403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Eurozone Economy Sees Glimmers Of Hope

(MENAFN- ING)

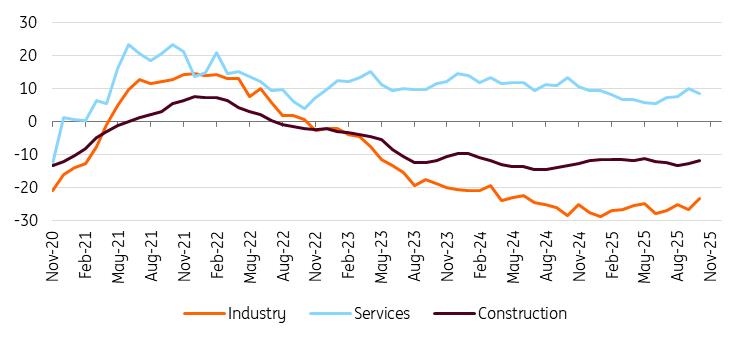

Signs of resilience

Source: LSEG Datastream Inflation near target

While it would be preposterous to speak of an economic boom in Europe, the eurozone economy has shown more resilience than anticipated despite multiple headwinds. US tariffs and a strong euro continue to weigh on exports, while Chinese imports are squeezing profit margins. Yet, eurozone GDP grew by 0.2% quarter-on-quarter in 3Q. Both the PMI and the European Commission's sentiment indicators improved in October, pointing to a continued recovery in the fourth quarter.

To be sure, Germany remains lacklustre, with third-quarter stagnation, while France posted a surprisingly solid 0.5% quarterly growth rate, though looming budgetary constraints could become a drag in 2026.

Industry nearing a turning pointServices activity is expanding, supported by consumer spending on tourism and hospitality, and boosted by IT services growth linked to rising AI investment and further digitalisation. Industrial activity is still subdued, but capacity utilisation has been trending upward throughout the year. Energy costs remain a competitive disadvantage, albeit less severe than before, now that both oil and natural gas prices have been trending lower. Without supply issues, which are still a short-run threat, industry should have bottomed out. Construction is showing signs of recovery, driven by stronger mortgage demand despite slightly higher long-term rates.

But for the eurozone economy to gain real momentum, German infrastructure spending will be key, and that's only likely to kick in from the second half of next year. We forecast 1.4% GDP growth in 2025 and a gradual quarterly acceleration next year. However, adverse base effects mean 2026 growth will likely average 1.1%.

Order books are bottoming outSource: LSEG Datastream Inflation near target

Headline inflation eased to 2.1% in October, close to the ECB's target. Core inflation remains sticky at 2.4%, driven by services inflation at 3.4%. However, selling price expectations in the services sector suggest easing pressures over the next six months. At the same time, wage growth is moderating and energy prices are declining. We expect inflation to fall below 2% in the coming months and remain there through 2026, with a slight uptick possible in 2027.

The ETS2 scheme, which was set to raise heating and transport costs from 2027, has been delayed until 2028. Its impact should be muted, as the European Commission has suggested that safeguards will limit its effects on consumers.

The ECB's good place is becoming a permanent residenceThe European Central Bank kept rates unchanged in October, reaffirming it is in“a good place”. With inflation near target and downward growth risks dissipating, according to President Lagarde, policymakers see little reason to change their current stance. Market pricing still sees a small chance of a 25bp cut by mid-2026, but this would probably require a faltering growth story, severe financial stress or a further strong appreciation of the euro.

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment