403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Latam FX Talking: Chile's Peso Looks Vulnerable After Aggressive Rate Cuts

| USD/BRL | USD/MXN | USD/CLP | ||||

| 1M | 5.15 | ↓ | 16.75 | ↓ | 975.00 | ↓ |

| 3M | 5.15 | ↓ | 16.75 | ↓ | 950.00 | ↓ |

| 6M | 5.15 | ↓ | 16.75 | ↓ | 900.00 | ↓ |

| 12M | 5.00 | ↓ | 16.50 | ↓ | 850.00 | ↓ |

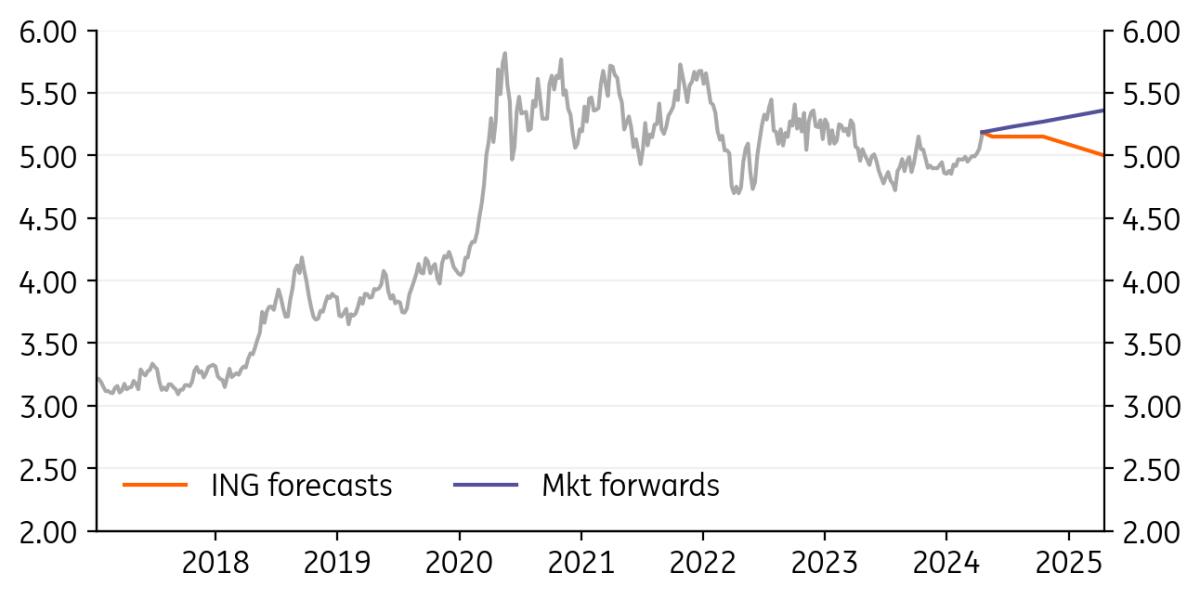

| USD/BRL 5.1851 | Neutral | 5.15 | 5.15 | 5.15 | 5.00 |

- The Brazilian real continues to lag and USD/BRL looks quite comfortable above 5.00. The broadly stronger dollar is playing a role, but it does look as though there is a Brazilian story here too. There is increasing focus on the interventionism of President Lula – especially with Petrobras – which could damage sentiment. Equally, the fear is that the Lula administration somehow overrules the fiscal plan such that a balanced budget is missed. Brazilian activity is doing quite well. Strong real wage growth is helping consumption and Brazil should grow 2% this year. The policy rate is now 10.75% and is expected at 10.25% in June. The market struggles to price the policy rate sub 10%, however.

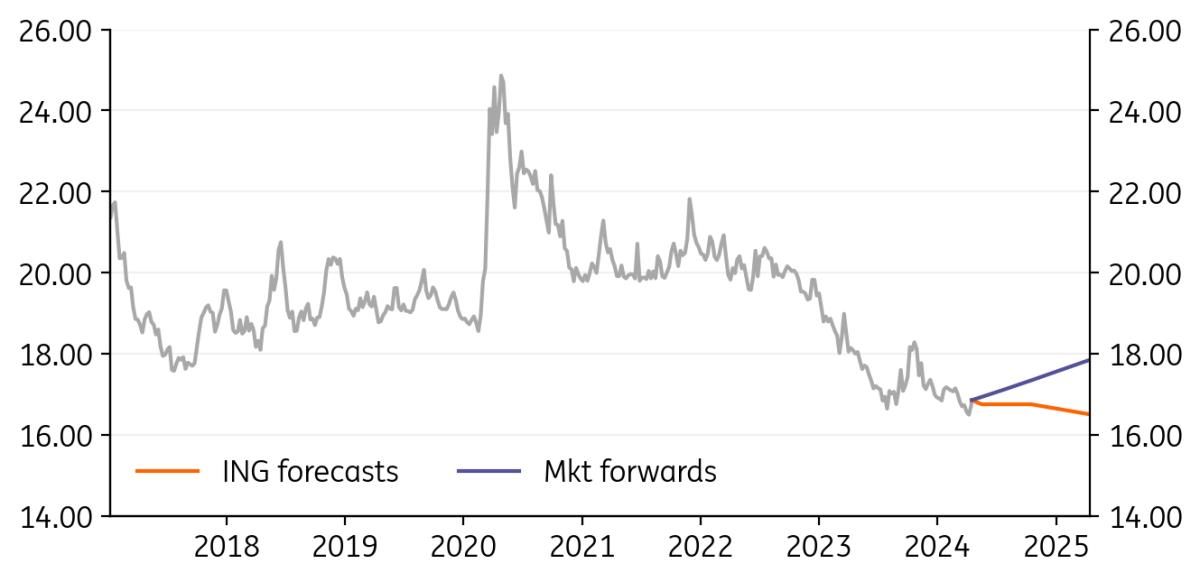

Refinitiv, ING USD/MXN: The Teflon peso

| USD/MXN 16.85 | Neutral | 16.75 | 16.75 | 16.75 | 16.50 |

- Despite the back-up in US rates, the Mexican peso has been performing strongly. Some think that may be a function of Banxico needing to join the Fed in keeping rates higher for longer. But FX volatility still seems relatively low and the carry trade also remains popular. MXN offers high, risk-adjusted yields. We are a little worried that Mexican policymakers will see the peso as too strong – on an inflation-adjusted basis it is back to levels last seen in 2007. To address this, Banxico may well start to cut rates quicker (the 11% policy rate is priced at 8.5% in two years' time) or come up with some FX reserve rebuild programme. This may only happen after the presidential elections on 2 June.

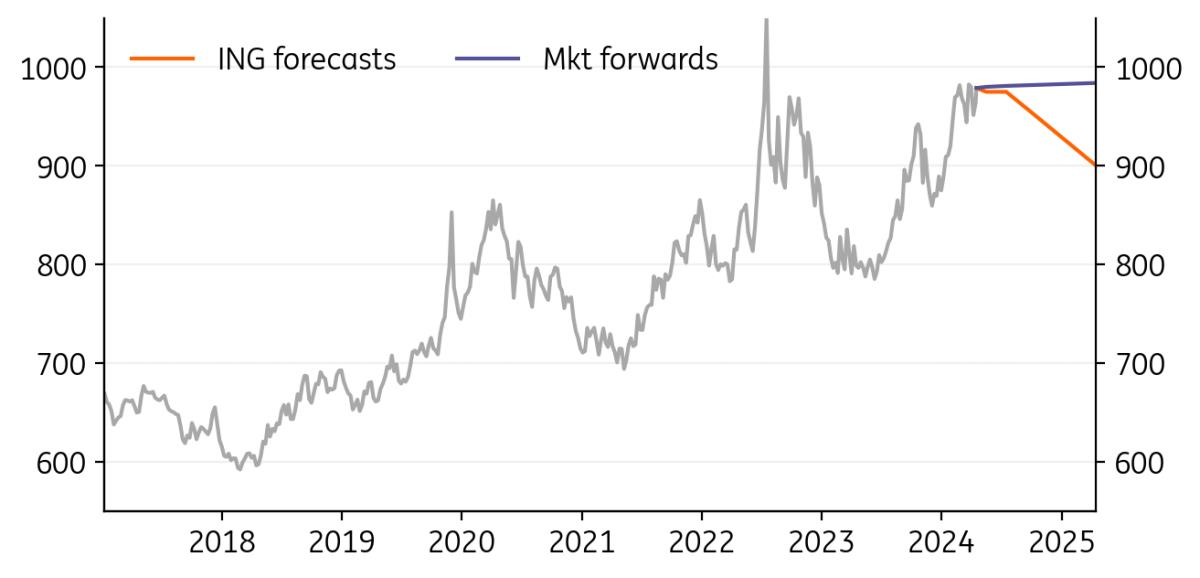

Refinitiv, ING USD/CLP: Yields are not particularly supportive for CLP

| USD/CLP 978.88 | Neutral | 975.00 | 975.00 | 950.00 | 900.00 |

- Chile's policy rates have been slashed from 11.25% to 6.50% over the last nine months as the central bank has gone for growth. However, it has now started to slow the pace of rate cuts since USD/CLP had traded close to 1000 again. The central bank wants to take rates to 6.00% in June – but we are worried that such a low real rate of just 2% leaves the Chilean peso vulnerable. Given the prospect of US rates staying higher for a little longer, we therefore see USD/CLP trading longer in this 950-1000 range. Chile's 3-4% of GDP current account deficit and dovish central bank means that USD/CLP trades on 14% volatility compared to 10% for Brazil's real and Mexico's peso. i.e. Chile requires a risk premium.

Refinitiv, ING

Author:Chris Turner

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment