403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

The Bank Of Korea Freezes Policy Rates And Keeps Macro Outlook Unchanged

| 3.5% | Base rate

Unchanged since January 2023 |

| As expected |

The Bank of Korea has not changed its growth and inflation outlook, but acknowledges risks surrounding the domestic economy's project financing and real estate markets as well as growing global geopolitical risks. The data so far has been encouraging, showing stronger-than-expected exports (particularly in semiconductors). At the same time, however, the domestic economy has weakened more than expected.

Governor Ree Chang Yong, repeated several times the "uncertainty" currently being faced by the central bank. Inflation in the last mile is expected to be bumpy, and the BoK isn't confident about the the path ahead. The policy focus should therefore remain on curbing inflation for the time being. However, if sluggish domestic growth continues and reduces inflationary pressure, then the BoK's stance will eventually change.

Also worth noting from today's meeting is that one in six members opened up an option for rate cuts to preemptively respond to slowing consumption, while the rest preferred to keep policy rate at the current level in the next three months. Today's decision was unanimous but there is certainly growing concern about weak consumption.

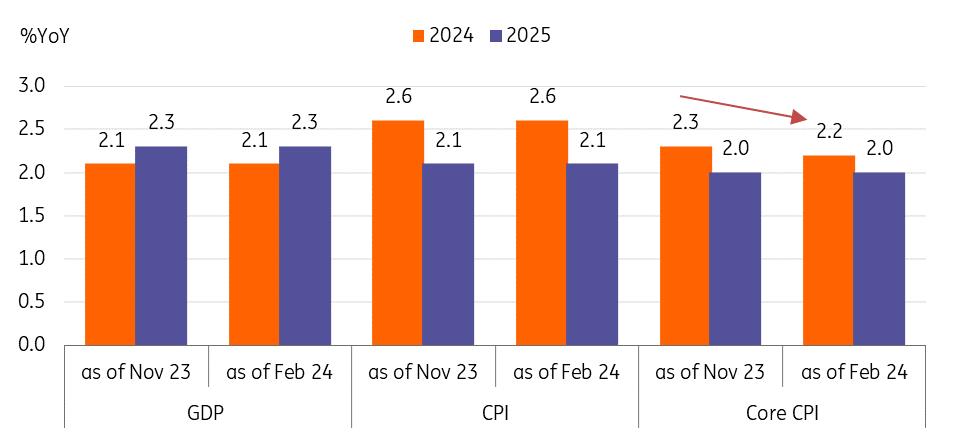

The BoK's quarterly outlookCompared with the previous outlook report released in November, the key macro outlook remained unchanged. Headline GDP and CPI forecasts for 2024 and 2025 remained the same, but core CPI inflation edged down from 2.3% year-on-year to 2.2% for 2024, mainly due to sluggish consumption recovery.

For the GDP outlook, growth dynamics have changed, and private consumption was revised down from 1.9% to 1.6%. This largely reflects the ongoing slowdown in consumption and construction, offset by an upward revision of exports (4.5% from 3.3% previously).

BoK's outlook hasn't changed much

Source: BoK BoK watch

We believe that inflation will remain the main concern for the Bank of Korea, and its stance will therefore remain hawkish stance for the time being. The reshuffle of two board members is scheduled in April, but for now, we are not sure how this would shift the board's stance. We think that the ways in which the macro situation evolves should be more of a focus than the characteristics of individual board members.

We don't think the BoK is likely to care too much about the timing of the Fed's rate cut. The macro conditions of the two countries are quite different at this stage. The BoK will likely focus on domestic matters such as inflation, project financing issues, household debt, and financial market moves.

Regarding the risk surrounding PF and construction, we believe that the BoK will likely first utilise its micro-level policy instruments, such as facility lending and loan cost cuts, to supply targeted liquidity in the market if the situation worsens.

The BoK will meet in April, right after the general election. By then, we expect inflation to return to a downward trend and that inflation expectations will also move down to the 2% level. We also believe the continued tight credit conditions will weigh on financial market instability, consumption and investment. If our macro view is correct, a minor vote favouring a rate cut could be made as early as April.

The quarterly outlook report will be released in May, and the inflation outlook should be key to watch for emerging minor votes. It will still take some time for a rate cut decision, and we've pencilled in a 25bp rate cut for the July meeting, followed by an additional 25bp cut in the fourth quarter. Due to concerns over the yield gap differentials and high levels of private debt, the BoK's easing should be quite limited and gradual.

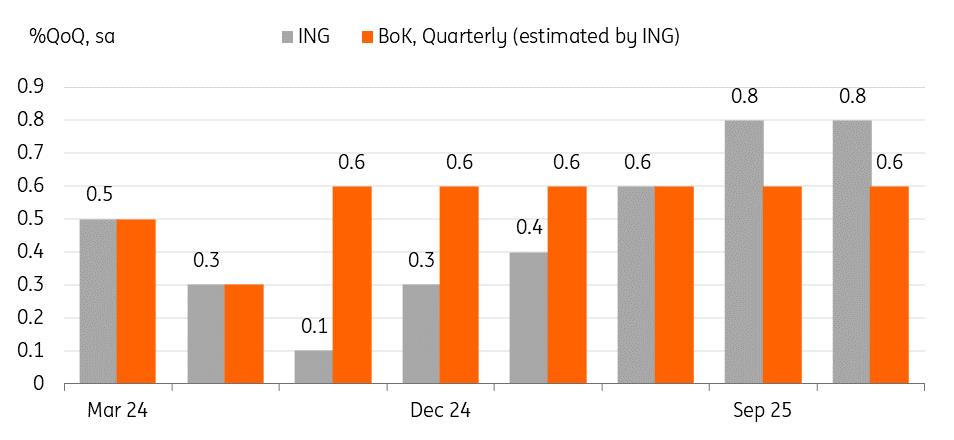

GDP outlook : ING vs BoK

Source: BOK, ING estimates The BoK releases half-year GDP outlook figures in terms of year on year growth

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment