403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Monitoring Turkey: Improving Outlook

(MENAFN- ING) Turkey: At a glance

ICE, Refinitiv, ING

- The Central Bank of Turkey's actions in March, including an unexpected and strong rate hike, a large set of macro-prudential measures and liquidity tightening have eased concerns about the disinflation priority, and contributed to supporting both local and foreign investors' confidence in TRY assets. These measures imply a tighter overall monetary stance than what is implied by the policy rate. Compared to February, consumer loan rates increased by 17.4pp to 76.4% (on a gradual declining path in the last two weeks), and the 3-month TRY deposit rate by 16.2pp to 68.1% (on a compounded basis). Residents' FX deposits have declined by US$6.6bn in the five weeks to 26 April, reversing some of US$10.4bn cumulative increase in the three weeks prior to the March hike in rates. Foreign flows to bonds have been positive in the last five weeks with a cumulative US$1.6bn, while inflows to stocks, and domestic banks' offshore FX swaps have picked up in recent weeks. While the CBT's gross reserves have been relatively flat in recent weeks, the net reserve position (excluding swaps) improved by a significant US$17.0bn (between 29 March-26 April). This implies that it prefers to reduce bank swaps to contain TRY liquidity created by this tool. Accordingly, the overnight repo rate remains close to the upper band of the interest rate corridor at 53%. April inflation, which was lower than the consensus, shows a continuing broad-based deterioration in price dynamics and confirms challenges to the disinflation process. While we still see the policy rate on hold until late 2024, the outlook implies that upside risks remain. The second inflation report of the year, to be released on 9 May, will provide further insight into the CBT's inflation forecast trajectory. After Fitch moved in March, S&P also upgraded Turkey's ratings to "B+" from "B" at the beginning of May. The agency stated that the coordination between monetary, fiscal, and income policy is set to improve, amid external rebalancing. Moody's, grading Turkey two notches below Fitch and S&P, may also move to upgrade at its scheduled review in July, in our view.

There is a consensus that 1Q GDP will likely be relatively strong on the back of the fiscal impulse and the minimum wage hike. However, following the surge in loan demand in the run-up to the local elections held at the end of March, the CBT imposed restrictions on TRY-denominated loans. Recent data shows that these restrictions led to a sharp slowdown in credit growth including a sharp decline in consumer credit card spending. Accordingly, growth is expected to lose momentum in 2Q and 3Q due to an erosion in purchasing power, with continuing pricing pressures and tightening financial conditions thanks to the CBT's actions in March. In fact the PMI, which was above the 50 threshold in February and March dropped below this level in April at 49.3 due to a sustained slowdown in new orders, leading to a renewed moderation of output. Overall, the PMI signalled a moderation of manufacturing though this is still marginal currently.

Real GDP (%YoY) and contributions (ppt) TurkStat, ING Accelerating industrial production in FebruaryCalendar-adjusted industrial production (IP) recorded an 11.5% year-on-year increase in February as earthquakes dampened production in the same month of last year. The seasonally- and calendar-adjusted index grew by 3.2% on a sequential basis at all-time high levels. and showed strength in economic activity ahead of March local elections. In the breakdown, while energy contracted by a mild -0.8% MoM, other groups managed to grow with capital goods recording the highest growth at 11.3% MoM, followed by nondurable (1.86% MoM) and durable (1.48% MoM) goods. The recovery in the manufacturing sector (3.8% MoM), on the other hand, was broad-based as 18 sectors out of 24 contributed positively. In the sectors, other transport equipment (dominated by defence industry products) provided the strongest contribution to manufacturing at 2.1ppt. All in all, the recovery strengthened in February, though this increase is likely to be temporary given the expected impact of the tightening measures taken in March.

IP vs PMI ICI, TurkStat, ING Retail sales maintained strength in FebruaryRetail sales volume on a calendar-adjusted basis increased by 25.1% YoY in February, showing an acceleration from the yearly performance a month ago (at 13.7% YoY) likely due to the impact of the small base last year, which was impacted by the earthquakes. The seasonally- and calendar-adjusted index, on the other hand, has remained strong and recorded the highest sequential growth since Mar-23 at 3.5% MoM. Retail sales, along with elevated consumption goods imports in February, imply continuing strength in domestic demand conditions. Among subgroups, non-food sales increased 4.9% MoM, which was the major driver followed by food (1.4% MoM) and automotive fuel sales (1.0% MoM). The highest sequential increase in non-food sales was observed in computers and telecommunications equipment. On the other hand, the (seasonally-adjusted) unemployment rate fell to 8.7% in February from 9% a month earlier, though the figure has been floating in an 8.6-9% range in the last five months. The composite measure of labour underutilisation, which is the sum of time-related underemployment, unemployment, and potential labour force, dropped by 1.9ppt in February on a sequential basis and fell to 24.5% down from 26.4%, the highest since Apr-21.

Retail sales vs consumer confidence TurkStat, ING No improvement in the underlying headline trendFollowing monthly inflation at 3.18% MoM, which was lower than the consensus, annual inflation turned out to be 69.8% YoY, up from 68.5% a month ago. The lower-than-expected monthly reading was mainly attributable to food prices, though core and services inflation remained elevated with a continuing broad-based deterioration in price dynamics. Accordingly, cumulative inflation in the first four months stood at 18.7% vs the 36% CBT forecast for this year. On a seasonally adjusted basis, after the spike in January, core inflation continued to decline, though remained elevated. The headline inflation trend, on the other hand, was unchanged at above 3%, thanks to the high trend in services, confirming the challenges for disinflation. As a result, monthly headline inflation (seasonally adjusted) was above CBT projections, which sees the seasonally-adjusted monthly inflation hovering below 4% on average in the first half of this year (around 3% except for January).

Inflation outlook (YoY%) TurkStat, ING Considerably narrower current account deficit in FebruaryThe current account in the second month of this year posted a deficit of US$3.3bn, better than the market consensus at US$3.7bn. In the breakdown, compared to the same month of last year, we see: i) a continuing decline in the gold trade deficit which was at US$0.7bn in Feb-24 vs US$3.4bn a year ago ii) a recovery in the net energy trade with a fall in deficit to US$4.4bn from US$5.8bn and iii) a turn in the core trade balance to a surplus of US$0.6bn from a slight deficit of US$0.9bn. On the capital account, net identified flows remained weak with a mere US$2.0bn of inflows following mild outflows a month ago. Errors and omissions outflows, which came back since September, were at US$5.0bn in February (amounting to US$17.4bn in the last 12 months). With the monthly c/a deficit and weak flow outlook, official reserves recorded a fall of US$6.2bn (after another US$6.2bn drop in January). Overall, the provisional customs data released by the Ministry of Trade reveal that the foreign trade deficit dropped by around 10% to US$7.5bn in March. The data implies continued improvement in external balances, though at a much lower pace after a sharp narrowing in the first two months of this year.

Current account (12M rolling, US$bn) CBT, ING Signs of spending cuts from the governmentDespite continued strength in direct and indirect tax collections, the March budget reflected a worsening in the deficit compared to the same month of last year due to the non-recurrence of CBT profit transfers this year and the acceleration in non-interest expenditures driven by personnel expenditures and current transfers. Accordingly, the budget posted a deficit of TRY209.0bn in March alone vs a TRY47.2bn deficit in the same month of last year, while the deficit for the last 12 months rose to TRY1,638bn (5.5% of GDP). In the new MTP, the budget deficit forecast for 2024 was at 6.4% of GDP. In the absence of restrictive measures, the budget deficit to GDP ratio is likely to increase further in the remainder of this year. According to recent news, Minister of Treasury and Finance Mehmet Şimsek has signalled that the government will take decisive steps regarding expenditure control in the public sector. As part of those actions: i) public institutions will not be allowed to buy new buildings as cost-saving measures will be implemented ii) there will be stricter rules for buying and leasing vehicles iii) the public procurement law will be amended, and procurement procedures will be updated in line with international standards.

Budget performance (% of GDP) Ministry of Treasury and Finance, ING CBT remains hawkish in AprilAt the April rate-setting meeting, the CBT kept the policy rate flat at 50% in line with the consensus and cited i) significant tightening in financial conditions and ii) lagged effects in monetary transmission as the major determinants of the decision. However, it has remained sensitive to the inflation outlook, emphasising that it is highly attentive to inflation risks. Accordingly, the bank restated that the“monetary policy stance will be tightened in case a significant and persistent deterioration in inflation outlook is foreseen”. This implies that it has kept the door open to additional hikes depending on inflation data. Additionally, the current level of policy interest rate will be maintained as long as needed as the bank reiterated two qualifiers to start cutting: i) a significant and sustained decline in the underlying trend of monthly inflation ii) a convergence of inflation expectations to the CBT's projected forecast range. Finally, the CBT reiterated the pledge for further macro-prudential moves“in case of unanticipated developments in credit growth and deposit rates”. After the MPC meeting, the CBT also increased the remuneration rates on the reserve requirements related to FX-protected deposits and TRY deposits. Higher remuneration rates should give banks more incentives to offer higher rates on locals' TRY deposits.

CBT funding (TRY bn) CBT, ING FX and rates outlookGiven the recent CBT's response in March with a number of tightening actions and hawkish stance, foreign interest in the lira has resumed. There are also efforts to tighten deposit interest rates which, in turn, are encouraging reverse dollarisation and reducing domestic demand by encouraging savings. Accordingly, with deposit rates on total lira deposits exceeding 60%, the share of TRY in the deposit base has been increasing again lately. The currency will likely remain supported in the period ahead.

In the April MPC statement, the CBT reiterated that services inflation is sticky and the domestic economy remains resilient. It has remained sensitive to the inflation outlook, emphasising that it is highly attentive to inflation risks. Accordingly, the bank retained a strong tightening bias and seems to be ready to hike further. Given that April inflation was at 68.5%, the ex-post real policy rate remains negative, while the ex-ante real policy rate is close to 15% (vs 12M inflation expectations at 35.2%). The rising inflation path in the near term is still a concern adversely impacting real returns.

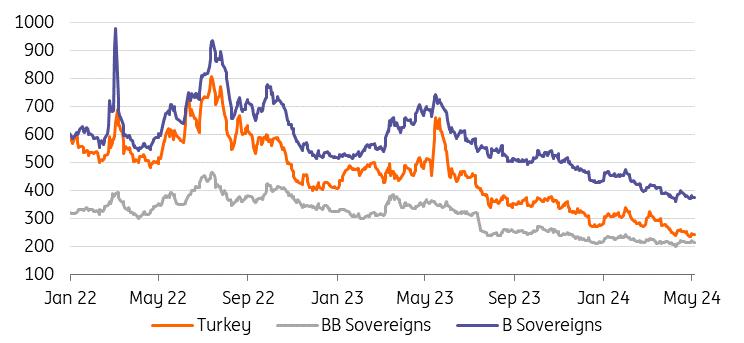

Local bond yields vs CBT funding rate Refinitiv, ING Sovereign credit: Rating momentum continuesS&P last week upgraded Turkey's sovereign credit rating to B+, maintaining a positive outlook. This brings the rating in line with Fitch, which upgraded in March, while Moody's is still two notches below at B3. An upgrade is likely for Moody's at its next scheduled review, on 19 July, while positive outlooks at all three main agencies highlight the scope for further improvement towards a return to a BB-rating if the current policy trajectory is maintained. S&P highlighted improved confidence in the policy trajectory following local elections, along with early signs of progress in external rebalancing, which should both also be positive factors for Moody's. Looking forward, more concrete evidence of fiscal consolidation, as promised by Finance Minister Şimsek, will be important in further boosting investor sentiment as imbalances are reduced, while the constitution preparation process, which the parliament speaker launched by reaching out to the relevant political parties, will also be in focus.

In this context, Turkey's sovereign credit spreads have compressed towards the BB-rated sovereign average, with current market pricing already implying a "BB-" rating across the curve. This leaves limited scope for further significant spread compression as fundamentals gradually improve, especially with more supply likely, but strong technicals should keep demand for sovereign dollar bonds well supported.

ICE US$ Bond Sub-Index Spreads vs USTsICE, Refinitiv, ING

Author:Muhammet Mercan, James Wilson

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment