Rates Spark: Drawing Out The Cycles

Date

9/22/2023 4:11:48 AM

(MENAFN- ING) With the bank of England's hold, while retaining all optionality, another central bank is attempting to draw out the cycle. That may keep bull steepening impulses at bay for now and leave room for a steepening more driven via the back end first if data broadly holds. The PMIs are the main data event for today In this article Steepening impulses from here on are probable, but not necessarily via the front end first Today's events and market view

Steepening impulses from here on are probable, but not necessarily via the front end first Following the Federal Reserve, the Bank of England has now also decided to keep rates on hold in a close 5-4 vote by the committee. But all options for another hike remain on the table. Maybe the BoE decided that the Fed's approach was better suited to its needs than the European Central Bank's.

The ECB had hiked, but in signalling that rates had reached levels sufficiently high to make a substantial contribution to reaching the inflation goal had been interpreted as rates having essentially topped.

ECB officials have since pushed against this notion, emphasising that this still means rates can rise under certain conditions. And some have resorted to shifting the discussion to the balance sheet. And the idea that speeding up quantitative tightening should precede rate cuts – as some officials have hinted – may be another strategy to draw out the cycle. Especially given that anything involving the ECB's balance sheet, including discussion about potentially adjusting the minimum reserve ratio, also ties in with the review of the operational framework, which is slated to conclude only by the end of the year.

The bullish steepening impulses that would typically unfold once cycle peaks have been reached are being held back by the optionality to do more that central bankers have retained. Still, we feel the room for policy rates to rise further is running out as headwinds are accumulating, but until markets see an actual smoking gun they remain more cautious.

Having been caught off-guard by the surprisingly hawkish Fed and its impact bear flattening, even if quickly reversed, is a case in point. In the meantime, the steepening impulses could continue to come from the back end as long as the data broadly holds, although the outright levels now look elevated at the back end. Still, the initial jobless claims data has just proven its relevance again yesterday, accelerating the steep sell-off in 10Y USTs towards 4.5%.

If cracks become more obvious, a brief bull flattening seems possible if central bankers are reluctant to embrace the signs of an impending downturn as they remain focussed on inflation risks – the effect of conducting policies via the rear mirror to which especially the ECB appears susceptible. The overly rosy outlooks from the Fed and also the ECB's own very optimistic view make room for disappointments. But we feel these could be brief interludes only or even just play out in relative terms.

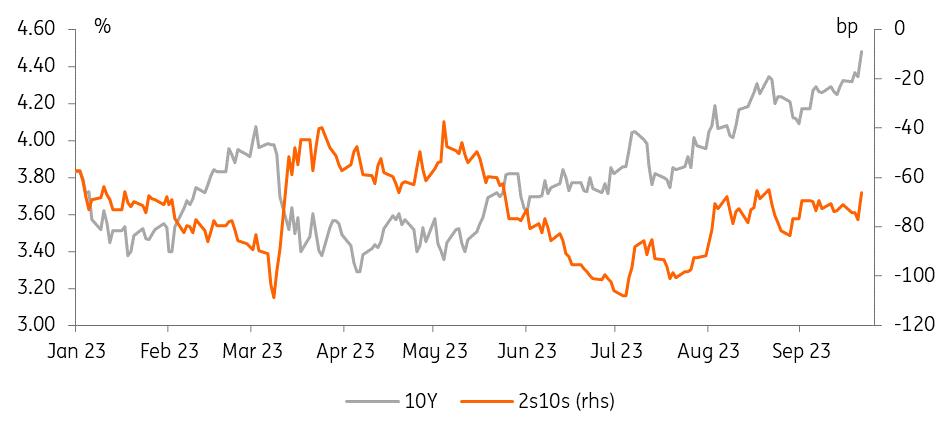

The long end is pulling the curve steeper

Refinitiv, ING Today's events and market view The US data have shown again what is relevant for the market. In the end, everything hinges on the data and whether it finally topples over. Today, the flash PMIs are the main event. Recall that in the US the larger surprise is the S&P PMI services last month had sent jitters through the market, but sentiment was probably also driven by the even larger disappointment in the European PMIs. For today, markets are seeing eurozone services slipping deeper below 50, while the manufacturing index is seen only slowly climbing out of its hole. All are still in recessionary territory.

Next week data will remain the main theme. In the US, the main focus is on the consumer with confidence readings as well as personal income and spending data – the consumer story is a crucial input for the soft landing scenario. We will also get the PCE deflator, the Fed's preferred inflation measure. In the eurozone, the main highlight is the September flash CPI, and it should give us more reasons to believe we have already seen the last ECB hike.

MENAFN22092023000222011065ID1107119104

Author:

Padhraic Garvey, CFA, Benjamin Schroeder

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.