Polish Inflation Rebounds As Core Inflation Remains Set To Stabilise

Date

4/30/2024 2:20:22 PM

(MENAFN- ING)

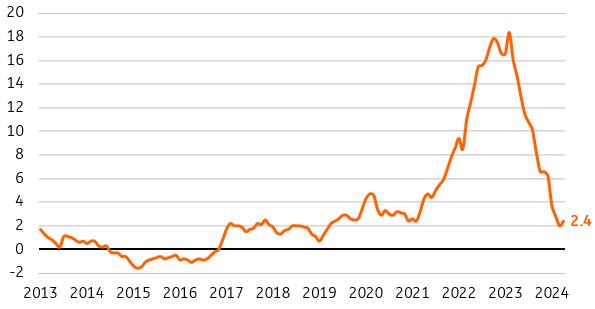

According to the flash estimate, consumer prices rose by 2.4% year-on-year in April (ING: 2.4%, consensus: 2.5%). Food and non-alcoholic beverages rose by 2.1% month-on-month, mainly as a result of the reintroduction of VAT – although it's worth noting that the pass-through was lower than implied by the full translation of higher tax rates. fuel prices rose by 2.1% MoM, while housing energy moderated by 0.2% MoM.

Inflation up for the first time in over a year

CPI, %YoY

GUS.

We estimate that core inflation excluding food and energy prices slipped to around 4.0% YoY from 4.6% YoY in March. The marked decline in the annual inflation rate is mainly due to the high reference base (up by 1.2% MoM in April 2023), but its momentum remains elevated at around 0.5-0.6% MoM. The main part of core price disinflation is now behind us, and core inflation will remain close to 4% in the coming months. This means that the threat of elevated consumer inflation is not over, and the National Bank of Poland will most likely stick to its hawkish rhetoric as a result.

There is an exceptionally high degree of uncertainty surrounding the forecasts for the inflation path through the second half of this year. The government has announced a partial freeze on electricity prices for households, but it is still unclear as to which level the distribution charges will be and whether action will be taken to limit potential gas price increases. In addition, we are likely to see changes to energy tariffs over the course of this year. In such circumstances, the MPC will most likely continue to keep interest rates unchanged. The first reductions are not expected until 2025, although discussions on monetary easing could begin towards the end of this year.

MENAFN30042024000222011065ID1108158024

Author:

Adam Antoniak

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.