(MENAFN- ING)

Housing data and regional business survey releases will have little impact on the Federal Reserve's interest rate path. In the UK, look out for key jobs, inflation, and retail sales figures

In this article - Four rate hikes expected in the US regardless of this week's data

- Growing inflation could force a rate hike in Canada

- What to expect in a busy week of UK data:

Shutterstock

Share

Download article as PDF

Newsletter

Stay up to date with all of ING's latest economic and financial analysis.

Subscribe to THINK Four rate hikes expected in the US regardless of this week's data

Financial markets are firmly behind the view that the Federal Reserve will raise interest rates four times this year and will soon seek to shrink the $8.8tn of assets it has on its balance sheet. There will be little to alter this belief in the coming week with housing data and regional business surveys the most significant releases in what is a holiday shortened week. We will be looking to see what sort of hit the Omicron wave has had on manufacturing in the regions while the housing numbers should continue to point to solid activity. The next key release is the 4Q Employment Cost Index on 28 January. Another solid rise here could cement expectations for a March interest rate hike.

Growing inflation could force a rate hike in Canada

In Canada, the CPI report is the key release and with headline inflation set to break above 5% we could see growing expectations of a January Bank of Canada interest rate hike. We are more cautious on the timing at this stage given some uncertainty over the Omicron hit to economic activity, but higher interest rates are certainly coming.

What to expect in a busy week of UK data:

- Jobs (Tues): The labour market has withstood the end of the furlough scheme last September pretty well. Redundancies have stayed stable, and we expect next week's data to echo the favourable hiring backdrop. But what matters most for the Bank of England are wages, and the jury's still out on where they are headed. As various data distortions fade, it looks like wage growth is roughly where it was pre-pandemic, which is a key part of the Bank's hiking rationale. There's also some evidence that pay rises have been larger in more short-staffed sectors, like IT and transport. Whether we're headed for a wage-price spiral though, we're less convinced.

- Inflation (Weds): Expect CPI to nudge a little higher once again, helped partly by accelerating food inflation, and perhaps further upside to used car prices (which are already up 30% in the past six months). Inflation is unlikely to peak until April, where we expect a roughly 50% increase in the household energy price cap, taking headline CPI to the 6.5% area. Importantly, gas futures prices are still pretty elevated for next winter, and if that stays the case we are looking at another 10% increase in electricity costs in October's cap update. As things stand, inflation is set to stay close to 4% until the end of this year, but dip noticeably below target in 2023.

- Retail sales (Fri): We expect a fall in sales after a bumper November, following what appears to have been a stronger-than-usual Black Friday trading period. What's less clear is if the arrival of Omicron, and reduced spending at social venues, translated into a boost for goods purchases, like we saw in past Covid waves. We suspect that effect will be much less pronounced, and short-lived, with early hints that consumers are less cautious about visiting hospitality venues than they were just before Christmas.

With Omicron's effect looking like it has been fairly modest, and given well-publicised concerns on the MPC about ever-higher rates of headline inflation, we think a February Bank of England rate rise is looking increasingly likely. But markets, which have been pricing Bank rate around 1% by the summer, are likely still overestimating the pace of tightening.

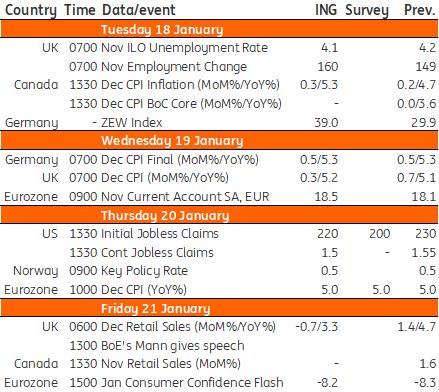

Developed Markets Economic Calendar

Refinitiv, ING, *GMT

MENAFN14012022000222011065ID1103542123

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.