Rates Spark: No Let Up For Now

Date

9/27/2023 4:12:23 AM

(MENAFN- ING) There is no let up in the upward pressure on rates. While risk sentiment is deteriorating further, we saw inflation swaps coming off their elevated levels as well. Are we finally getting

the medicine that was needed?

Bund asset swaps remained calm despite

wider sovereign

spreads and a lower collateral supply outlook

In this article Rates pressure remains, but risk sentiment is souring Today's events and

market view

Market rates continue to remain under pressure Rates pressure remains, but risk sentiment is souring

Following their rise at the start of the week, yields tested lower yesterday. But that rally proved short-lived, with the 10Y Bund yield ending the session above 2.8% again.

What remained of the day was a sense of risk-off again. Equities ending in the red and European sovereign spreads noticeably wider even when yield levels briefly dipped. The key spread of 10Y Italian bonds over the German Bund is now above 190bp, solidly back into the range that prevailed ahead of the summer. But the widening was not confined to Italy. We saw a widening in Greek and other periphery country spreads, though not quite as pronounced.

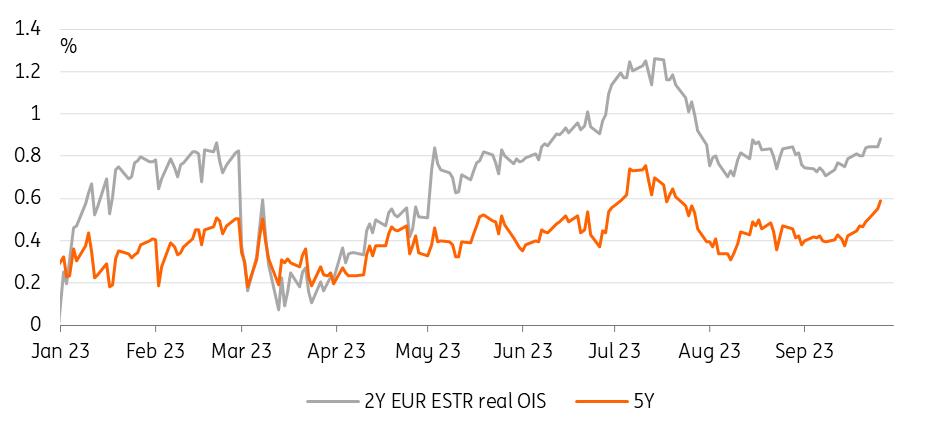

Perhaps it is the medicine that is needed. Real rates are on the rise again with the 5Y real ESTR OIS marching towards 0.6% – a level it had topped only briefly in July during this tightening cycle. Inflation swaps are coming off their highs, with the 5y5y inflation forward down another 2bp after Monday.

Perhaps more surprising against the backdrop of souring risk sentiment was the fact that Bund asset swap spreads (ASW) were little changed – typically, they are sensitive to risk-off. And even more notable as the German debt agency yesterday cut back the issuance targets for the fourth quarter by more than anticipated. Bond sales for the quarter were cut by €8 billion and Bubill sales by €23 billion.

There was only a very short-lived widening in the Bund ASWs on the lowered collateral supply prospects, but we have to acknowledge that the current conditions in markets for high-quality collateral appear rather benign judged by Bubills trading relatively inexpensive versus swaps. And going from a current Bubill outstanding stock of €155 billion to €148 billion by the end of the year as now pencilled into the new funding calendar is not a dramatic shift to prevailing conditions, even if the original plan was to bring the stock to €171 billion.

In terms of more direct impact, we also still have to wait for October when the Bundesbank ends remuneration of government deposits, which by the latest reading were around €38 billion at the end of last week. This could then still push into the collateral market. Note though that the debt agency itself has said its balances have already been shifted into the secured money market and are now close to zero.

Real rates are in the driving seat

Refinitiv, ING Today's events and market view

Yesterday's short-lived test lower shows that upward pressure on rates is maintained. For now, the calendars have held little to really change the picture, and the same may hold for today. Only the US durable goods orders are of note today. The eurozone will release money supply data.

Government bond primary markets will stay busier with a 10Y Bund tap out of Germany, a 50Y gilt reopening in the UK and later, a new 5Y note from the US Treasury alongside a 2Y floating rate note tap.

MENAFN27092023000222011065ID1107150075

Author:

Padhraic Garvey, CFA, Benjamin Schroeder

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.