are essential building materials used in various structures, including residential and commercial buildings, infrastructure, and urban amenities. The production of cement involves the grinding of raw materials like aggregate, sand, gravel, and coal, which is then burned at high temperatures in kilns to form clinker. This clinker is ground into cement in grinding mills. Concrete is made by mixing cement, water, and aggregate. Concrete pipes, bricks, paving blocks, and other concrete products are also produced using cement. Urban areas, particularly urban centers, are major consumers of cement and concrete due to the high demand for buildings, infrastructure, and other construction projects. The concrete industry faces several challenges, including energy-intensive production processes, regulatory standards, and threats from sustainable construction practices and digitalization in construction. However, there are also opportunities for growth through infrastructure investments, operational efficiencies, and the production of advanced concrete products like rapid-hardening, low-heat, white, hydrophobic, colored, and Portland pozzolana cement. Factories produce cement and concrete through batch plants, which mix and produce the concrete mixture on-site or at the factory. Ready-mix concrete is also available from wholesalers for delivery to construction sites. Cement manufacturing involves significant investments in capital-intensive equipment like kilns and grinding mills, which require a steady supply of coal. The industry is also under pressure to improve load-bearing capacity, fire resistance, and acoustics in concrete structures while reducing the environmental impact of cement production. In developing markets, the construction boom presents significant opportunities for growth, while in developed markets, the focus is on infrastructure investments, regulatory standards, and sustainable construction practices. The industry is also adopting digitalization, including remote monitoring, predictive maintenance, and advanced concrete technologies, to improve operational efficiencies and reduce costs. Despite the challenges, the cement and concrete industry remains a vital contributor to the global construction sector, providing the foundation for buildings, infrastructure, and urban development.

Table of Contents:

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation

-

Product

-

Cement

Concrete

-

Residential

Non-residential

-

APAC

Europe

North America

South America

Middle East And Africa

7

Customer Landscape

8 Geographic Landscape

9 Drivers, Challenges, and Trends

10 Company Landscape

11 Company Analysis

12 Appendix

About Technavio

Technavio is a leading global technology research and advisory company. Their research and analysis focuses on emerging market trends and provides actionable insights to help businesses identify market opportunities and develop effective strategies to optimize their market positions.

With over 500 specialized analysts, Technavio's report library consists of more than 17,000 reports and counting, covering 800 technologies, spanning across 50 countries. Their client base consists of enterprises of all sizes, including more than 100 Fortune 500 companies. This growing client base relies on Technavio's comprehensive coverage, extensive research, and actionable market insights to identify opportunities in existing and potential markets and assess their competitive positions within changing market scenarios.

Contacts

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email:

[email protected]

Website:

SOURCE Technavio

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment