403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

The European Trailer Market Cools After Years Of Expansion

(MENAFN- ING) After some strong years, faltering transport demand sparked a downturn in the European trailer market in 2023. Trailer 'hoarding' led to a delay in investments and long lead times disappeared. Add to that capacity pressures, and we don't think we'll see a trailer sales recovery any time soon In this article A 2021-2022 rebound for the European trailer market Longer deployment and refurbishment added to the trailer fleet Contraction trailer sales to slow in 2024 Market share of curtain side trailers revived following box trailer price hikes Trailers need to decarbonise and electrif

We don't expect to see a trailer recovery any time soon A 2021-2022 rebound for the European trailer market

RAI/RDC, CLCCR, Febiac, VDA, SDES-RSVERO, *ING Research

Eurostat, *ING Research Longer deployment and refurbishment added to the trailer fleet

Eurostat, *ING Research Contraction trailer sales to slow in 2024

RAI/RDC, CLCCR, Febiac, VDA, SDES-RSVERO, *ING Research, **Includes The Netherlands, Belgium, France, Germany, UK

RAI, KBA, ING Research Market share of curtain side trailers revived following box trailer price hikes

RAI, KBA, ING Research *up and until Oct. 2023 Trailers need to decarbonise and electrify

We don't expect to see a trailer recovery any time soon A 2021-2022 rebound for the European trailer market

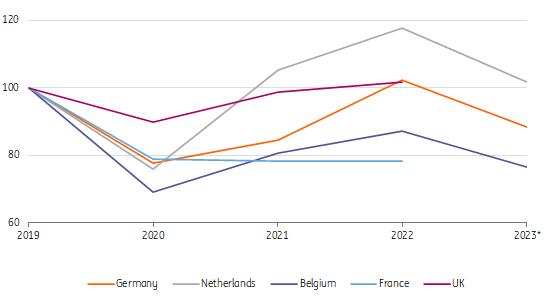

The trailer market saw a rebound from the pandemic lows back in 2021, mainly on the back of strong order books. Trailer manufacturers encountered shortages with components such as axles, but on a less severe scale than in truck production, where electronics - and chips - are more important. They also saw greater success in keeping production lines up and running. Accelerated by pent-up demand, some European countries' trailer registrations surpassed their pre-pandemic registration figure or already reached records previously seen in 2022.

Unlike trucks, trailer registrations rebounded in 2021-2022Development of new semi-trailer registrations per country (2019 = 100)

RAI/RDC, CLCCR, Febiac, VDA, SDES-RSVERO, *ING Research

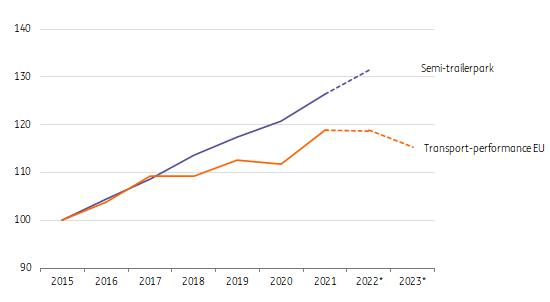

The European semi-trailer fleet continued to grow through the economic cycle as well as the pandemic. In total the fleet is estimated at around three million in 2022 (in EU + EFTA + UK). The European trailer park has grown rapidly since 2015 and in contrast to the truck fleet, the trailer fleet has already outpaced road transport for longer. Figures about 2022 from the Dutch fleet suggest that this continued to grow through 2022 and probably into 2023. On average, the fleet has expanded by around 30% since 2015.

In prevalent European home countries for international transport, the trailer fleets have expanded. As such, Lithuania, Romania, and Poland – for a long time known as the European market leader in international road transport - have grown the fastest in recent years. International transport activities and registered equipment have increasingly been shifted to entities in Central and Eastern Europe for cost reasons.

European semi-trailer fleet expansion exceeded transport demand for longerDevelopment of trailer park vs. transport performance in ton/km (EU), index (2015 = 100)

Eurostat, *ING Research Longer deployment and refurbishment added to the trailer fleet

The gap between the trailer fleet and transport demand has widened recently. The most important reason for this is that fleet owners tend to stick to older trailers. Consequently, the average age of the fleet has increased. There are multiple reasons for this phenomenon:

- The transport market has turned more volatile and less predictable in recent years and this requires more flexibility 'just in case'. It doesn't cost much to keep trailers in the fleet and more trailers don't necessarily require more drivers. Consequently, the trailer-truck ratio has gone up. Drawbars are increasingly being replaced by semi-trailers, which are deemed more flexible in operations. Even in a country with a long tradition of drawbars and swap bodies, Germany, the semi-trailer is gradually gaining ground. The role of trailers in logistics has expanded too. Trailers are more often used as means of storage (e.g., at warehousing docks). Also, trailers travelling between the UK and the rest of Europe have longer turn-around times after Brexit. Fleet owners have chosen to attain and refurbish semi-trailers more often in recent years. Production limitations and shortages were a reason; higher new prices and sustainability considerations also became a factor. Refurbishment could extend life cycles by 5-6 years Lessors and large fleet owners such as TIP, PNO, DHL and DSV are also convinced that longer deployment is possible. Refurbishment used to be common practice, exclusively for more expensive units such as bulk trailers, but this happens more often for other configurations as well.

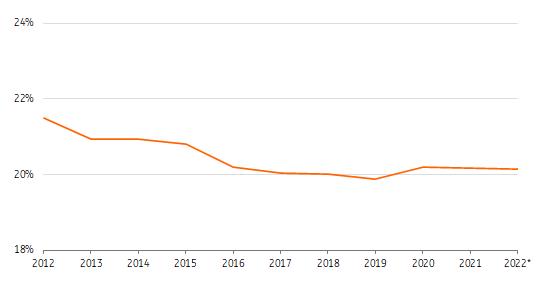

Another factor in play for fleet development is efficiency. Over time, vehicle occupation rates have improved. However, despite multiple efforts at further efficiency improvement – and a further reduction of empty running - has shown itself to be easier said than done against the current economic and logistics backdrop. Despite the planning benefits of digitalisation and platforms, further efficiency improvement stalled.

The impact of regulation (such as driving time, rest hours and locations) in combination with specific client preferences has limited the upside. Intensified cooperation (data-sharing) and perhaps the use of artificial intelligence in planning still provide an upside for efficiency, but as mentioned above, there are more variables in play.

Reduction empty running in European road haulage stalledShare of empty road freight transport vehicle km's in the EU-27

Eurostat, *ING Research Contraction trailer sales to slow in 2024

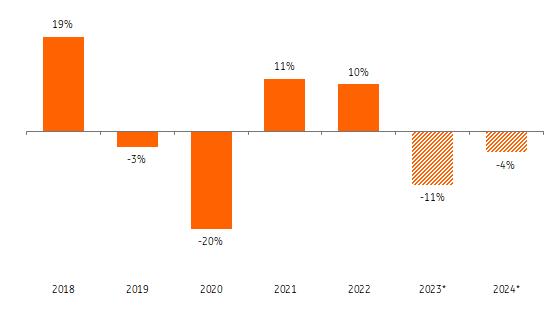

Following the decline of freight transport demand at the end of 2022, things started to change. The normalisation of elevated consumer demand for goods, economic headwinds, and rapidly rising interest rates affected the business climate and investment appetite. This suppressed demand for new trailers in 2023 and, after catching up with deliveries and the normalisation of extended lead times, this showed up in registration figures.

Trailer lifecycles can be stretched fairly easily, and that can lead to a relatively speedy adaption and reduction. For the full year 2023, registration is expected to fall by just over 11%. We still expect to see a contraction in 2024, albeit smaller, as the economy is expected to remain sluggish and road transport only mildly recovers. With economic growth catching up, expansion could happen in 2025.

Despite market headwinds, large fleet owners such as leasing companies TIP and PNO continued to invest in fleet renewal and extension in 2023. The leased-out share in the trailer market has become significant over time, and operational solutions like 'trailer as a service' have been introduced.

Setback after earlier high tide on the European trailer marketWestern European** registrations of semi-trailers, YoY

RAI/RDC, CLCCR, Febiac, VDA, SDES-RSVERO, *ING Research, **Includes The Netherlands, Belgium, France, Germany, UK

Following the drop in order intake, trailer manufacturers have also scaled back their units' production and now clearly operate below their maximum capacity. The changed market conditions also intensified competition between manufacturers, with price pressure returning. Average prices of new trailers have risen at least 25% against the backdrop of the inflationary shock in 2022.

But raw material prices are no longer at extremely elevated levels and this will gradually trickle down via suppliers. At the same time, wage increases push up production costs structurally. Although prices won't return to previous levels, buyers have gained market power, which is likely due to a moderation of prices over the course of 2024. In combination with a starting recovery of freight volumes and an older fleet, this may trigger some extra demand again.

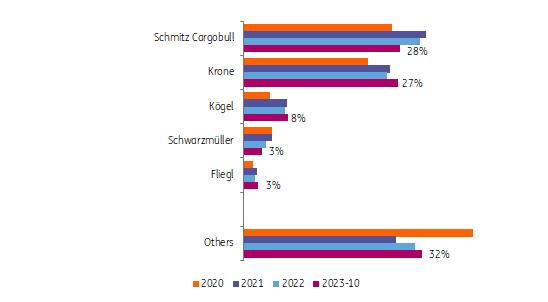

Krone approaches Schmitz's market share, other specialist brands regain groundMarket share

in new semi-trailer registrations in Germany

RAI, KBA, ING Research Market share of curtain side trailers revived following box trailer price hikes

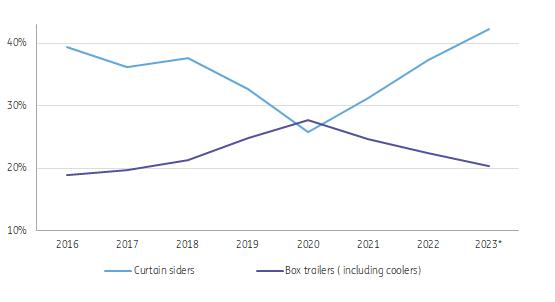

When looking at different types of trailers, there has been a shift in trailer registrations from traditional curtain siders to box trailers for security reasons. The rise of e-commerce also had an impact here. The share of (fixed) box trailers, including coolers, even exceeded the traditional curtain sider share in 2020. However, the trend hasn't been sustained in the last couple of years; sales of curtain siders have revived, with market share again hitting 40%.

Initially, large (rental) fleet orders have pushed curtain sider deliveries. But from 2022, significant price increases for heavy box trailers have probably reversed the trend. Fleet owners may have decided to refurbish trailers and postpone their replacement. Demand for box trailers is likely to catch up somewhat later, and therefore, we expect the share of box trailers – and especially coolers - to stay at higher levels than previously.

Popularity curtain sider return with higher prices for box trailersShare of main semi-trailer configurations in total registrations in Europe's largest market Germany

RAI, KBA, ING Research *up and until Oct. 2023 Trailers need to decarbonise and electrify

Although the combustion engine is the main focus for carbonisation, the energy transition increasingly also affects the trailer market and its manufacturers. The adopted European plan to increase the CO2 reduction targets for heavy-duty also includes obligations for a 15% reduction for semi-trailers such as 3-axles 'standardised' box trailers by 2030 compared to 2024 when the CO2-labelling via the so-called VECTO tool starts. For some specials and drawbars, 12,5% and 7,5% applies.

Achieving this target isn't as easy as the relatively low figure may suggest. As trailers lack an engine, progress should be found in the used materials, design, and components such as the axles and cooling system. European manufacturers branch CLCCR already declared this hardly realistic. Nevertheless, and apart from materials, significant CO2 reduction could be reached by electric technologies which are already available:

- Over the years, the share of conditioned transport has grown steadily, but almost all cooling units on trailers are still equipped with diesel engines. This has now started to change with increased attention to hybrid refrigerated trailers and full-electric systems, which are powered by the grid or operate in combination with solar panels. Another available electric feature for trailers is the regeneration axle that works in combination with a battery. Many fleet owners have already shown interest in this. The next generation is an axle which even has its own battery pack and electric motor, which is able to 'push up' the truck from the rear side. However, this is not yet approved under European law.

The market entrance of electric trucks could perhaps simultaneously push the electrification of the trailer. But as it still takes over two decades to replace the full fleet, it could also work in combination with diesel trucks and raise efficiency.

Author:Rico Luman

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment