403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Strong Tokyo CPI Will Likely Put Pressure On The Bank Of Japan

| 3.3% | Tokyo consumer prices

%YoY |

| Higher than expected |

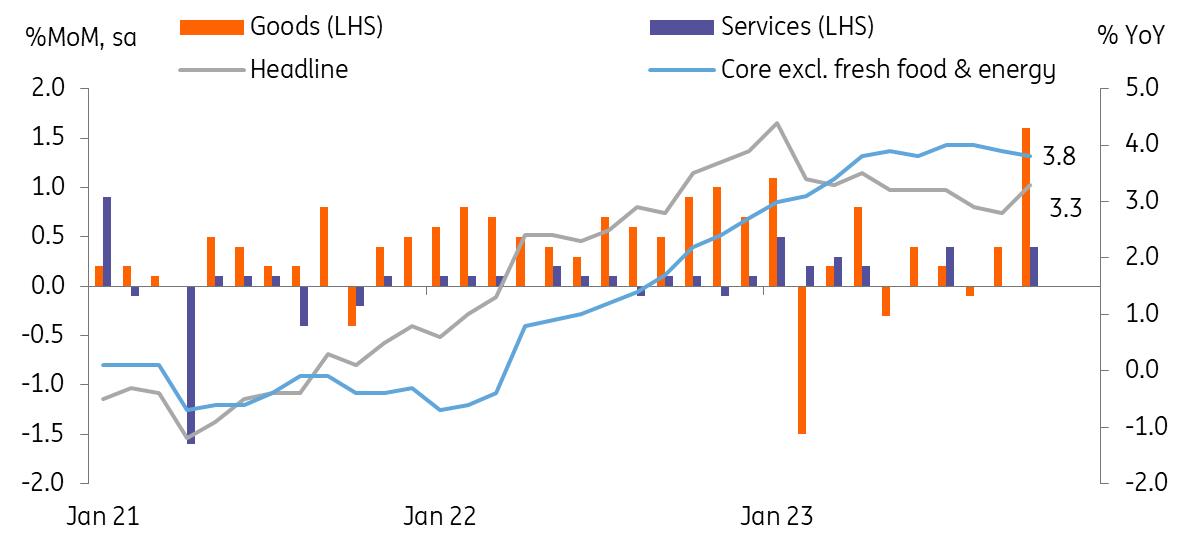

Tokyo inflation climbed up to 3.3% YoY in October (vs 2.8% in September, market consensus). Upside surprises came from:

- Higher than expected pick up in utilities with a reduction of government subsidies and A solid rise in entertainment prices.

More importantly, the BoJ's preferred measures of inflation, core CPI excluding fresh food (2.7% vs 2.5% in September & market consensus) and core-core CPI excluding fresh food and energy (3.8% vs revised 3.9% in September, 3.7% market consensus) came out higher than market consensus. Since Tokyo inflation is a leading indicator for nationwide inflation, today's readings showed that inflation has been clearly overshooting the BoJ's projections.

On a monthly comparison, CPI soared 0.9% MoM, seasonally adjusted, in October, with both goods and services prices rising by 1.6% and 0.4% each.

Tokyo's inflation reaccelerated in October

CEIC

Utilities and fresh food prices rose the most, but prices of all other major items gained. In particular, the weak JPY has accumulated pressure on the imported goods prices, and this prolonged pressure pushed up prices of household goods, apparel, and transportation. The rise in entertainment is mostly driven by strong demand from foreign and domestic tourists.

Going forward, we expect that base effects will kick in and suppress the headline inflation again by the end of the year, but we will likely witness a stickier than expected inflation trend throughout next year.

Overheated inflation is a risk for the recoveryToday's hotter-than-expected Tokyo CPI reading will likely be a warning to the Bank of Japan. It may still rule out a policy change at its October meeting, but at least we expect the BoJ to change its view on inflation.

It is clearer that companies are shifting the pressure of rising input costs to consumers, and the weak JPY is partially contributing to the added pressure on input costs. Also, demand-led price hikes continued on the back of a solid recovery in service activity despite a fall in real wage growth. But, if the yen weakens further and brings about overly heated inflation for longer, it will eventually hamper private consumption even before the BoJ's long-awaited goal of sustainable inflation is accomplished, which is the biggest risk for the BoJ.

We are sticking to our call that the BoJ will deliver a policy tweak and revise the inflation outlook meaningfully for FY 23 and 24. And today's outcome has slightly increased our confidence in our non-consensus view. There are more details about the BoJ's next moves in our article earlier this week; find it here .

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment