403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

US Mixed Manufacturing Messages Clouds The Outlook Ahead Of Powell

(MENAFN- ING) Surprise ISM drop shows manufacturing woes continue

Source: Macrobond, ING Data conundrum to continue as markets look to Powell and payrolls

We have had some surprisingly soft numbers out of the US this morning. The ISM manufacturing survey fell to 47.7 in February from 49.1 (consensus 49.5), contradicting the story told by the bulk of the regional manufacturing reports. That means we have had 16 consecutive months of sub-50 prints, which is the dividing line between expansion and contraction. The details show production contracted at its fastest rate since last July while new orders dropped back into contraction territory and the employment component dropped to 45.9, indicating some meaningful weakness – it has only been lower once (July last year) since the pandemic in 2020.

However, as with so much of the US data, there are contradictions and nuances within the report that are important. We see that 61% of industries reported rising new orders so that implies the weakness leading to a contraction in the main report mentioned earlier was especially concentrated in a small number of sectors. And while production fell, the proportion of industries reporting growth actually increased to 39% from 22%. Clearly there are winners and losers right now – the manufacturing sector is not performing uniformly.

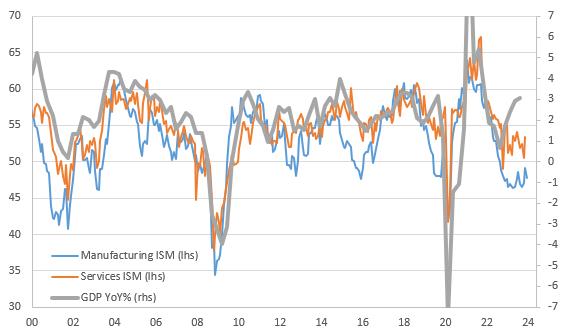

The chart below shows the relationship between GDP growth and the ISM surveys – the disconnect between official data and third party surveys is really wide, which makes forecasting any piece of data accurately incredibly challenging.

ISM surveys suggest the economy is weaker than official GDP growth data indicatesSource: Macrobond, ING Data conundrum to continue as markets look to Powell and payrolls

Meanwhile, construction spending fell 0.2% rather than rise 0.2% as predicted (although there was a 0.2 percentage point upward revision to December's spending). Residential construction spending rose 0.2%, but non-residential spending fell 0.4%, led by weakness in commercial buildings. We wouldn't be surprised to see construction struggle a little bit more in coming months given the recent rebound in borrowing costs.

Rounding out the numbers is the final reading of the February University of Michigan sentiment measure, which surprisingly fell to 76.9 from 79.6. Normally you don't get much of a change from the preliminary outcome to the final outcome so it perhaps hints at a sizeable dropping off in confidence in the second half of February. Market reaction to all of these data points has been rather muted though, which we attribute to the fact that we have Fed Chair Jerome Powell testifying before Congress next week on monetary policy and we also have publication of the February jobs report next Friday, which will be more critical for the outlook for rates. The consensus for payrolls is currently 190k, but this feels like a random number generator of a statistic right now. It contradicted pretty much every other labour indicator last month, hence why economists are clustering around the 6M rolling run rate for safety.

Author:James Knightley

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment