(MENAFN- ING)

At its March policy meeting, the Riksbank said rates should be lowered either in May or June. Lower inflation and a weaker domestic economic backdrop point to a cut this month, whereas a weak krona and a reluctance to move ahead of the ECB suggest holding until June. It is a close call, but the latest communication from Executive Board members and the wording of the March statement suggest the Riksbank may cut in May, but also deliver a relatively hawkish message.

The case for a cut

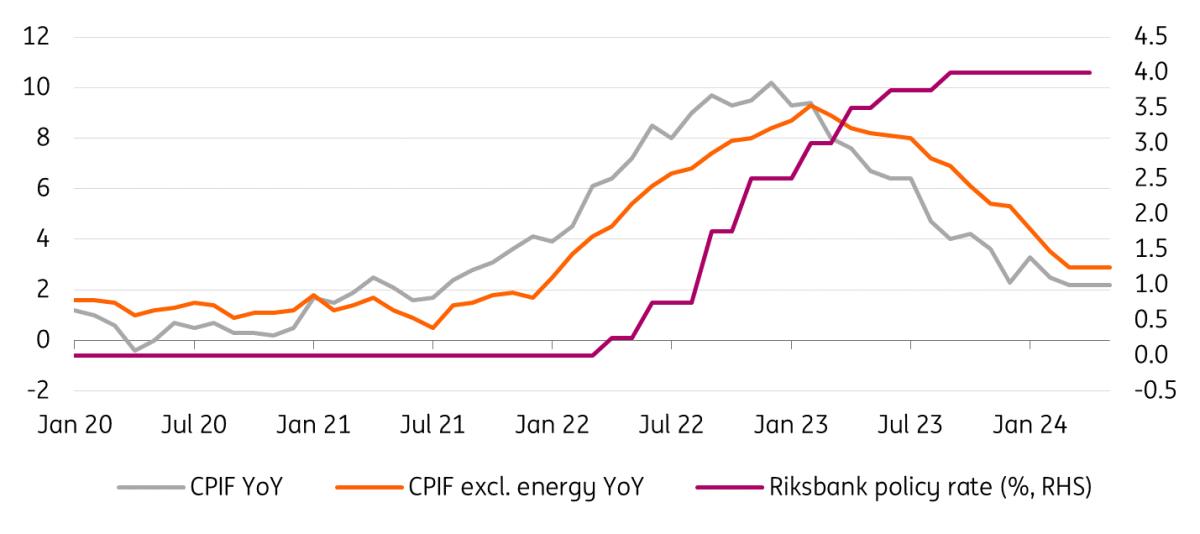

Inflation in Sweden has slowed more than expected, and probably no longer justifies the tight grip of restrictive monetary policy on the very rate-sensitive Swedish economy. CPIF inflation has declined to 2.2%, and the Riksbank-preferred core measure (excluding energy) to 2.9%. The Riksbank targets a 2% stable CPIF inflation.

The jobs market is also far from the ultra-tight conditions of 2022. Unemployment at 8.6% in March was above the pre-pandemic 5-year average of 6.9% and the percentage of firms saying labour is a limit on business has dropped to just 15% – one of the lowest in the EU, and a third of the 45% 2022 peak. This suggests lower risks of the jobs market fuelling further inflation.

Growth: Sweden has recorded four consecutive negative-growth quarters, with the latest 1Q print at -0.3% QoQ. Consumer confidence has recovered but remains close to the Great Financial Crisis and Covid lows. Sweden's economy has an elevated sensitivity to rates, with the mortgage market having one the highest share of flexible rates among developed countries. The good news is that optimism about the housing market is recovering at a time when transactions are starting to pick-up – presumably on the expectation of rate cuts. But the situation remains fragile.

Rates look too restrictive given lower inflation

Source: ING, Macrobond The case for a hold

Weak krona: the main argument to hold rates is the weakness of the krona. The shift to a dovish tone by the Riksbank earlier this year and the rise in USD yields has prompted SEK to trade around 8% lower YTD versus the dollar, and 5% versus the euro. This is a big conundrum for the Riksbank, because a weak krona is seen as one of the biggest inflationary risks. In almost every speech, Governor Erik Thedeen has stressed concerns on the currency.

More disinflation evidence? Another point is that inflation data tends to be quite volatile in Sweden, and holding rates until the 27 June meeting would allow policymakers to look at two more inflation prints (for April and May) to make sure disinflation is on a stable downtrend – especially on the service sector. The flash estimates in the eurozone, and particularly in Germany, pointed to some stickiness in prices in April.

Wait for ECB : the ECB is the Riksbank's“reference” central bank, and has its next meeting only on 6 June, when it is widely expected to cut by 25bp. It is generally believed that the Riksbank prefers to trail the ECB rather than leading it in policy cycles. If we look at the latest easing cycles, the Riksbank started cutting one month after the ECB in 2011, and in 2008, both central banks cut on the same day in a coordinated action.

Recent communication points to a (hawkish) cut

Governor Thedeen mostly stands out for comments on the krona, as he has long attempted verbal intervention through pointing at SEK undervaluation and the risks of a weak currency for inflation. He has recently sounded more constructive on disinflation, but we suspect that he would be in the camp of holding rates in May.

At the same time, there is an evident pressure from the other four members of the Riksbank's Executive Board to speed up easing. First Deputy Governor Anna Breman said SEK weakness is manageable and that gradual, cautious rate cuts is the main scenario. Per Jansson said that the risks to a May cut in Sweden mostly come from other central banks, and that he is significantly more confident on inflation. With the ECB likely going ahead with a cut in June and the Fed not sounding as hawkish as feared, Jansson's vote looks more likely to be for a cut next week. Martin Floden has downplayed the sticky service inflation risk, and Aino Bunge also signalled greater confidence on disinflation.

All in all, we see the consensus within the Executive Board as tilted towards a 25bp rate cut to 3.75% next week. The concerns about an excessive weakening of the krona should – in our view – be addressed with a relatively hawkish communication. That could mean signalling easing will be gradual and potentially dependent on krona's developments and other central banks' decisions. The goal would be to prevent markets from pricing in back-to-back rate cuts in Sweden and align with ECB's relatively cautious message.

How far would SEK need to fall to prevent a cut?

The US jobs report on Friday, 3 May is a key risk event in the FX market, which might ultimately influence the Riksbank's rate decision on 8 May. Consensus is for a slowdown in hiring to 240k in April, and our US economist is expecting an even softer print. Our base case is that the very risk-sensitive krona should either stabilise or recover more ground in the coming days, ultimately making the Riksbank more comfortable with a cut next week.

A bearish scenario for SEK (stronger US data, higher USD yields, weaker risk sentiment) begs the question of how far the krona would need to drop before next week's Riksbank meeting to tilt the balance from a cut to a hold.

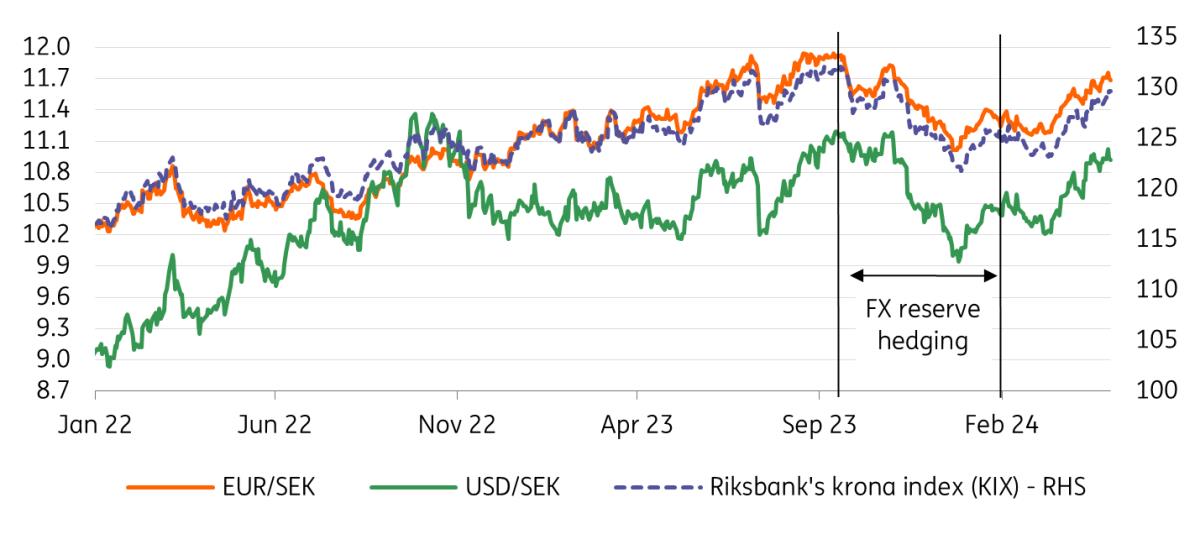

The Riksbank generally takes its own SEK trade-weighted KIX index as reference (higher KIX=weaker krona), and that is around 1.5% below its October 2023 highs and 2.5% below its September 2023, pre-FX reserve hedging programme highs. As shown in the next chart, the KIX moves almost identically in line with EUR/SEK, as the euro has a 46% weight in the index, so taking EUR/SEK as reference is appropriate.

We think that a move to the October high in EUR/SEK (11.83) from the current 11.68 would make a May cut close to a 50-50 deal, with further rallies beyond that level (11.90+) likely to tilt the balance to a hold.

The krona is re-approaching its 2023 lows

Source: ING, Refinitiv Market impact

Markets are currently pricing in -12bp for the May meeting, and -50bp in total over the next four meetings (May, June, August, September). This means that there is room for SEK swap rates to drop on a cut next week as markets may well adjust the pricing for September from the current 3.50% to levels closer to 3.25%.

A hawkish communication may contain the move in rates, but the downside risks for the krona next week (and beyond) are still tangible. The fact that the Riksbank is ready to cut rates despite a significantly weaker krona will inevitably convey the message that the Bank is not as concerned about currency implications for inflation as it might have been in the past, which unlocks upside potential for EUR/SEK up to the 11.90/12.00 area should USD rates remain supported on the back of strong US data and/or a more hawkish Fed.

However, EUR/SEK may struggle to stay at such high levels very long. First, because markets should price out Riksbank easing after a major SEK drop, and second because the Riksbank may deploy a new round of its FX reserve hedging operations. That is a form of FX intervention, which we estimate to have added up to 3% of extra SEK performance versus the euro in the September-February period. The programme was started when EUR/SEK was trading around 11.90-11.95 and USD/SEK was close to the 11.20 mark.

MENAFN02052024000222011065ID1108167758

Author:

Francesco Pesole, James Smith

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.