| 2.3% YoY | China's April retail sales growth |

| Lower than expected |

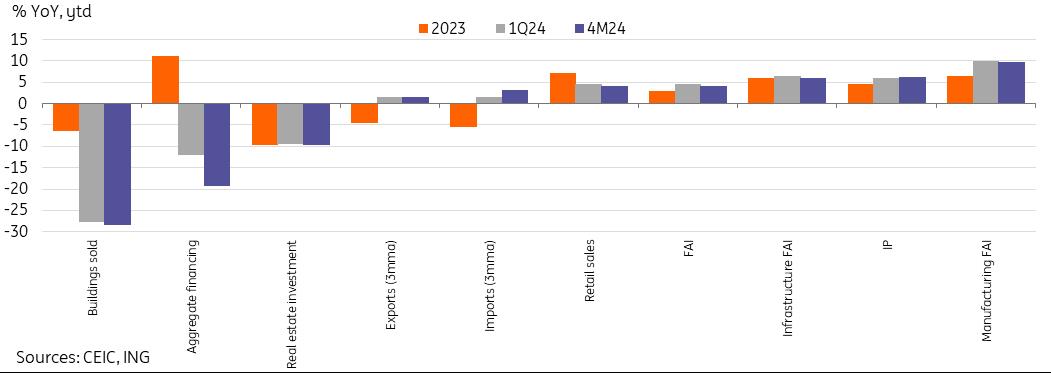

China activity monitor

Retail sales growth fell to a new post-pandemic low

April's data continued to show a shift away from consumption as a growth driver for 2024. April retail sales growth fell to 2.3% YoY, down from 3.1% YoY in March, bringing the year-to-date growth rate to 4.1% YoY.

The largest drag to retail sales in April was tied to auto sales, which declined -5.6% YoY, and the data may add fuel to the fire for the critics of China's overcapacity in this sector. Another major category, household appliances, also slowed to 4.5% YoY. As trade-in policies take effect later in the year, these categories could see some recovery. However, weakness in other categories including clothing (-2.0%), cosmetics (-2.7%), and gold & jewellery (-0.1%) show that many categories of discretionary consumption remain on the weak side.

On the bright side, we continued to see the "eat, drink, and play" theme outperform in April. Year-on-year growth for catering (4.4%), tobacco & liquor (8.5%), and sports & recreation (12.7%) outpaced headline growth. Consumers have been forgoing big-ticket purchases in favour of spending in these categories in 2024.

Consumption growth is likely to remain moderate through most of 2024, as consumer confidence remains downbeat amid tepid wage growth and the lingering negative wealth effects from the past several years of declining asset prices. A possible bottoming out of prices would also take some time before translating to stronger consumer activity.

Housing prices continued to slump as homebuyers remained cautious ahead of policy rollout

April's data showed that in the 70-city sample from China's National Bureau of Statistics, property prices continued to slide. New home prices fell by -0.58% MoM, and secondary market prices fell by -0.94% MoM, which were the steepest sequential declines since the start of the housing slump in 2021, down from -0.34% and -0.53% MoM growth respectively in March.

At the city level, 69 out of 70 cities continued to see declining prices in the secondary home market in April, unchanged from March. Ten of these cities experienced steep MoM declines between 1.5-1.8%. The new home market fared slightly better. Six out of 70 cities, including Shanghai and Tianjin, saw an uptick in new home prices. However, this was still a weaker performance than in March, when 11 out of 70 cities saw increased prices.

A recent flurry of supportive policy announcements including removing purchase restrictions, housing "trade-in" policies, and plans to directly purchase housing units for social housing programmes, has boosted market optimism that we will see a bottoming out of housing prices sometime this year. As these policies continue to roll out in the coming months, they should help to alleviate some of the downward pressure on property prices. With that said, data indicates that homebuyers may still be on the cautious side and some may remain on the sidelines until a trough is established. While it is arguably one of the most important signs of a stabilisation of sentiment in China, it is worth noting that a potential bottoming out of housing prices would only be the first step; elevated housing inventories will likely keep real estate investment suppressed for some time yet, and the property sector will remain a major drag on the economy this year.

Housing prices continued to slump in April Fixed asset investment unexpectedly moderated

Year-to-date fixed asset investment growth pulled back to 4.2% YoY, which was softer than expected. The key themes of 2024 for investment remained little changed.

First, infrastructure and manufacturing investment continued to lead the way. Infrastructure investment has grown by 6.0% YoY ytd, and manufacturing investment has grown 9.7% YoY ytd, both comfortably higher than the headline growth.

Second, investment growth remains heavily driven by the public side. Public sector investment rose 7.4% YoY ytd, while private sector investment slowed further to 0.3% YoY ytd, indicating that sentiment has yet to recover.

Third, real estate investment growth continued to disappoint forecasts. Real estate investment growth dropped to -9.8% YoY ytd, missing consensus forecasts for the third consecutive release. New housing starts remained in steep contraction at -24.6% YoY ytd. The real estate sentiment index has flattened in 2024, but continued to make new historical lows, reaching 92.02 in April.

However, we remain relatively optimistic that we could see an uptick in FAI in the months ahead. China is expected to begin issuance of the previously announced RMB 1tn of ultra-long-term bonds today. Though there are few firm details available on how the proceeds of this bond issuance will be used, given China's recent top-level policy direction to support growth stabilisation and develop key strategic industries for the future, fixed asset investment is likely to be one of the beneficiaries of the funds from the bond issuance being put to work.

Key themes for FAI continued in April Industrial activity the lone bright spot in April's data

The value added of industry rose to 6.7% YoY in April, up from 4.5% YoY in March, coming in notably stronger than forecasts. April's strong data brought year-to-date growth to 6.3% YoY, and industrial activity looks like it will be one of the main growth drivers in the second quarter of the year.

The transition toward high-tech manufacturing continues to be one of the major driving forces for industrial production. High-tech manufacturing grew 11.3% YoY in April, and 8.4% YoY over the first four months of the year. This was also reflected in the computers, communications and other electronic equipment category, which rose by 15.6% YoY in April and 13.6% YoY ytd.

Auto production also rebounded strongly, up to 16.3% YoY in April up from 9.4% YoY in March. Strong production growth but weaker domestic demand has translated to falling auto prices in the year to date.

An interesting distinction is that unlike FAI data, industrial production growth has been stronger in private enterprises. In April, private enterprise industrial production grew 6.9% YoY, outpacing the 5.4% YoY growth in state-owned enterprises.

China's industrial activity bucked the trend to beat forecasts in April Caution persists in China as growth stabilisation efforts continue

Overall, the data releases for April indicate that the caution entrenched over the past several years will take some time to recover. As the weakness of the earlier published credit data hinted, today's key activity data pointed to private-sector and household sentiment remaining downbeat and holding back overall growth. In 2024, growth will likely have to be driven by the public sector; fortunately, the policy rollout has begun, and the impact of supportive policies should gradually begin to trickle through the economy in the months ahead. There remains work to be done if China aims to hit its 5% growth target in 2024.

MENAFN18052024000222011065ID1108228607

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.