403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

South Korea: Monthly Activity Data Contracted In May, Pointing To A Slowdown In Current Quarter GDP

| -1.2% |

Industrial Production

%MoM, sa |

| Lower than expected |

Industrial production (IP) unexpectedly fell by 1.2% MoM sa in May (vs revised 2.4% in April, 0.2% market consensus). Monthly growth has been volatile recently, due to fluctuations in automobile and semiconductor production.

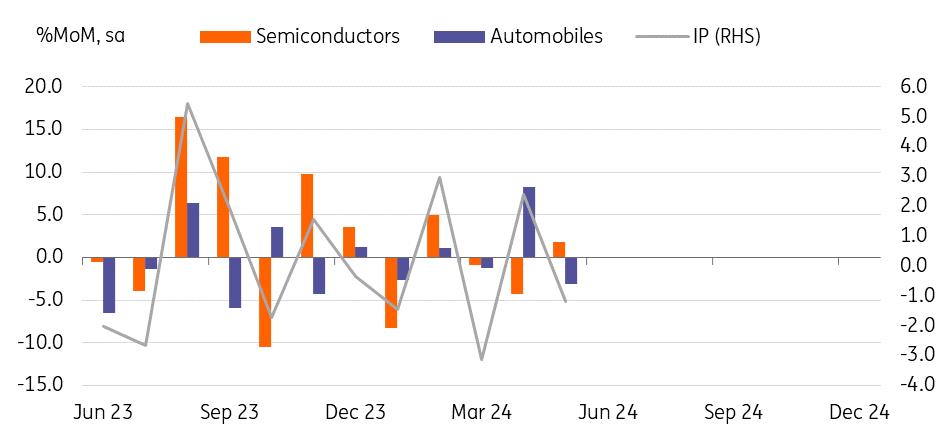

As expected, semiconductor production (1.8%) rebounded after two months of decline thanks to strong global demand for AI chips. Shipments also bounced back quite smartly (18.8%) but inventories edged up this month (1.4%). We think the inventory level itself is not a concern for now as chipmakers have cut their inventories by almost 40% over the past ten months. Strong semiconductor production should lead to an overall gain in IP this year.

Meanwhile, automobile output (-3.1%) dropped as industry data suggested. We expect auto production to moderate in the coming months, as global demand is likely to lose momentum and inventories have been on an upward trend since early 2023.

Service activity declined by 0.5% in May (vs +0.7% in April). Retail/wholesale (1.9%) rose but deeper falls in financial (-2.5%) and communications (-1.6%) caused overall activity to decline.

IP data has been choppy

Source: CEIC Retail sales dropped for a second month in May

Retails sales fell 0.2% MoM sa in May (vs -0.8% in April). By product, durable goods sales (0.1%), especially automobile sales (3.0%) rebounded. Consumer goods also rose in the last three months, as food and pharmaceutical sales rose firmly. However, this was more than offset by the decline of semidurable goods (-2.9%) such as apparel, and entertainment goods.

Monthly data showed that retail sales have been quite weak since the middle of 2022. In year-on-year terms, retail sales stayed in negative territory most of the time. However, in terms of GDP, private consumption has always been stronger than the monthly data, so we suspect that residents' spending abroad and on services must have been stronger than their goods consumption. However, weak consumption should be a drag on overall growth over the next few quarters.

Retail sales remained weak in MaySource: CEIC Investment contracted in May

Equipment investment dropped -4.1% MoM sa in May, declining in four out of the past five months. The falls in the last two months were mainly due to a sharp drop in the volatile "other transportation equipment" segment (such as vessels and aircraft). IN addition, the strong performance in semiconductors has not translated into strong equipment investment. The forward-looking machinery orders data declined -1.4%, and so the near-term outlook for equipment investment is quite cloudy.

Construction also declined -4.6% MoM sa in May (vs 3.1% in April). We believe that the last quarter's rebound in construction was temporary as some major projects were completed and government-led infrastructure projects were implemented. We believe that the construction cycle has bottomed out as orders have picked up for a few months. But the recovery is likely to be limited given the sluggish real estate market and high inventories.

GDP and BoK outlookDomestic activity softened in May, but we don't think this will trigger an immediate BoK rate cut. Recently, the government and policymakers have been openly urging the BoK to ease monetary conditions as inflation gradually moderates. But we think the inflation path ahead is the most important factor for the BoK. However, we also acknowledge that given today's weak data, the likelihood of a rate cut in 3Q24 and the emergence of votes for cuts is increasing. We expect consumer prices to decelerate gradually in 3Q24, but upside risks are still quite substantial, consequently, we expect the BoK to deliver its first rate cut in October.

For the GDP outlook, we maintain our current forecast of 0.2% QoQ sa in 2Q24, down from 1.3% in 1Q24. Net exports will remain a driver for GDP, but private consumption and investment will both drag on growth.

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment