(MENAFN- ING)

The Russia-Ukraine war has exacerbated the market dislocation between London and Shanghai. As we have pointed out before, the China market has been on the soft side post-Chinese New Year due to weaker seasonal demand, and more recently the Covid outbreaks have forced some traders to maintain a wait-and-see approach, which has weighed on the prices in Shanghai market. On the other hand, however, the war continues to disrupt the supply chain as self-sanctioning put in place by supply chain participants, from banks to shippers, has further tightened the physical liquidity on top of an already-stretched market. Subsequently, the world market, excluding China, has continued to tighten, reflected in the rising physical premium from Europe to the North American markets.

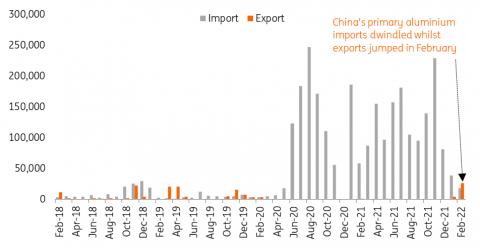

The market dislocation has temporarily redrawn the trade landscape which previously saw China as an importer of primary aluminium. The latest trade data for the first two months of this year provide some evidence. Reversing the strong imports over the last two years, China's exports of primary aluminium jumped to more than 30kt during the first two months, compared to only 1.6kt during the same period of 2021.

China primary aluminium exports jump in February (tonnes)

China Customs, ING

However, exported primary aluminium is likely due to opportunistic selling, and this is not homemade Chinese aluminium. This aluminium is believed to be pre-imported ingots sitting in the Chinese bonded warehouses, which are exempt from China's export tax when they leave the bonded zones. Therefore, instead of waiting for the opportunity to enter the Chinese domestic market, they are now incentivised to take advantage of the physical reverse arbitrage in other markets.

As for the domestic primary metal, it would need a further incentive to spur exports, bearing in mind the 15% export tax on top of the pricing. In other words, this would need the London Metal Exchange (LME) market to further outperform the Shanghai Futures Exchange (ShFE), or physical premiums to rise further.

For the time being, the base case here is that China imports may remain subdued, but massive exports of domestic ingots seem less likely. However, should Russian aluminium be further disrupted due to either self-sanctioning or curtailment at Rusal due to raw material shortages, that could take out up to four million tonnes of supply, and spur market dislocation, thus attracting some Chinese exports to fill the gap.

Meanwhile, we think the current market dynamics should encourage China's exports of semis and aluminium products, supporting domestic demand.

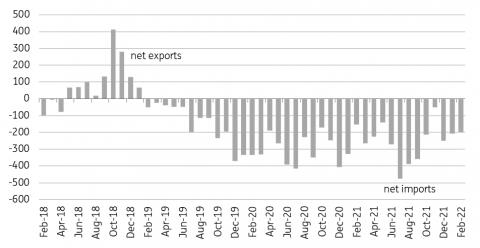

China alumina net im/exports (tonnes)

China Customs, ING

China is a net importer of alumina, though there are precedents when exports surge amid market dislocations incentivising exports.

The raw material market is also full of uncertainty. We noted earlier that the physical market alumina liquidity has started to shrink. The risks rose further after Australia banned exports to Russia, leaving Rusal little room to manoeuvre in seeking alternative alumina feed to fill the gap. Such a ban only adds to the risks of production curtailment in Russia. Exports of alumina from China are possible, as seen back in 2018, but any potential spike in exports is unlikely to be sustained. As Chinese smelters seek steady restarts to take advantage of the decent margins right now, their demand for alumina is poised to rise, supporting the raw material's pricing in the onshore market.

MENAFN23032022000222011065ID1103902189

Author:

Wenyu Yao

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.