403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Germany's Economic Health Check Shows Further Signs Of Weakness

(MENAFN- ING) The debate over whether Germany is emerging as the 'sick man of Europe'

again has picked up steam once again over the summer. In our view, the answer is a resounding "yes”. However, the

pandemic, war in Ukraine and inflation are not the root cause of the country's economic problems

In this article A worrying economic health check German business model needs an overhaul More fallout from a lack of investment The consequences of an aging society

Supply chain frictions in the wake of the pandemic, the war in Ukraine and the energy crisis have only exposed pre-existing structural weaknesses in Germany's economy

Refinitiv, ING Research

Eurobarometer Spring 2023 and Eurobarometer Spring 2017

Refinitiv, ING Research

Eurostat, ING Research

Eurostat, ING Research More fallout from a lack of investment

OECD Broadband Portal The consequences of an aging society

German Statistical Office

ING Research

Refinitiv

Refinitiv

again has picked up steam once again over the summer. In our view, the answer is a resounding "yes”. However, the

pandemic, war in Ukraine and inflation are not the root cause of the country's economic problems

In this article A worrying economic health check German business model needs an overhaul More fallout from a lack of investment The consequences of an aging society

Supply chain frictions in the wake of the pandemic, the war in Ukraine and the energy crisis have only exposed pre-existing structural weaknesses in Germany's economy

Weak growth, worsening sentiment, and pessimistic forecasts have brought back headlines and public discussion over one key theme over the last few months: whether Germany is once again the 'sick man of Europe'. The Economist reintroduced the debate this summer more than two decades after its groundbreaking front page. The infamous headline certainly seems justified when looking at the current state of the German economy.

A worrying economic health checkMore than 10 years ago, Germany was celebrating its Wirtschaftswunder 2.0 and grew by 2.1% on average per year between 2010 and 2015. The eurozone – excluding the German economy – grew by only 0.8% on average per year over the same period. Between 2016 and 2022, however, other eurozone economies picked up speed and Germany lost momentum. GDP growth in the monetary union (excluding Germany) was 1.7% on average per year between 2016 and 2022, compared with an average GDP growth per year of 1.1% in Germany.

Average GDP growth (%)Refinitiv, ING Research

Currently, cyclical headwinds like the still-unfolding impact of the European Central Bank's monetary policy tightening and high inflation – plus the stuttering Chinese economy – are being met by structural challenges like the energy transition and shifts in the global economy, alongside a lack of investment in digitalisation, infrastructure and education. To be clear, Germany's international competitiveness had already deteriorated before the Covid-19 pandemic and the war in Ukraine.

To a large extent, Germany's issues are homemade. Supply chain frictions in the wake of the pandemic, the war in Ukraine and the energy crisis have only exposed these structural weaknesses. These deficiencies are the flipside of fiscal austerity and wrong policy preferences over the last decade.

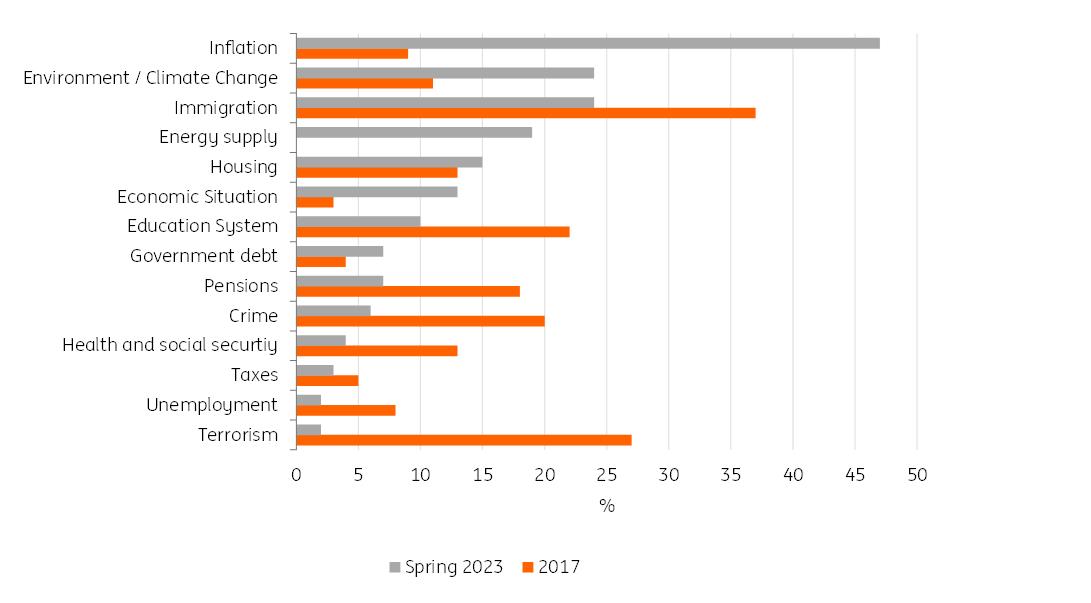

Most important issues Germany faces at the moment (%)Eurobarometer Spring 2023 and Eurobarometer Spring 2017

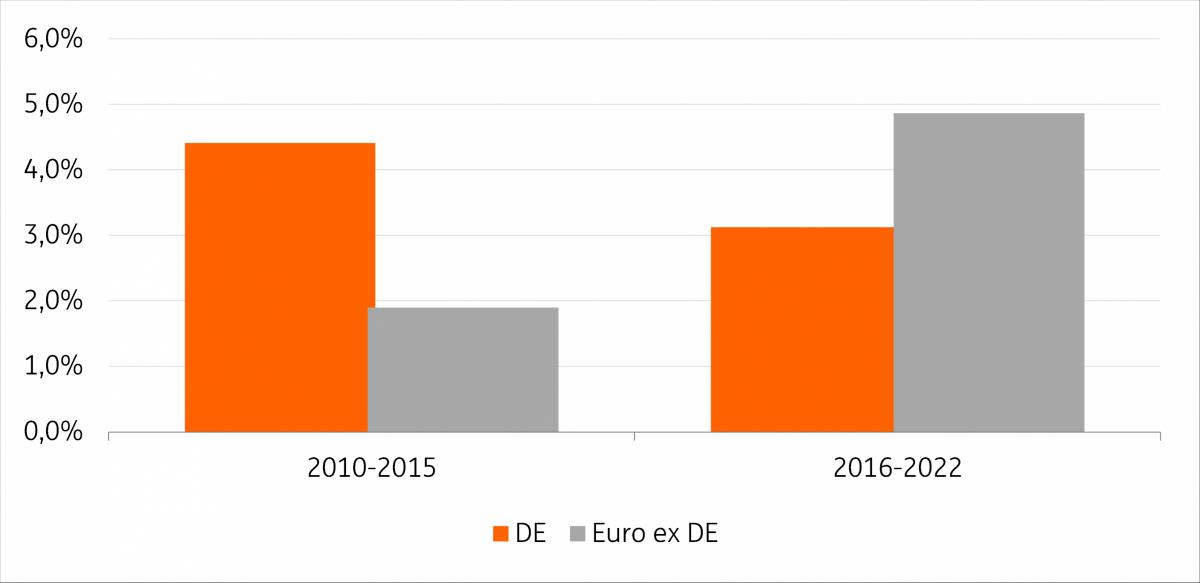

Germany's low level of investment activity in recent years is evidence of the fact that the country has long rested on its functioning business model of importing cheap energy and exporting goods. While fixed capital investment in Germany grew by an average of 4.4% per year between 2010 and 2015, growth was only 3.1% between 2016 and 2022.

Average growth of investment in equipment and machinery (%)Refinitiv, ING Research

Just like the economic growth story, the picture elsewhere in the eurozone looks quite the opposite. Excluding Germany, the eurozone's fixed capital investments grew by an average of 1.9% per year between 2010 and 2015. In the years 2016-2022, average investment growth per year was 4.9%.

German business model needs an overhaulThe structural transitions the economy is facing will come at a cost. Just think of energy-intensive production. In the production of food, beverages and tobacco, for example, more than half of the total energy consumption is covered by natural gas. Such a large share of consumption is met by renewable energy sources only in the manufacturing of wood and wood products. The shift from natural gas production to greener forms of production will initially come with productivity losses and, as a result, cause products to become more expensive.

Share of energy sources in total energy consumption per industrial sector (as of 2021)Eurostat, ING Research

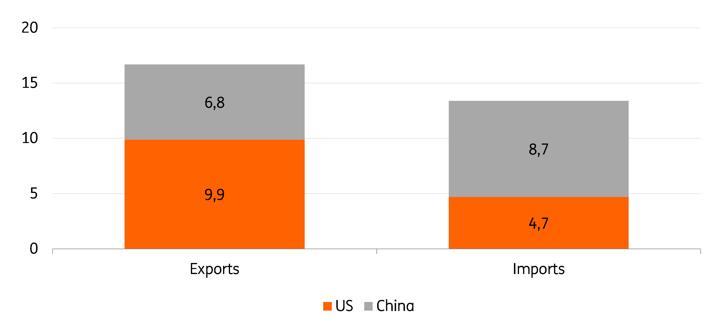

The good old growth driver, exports, is also stuttering. On the one hand, China's economic weakness and the expected economic downturn in the US are a burden on German exports. If both of its main trading partners are not doing well economically, this automatically does not bode well for German trade. Secondly, the globalised world as we know it will change. This does not necessarily mean deglobalisation, but rather that trade flows will change. Be it supply chain disruptions in recent years or geopolitical tension, there is certainly a case for diversifying trading partners more and, if possible, bringing production closer to home. However, this development will also be accompanied by efficiency losses and higher prices.

Share of China and the US in Germany's total international trade in goods (in % of total exports and imports, respectively, 2022Eurostat, ING Research More fallout from a lack of investment

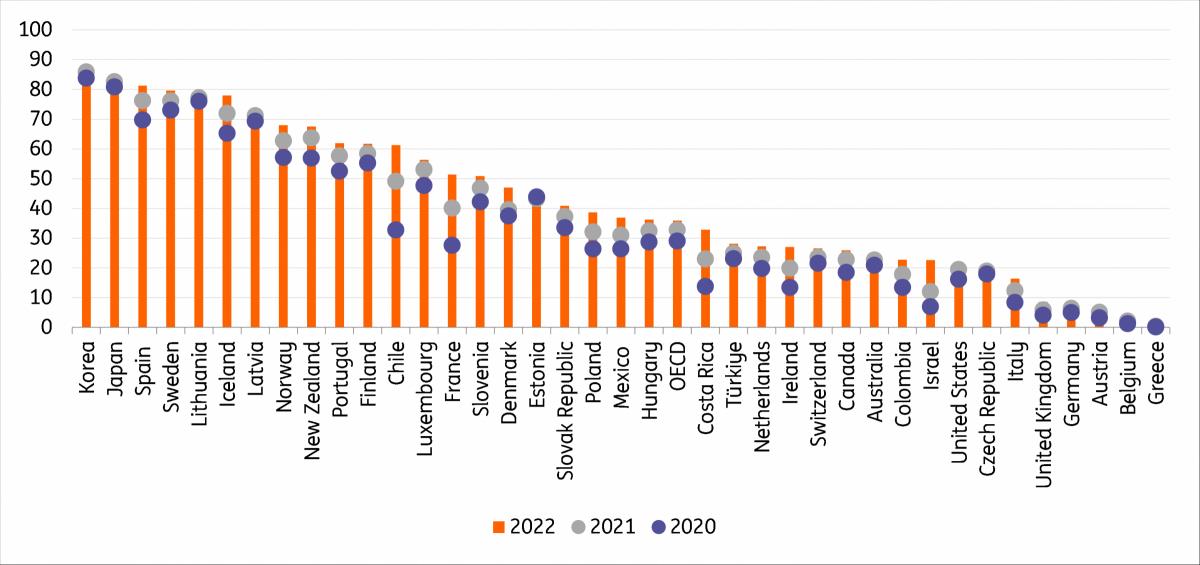

The general lack of investment is reflected in crumbling infrastructure. The quality of German roads has been rated worse and worse by various indices since 2010, and digital infrastructure in Germany remains in need of improvement as well. Fibre connections, or high-speed Internet, only accounted for some 8% of total German broadband connections in 2022. The OECD average in the same year was 36%.

Share of fibre connections in total broadband subscriptions (%)OECD Broadband Portal The consequences of an aging society

Demographic change will also structurally weigh on the German economy in the coming years. By 2060, the German working population could shrink up to around 25% compared with 2019. Assuming high labour market participation and high net migration, the loss would still be 5%.

Labour force projection (persons aged 15-74)German Statistical Office

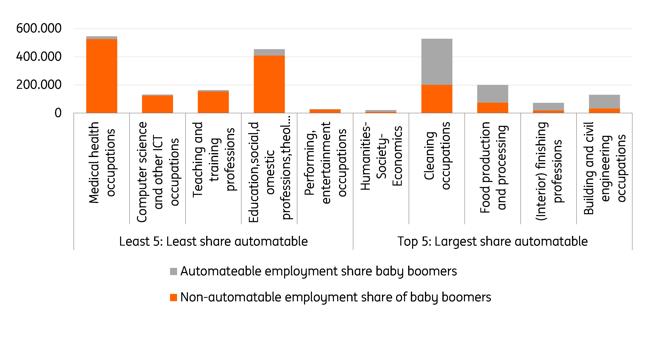

Particularly over the next 12 years as the baby boomer generation retires from the German labour market, the shortage of skilled workers in Germany will become much more severe. However, in addition to labour market migration, another factor which could help to fill the gap in the German jobs market is automation. Nearly 80% of baby boomers currently employed in humanities and social sciences could be replaced by fellow robots. In the cleaning profession, more than 60% of employees aged over 55 could be replaced by automation.

Least 5 & top 5 automatable employment share baby boomers per professional groupING Research

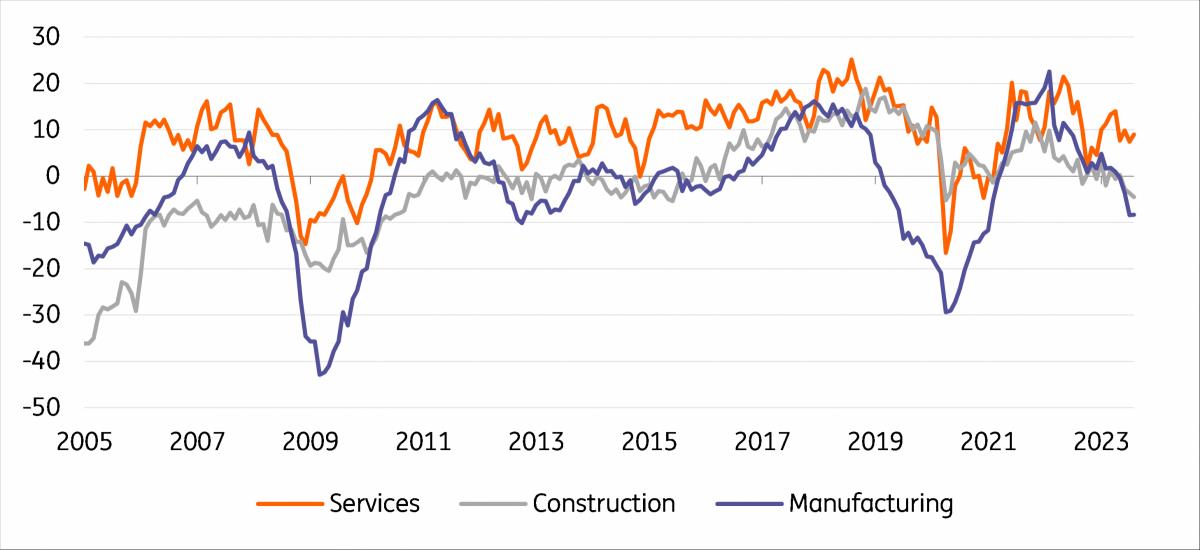

They say a real crisis only shows in the labour market. With a seasonally adjusted unemployment rate of just 5.7%, the German labour market is holding up very robustly. Beneath the surface, however, the first effects of the tense economic situation are beginning to show. For roughly a year now, the number of job postings has been declining, and companies' employment expectations are also slowly becoming much more gloomy. For the time being, it is therefore likely that labour unions will increasingly argue for job security rather than strong wage increases.

Ifo employment expectations (net balance)Refinitiv

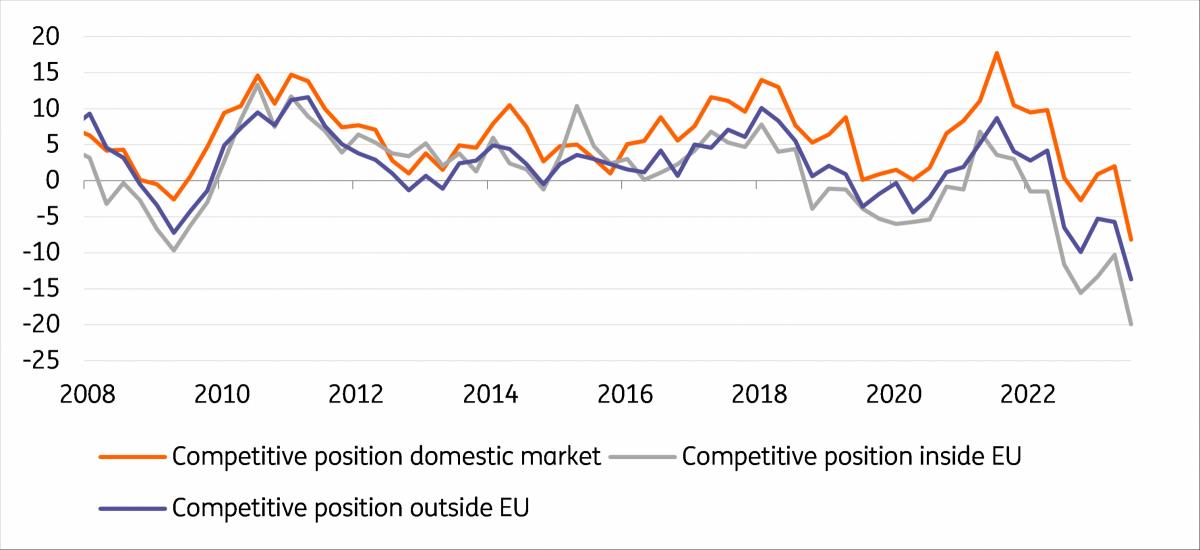

Taking all the above findings into account, it is clear that the German economy – like a patient that has not taken good care of itself over the last decade – is now paying the price for too little maintenance work. As a result, the country has lost international competitiveness in almost every single ranking. In the European Commission's latest industrial survey, for example, more companies than ever before stated that they expect Germany's competitive position to deteriorate – both within and outside of the EU.

European Commission industry survey, competitive position of GermanyRefinitiv

Germany has shown regularly in the past that it can master crises. At the current juncture, however, the remedy for the country's current economic problems is not a simple one. It requires a long list of policy measures, structural reforms and investments to bring the economy back to full speed. More than twenty years ago, it took around five years between the first diagnosis and the beginning of serious structural reforms. Let's hope that it will be less this time around.

Author:Carsten Brzeski, Franziska Biehl

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment