403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Sticky UK Services Inflation Pushes Back Rate Cut Hopes

(MENAFN- ING)

Macrobond, ING calculations

Macrobond, ING calculations

The Bank of England has pinned the timing of the first rate cut on wage growth and services inflation. The former came in hotter than expected in data released on Tuesday, and now the latest data on the latter has come in stickier than expected too. The result is that markets are now only full pricing the first rate cut in November.

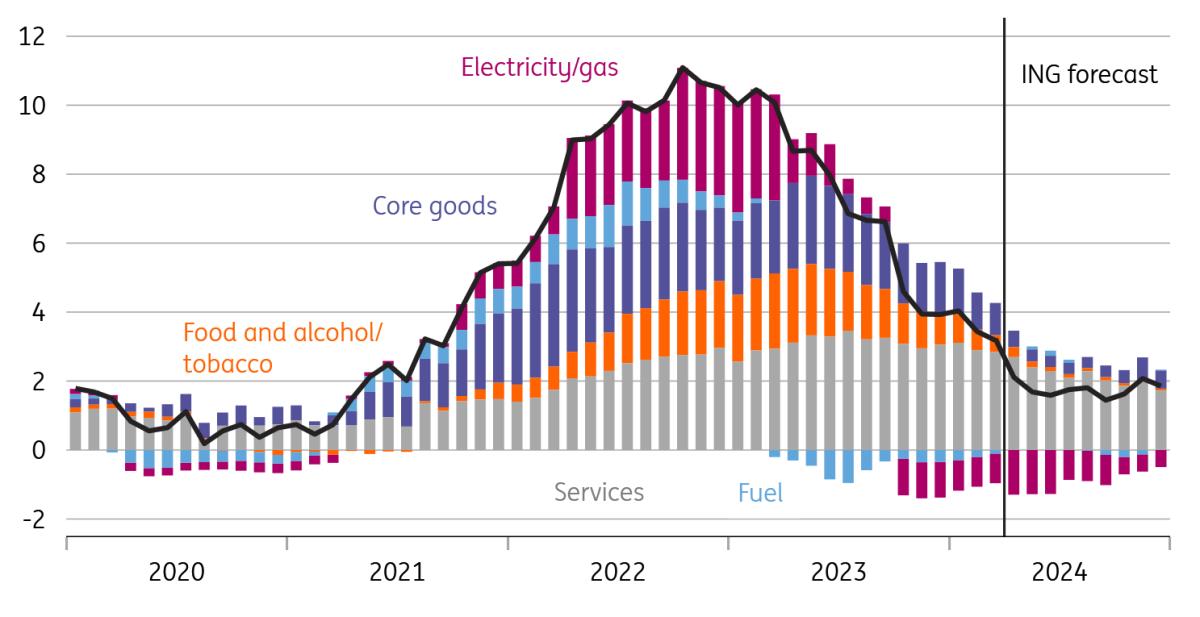

While overall inflation continued to tick lower to 3.2%, albeit slightly above consensus, services inflation came in above the BoE's most recent forecast. The Bank had been looking for services CPI at 5.8% in March, whereas it remained sticky at 6.0%. What's interesting is there's no one single thing that's driving this stickiness, but what stands out is rental inflation, which, contrary to other parts of the inflation basket, is only now reaching its highs.

Contributions to UK inflation and ING forecasts (YoY%)Macrobond, ING calculations

We should, however, see a renewed downtrend in services inflation over the next couple of months, but this latest data reinforces our view that it could prove a little stickier than the Bank is forecasting in the near term. Next month's data covering April is really important, because this is when swathes of the services basket is subject to annual index-linked price rises. April's data last year came in way hotter than anyone had expected and indeed that data drove the biggest daily upward move in two-year swap rates at any point in 2023. That's a gauge of market interest rate expectations for the BoE.

This year's price rises should be less aggressive, given that many are tied to recent rates of headline inflation which are much lower than the levels that fed into the index-linked rises last April. But there's still scope for surprise and the Bank will want to see the data on this before committing to any policy action. That all but rules out a rate cut in May, and if we're right that April's data proves stickier than the Bank is expecting, then we think that would drastically reduce the chances of a cut in June, too. We think April's services inflation could come in at 5.6% vs. the BoE's forecast of 5.3%. Our base case is that the Bank will cut rates for the first time in August.

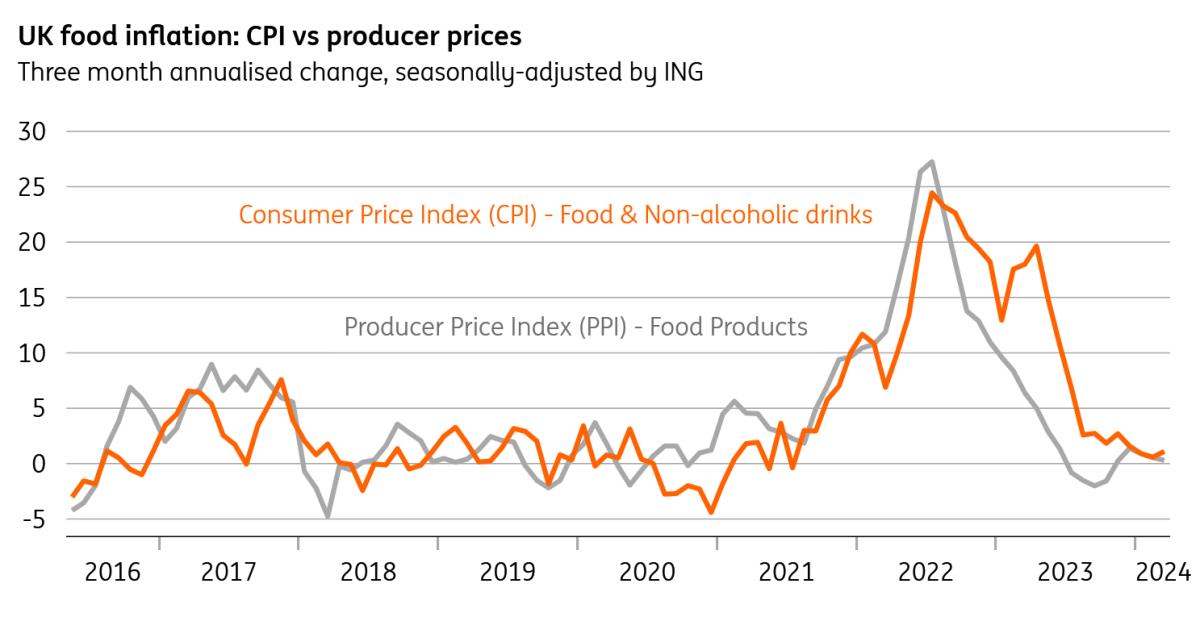

Annual food inflation is heading towards zero, judging by producer pricesMacrobond, ING calculations

Ultimately, that debate will decide the timing of the first rate cut, though from the perspective of consumers, the good news is that there's plenty more disinflation in the pipeline elsewhere. We already know that household electricity/gas bills fell by 12% on average at the start of April, and in all likelihood, we'll get another fall when the regulator's price cap is reset again in July.

Food inflation is also slowing rapidly too. Having peaked close to 20% this time last year, it's now at 4%, and we think it'll be close to zero by the summer. Producer price inflation, measured on a three-month annualised basis, has been flat or slightly negative for several months now.

That means headline inflation will fall close to 2% in April and to 1.6% in June and stay below the Bank's target for most of 2024.

Author:James Smith

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment