403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Advanced Space Composites Market Size, Share, Growth, Analysis, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

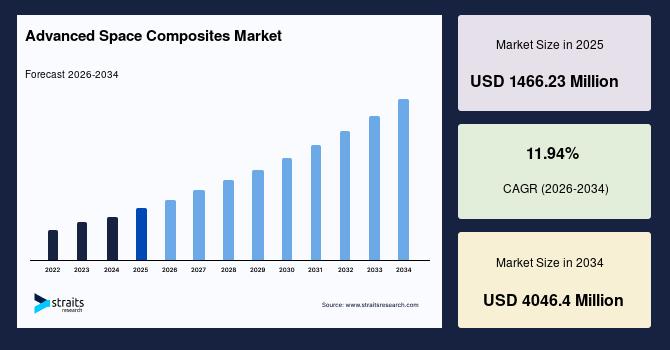

| 2025 Market Valuation | USD 1466.23 Million |

| Estimated 2026 Value | USD 1641.29 Million |

| Projected 2034 Value | USD 4046.4 Million |

| CAGR (2026-2034) | 11.94% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Europe |

| Key Market Players | RUAG Group, Toray Advanced Composites, Hexcel Corporation, Airbus S.A.S, Boeing |

Download Free Sample Report to Get Detailed Insights.

Advanced Space Composites Market Dynamics Market DriversGrowing Satellite Launches and Space Exploration Missions and Rising Need for Lightweight, Fuel-Efficient Spacecraft Design Drives Market

The increasing number of satellite constellations for communication, earth observation, and navigation is driving strong demand for lightweight and high-strength composite materials. Government space agencies and private players are expanding lunar, Mars, and deep-space missions, which require materials capable of withstanding extreme thermal and mechanical stress. Advanced composites are preferred due to their high strength-to-weight ratio and radiation resistance. This surge in launch activity is significantly boosting consumption of space-grade composite structures.

Space missions increasingly focus on reducing launch weight to lower fuel consumption and mission costs. Advanced composites such as carbon fiber-reinforced polymers are replacing traditional metals in spacecraft structures, satellite panels, and propulsion components. These materials offer high durability while significantly reducing overall spacecraft mass. As space agencies and private companies prioritize efficiency and payload optimization, demand for advanced space composites continues to grow rapidly.

Market RestraintsLimited Availability of Space-grade Raw Materials and Complex Fabrication & Precision Engineering Requirements Restrain Market

Advanced space composites require highly specialized carbon fibers, resins, and ceramic-based materials that are produced by a limited number of global suppliers. Strict quality and performance requirements for space applications further narrow the pool of approved raw material sources. Any disruption in supply or export restrictions can significantly affect production timelines and material costs. This limited availability creates procurement challenges and increases dependency on specialized supply chains.

Manufacturing advanced space composites involves highly precise fabrication processes to ensure structural integrity, thermal stability, and weight optimization. Even minor defects such as voids, delamination, or fiber misalignment can compromise spacecraft performance in extreme space conditions. The need for specialized equipment, cleanroom environments, and skilled engineering expertise increases production complexity and operational costs. These technical issues can extend manufacturing timelines and limit scalability for composite manufacturers.

Market OpportunitiesIncreasing Commercialization of Private Space Programs and Increasing Adoption of Reusable Launch Vehicles & Next-Generation Spacecraft Opens New Growth Avenues

The rapid expansion of private space companies and low-earth-orbit satellite constellations is creating strong demand for lightweight, high-strength composite materials. Commercial operators are increasingly seeking advanced composites to reduce launch weight, improve payload capacity, and enhance fuel efficiency. Rising investments in communication, earth observation, and broadband satellite networks are accelerating spacecraft production volumes. This presents major opportunities for manufacturers specializing in space-grade composite structures and components.

The shift toward reusable launch systems is driving demand for highly durable composite materials capable of withstanding repeated thermal and mechanical stress. Advanced composites are increasingly being used in launch vehicle structures, propulsion systems, and thermal protection components to improve performance and reduce operational costs. Space agencies and private launch providers are investing heavily in next-generation spacecraft technologies focused on efficiency and reusability. This trend is creating significant opportunities for innovation in high-performance composite manufacturing and engineering.

Market ChallengesRising Geopolitical Restrictions and High Dependency on Government Space Budgets & Funding Challenges Advanced Space Composites Market Growth

The advanced space composites market is increasingly affected by geopolitical tensions, export control regulations, and trade restrictions related to aerospace materials and technologies. Restrictions on the cross-border supply of carbon fibers, specialty resins, and defense-grade materials can disrupt global procurement and manufacturing operations. Companies operating in international space programs may also face delays in technology transfer approvals and collaborative projects. These geopolitical uncertainties create supply chain instability and increase operational risks for manufacturers.

A significant portion of demand for advanced space composites is tied to government-funded space exploration, defense, and satellite programs. Changes in political priorities, budget reallocations, or delays in public funding can directly impact spacecraft production and material procurement. Many long-term projects depend on continuous government investment, making market growth vulnerable to policy and economic fluctuations. This dependency creates uncertainty for manufacturers planning capacity expansion and long-term R&D investments.

Regional AnalysisNorth America's advanced space composites industry share is expected to grow at a CAGR of 11.46% over the forecast period. One of the major factors for the substantial growth in the market in the region is the growing satellite constellations that will be launched in the next 10-15 years. The presence of major advanced composite providers such as Lockheed Martin, Northrop Grumman, Toray Advanced Composites, and Hexcel Corporation within the region and space exploration programs by government and military players are also creating market opportunities. Additionally, the National Aeronautics and Space Administration (NASA) and other space companies have been using advanced composites on satellite systems and space launch vehicle structures. In July 2021, NASA's Langley Research Center, in partnership with NASA Ames Research Center, NanoAvionics, and Santa Clara University's Robotics Systems Lab, developed a deployable lightweight composite boom and solar sail system for the Advanced Composite Solar Sail System (ACS3) mission. This will be the first-time composite booms are used for a solar sail in orbit. Such factors are anticipated to boost market growth in the region.

Europe is anticipated to exhibit a CAGR of 12.92% over the forecast period. The European region's space sector is highly driven by the presence of one of the leading national space agencies, the European Space Agency (ESA), and the European Commission, apart from the commercial space companies operating in this region. The European Space Agency (ESA) introduced the SpaceCarbon project under the Horizon 2020 Programme. This project aims to develop European-based carbon fibers (CF) and pre-impregnated materials for launchers and satellite applications. This will enable a European supply chain that can reduce the dependency of the European Space sector on this critical Space technology, hence reducing the risk of stopping future space programs due to supply restrictions and shortage of these materials from non-European sources, thereby driving the market growth.

The space sector in Asia-Pacific is significantly growing as the region's major economies have been gradually accelerating toward a strong growth pattern, along with economic booms in Asia-Pacific countries such as Australia, Singapore, Indonesia, Malaysia, and Thailand. Countries in this region are increasingly producing small satellite constellations, which will enable satellite-based services. The region also has a committed forum, the Asia-Pacific Regional Space Agency Forum (APRSAF), which was established in 1993 to increase space activities in the Asia-Pacific region. Other Asia-Pacific countries such as Australia, Singapore, and Vietnam are developing and enhancing their space capabilities, from building launch vehicles to satellite manufacturing. However, the countries in the APAC region only have a small number of satellites in space, except for China. Therefore, the market share of the region at the global level could be higher, which has hindered the growth of the market.

Rest-of-the-World includes countries such as Brazil and the U.A.E. The space industry in Rest-of-the-World countries has yet to fully develop compared to powerful nations such as the U.S. and the U.K. Hence, the demand for advanced composites may be low compared to other regions. However, these countries are focusing on technological advancements to build a fleet of satellites enabling Earth observation, technological developments, and communication-based applications, driving market growth.

Advanced Space Composites Market Segmentation Analysis By PlatformBased on the platform, the global market is divided into satellites, launch vehicles, and deep space probes and rovers. The satellite segment is the most significant contributor to the market and is estimated to exhibit a CAGR of 12.76% over the forecast period. Satellites are usually used for communication, navigation, and tracking and are primarily placed in the Earth's orbit. There is an extensive demand for LEO-based satellite constellations in the market owing to the increasing need for faster, reliable, and efficient real-time tracking and monitoring, real-time Earth observation (EO), navigation, communication, and technology demonstration. This growing LEO-based satellite mega constellation is one of the significant factors that may contribute to the demand for advanced composites. The satellite segment is further sub-segmented into small satellites (0-1,200kg), medium satellites (1,201-2,200kg), and large satellites (above 2,200kg).

By ComponentsBased on components, the global market is bifurcated into payloads, structures, antennae, solar array panels, propellent tanks, spacecraft modules, sunshade doors, thrusters, thermal protection, and others. The structures segment dominates the global market and is projected to grow at a CAGR of 14.12% over the forecast period. Space structures or frames for satellites and launch vehicles comprise several advanced composites. For instance, aluminum matrix composites are used for satellite structures, and aluminum-carbon-reinforced plastic laminates are used in the satellite structure assembly. These offer a 33% weight reduction in the satellite structure assembly compared to their metallic counterparts. In launch vehicle structure, some companies use carbon-silicon carbide composites in disc brakes, jet vanes of nozzles, engine flaps, and nose caps of launch vehicles.

By MaterialsBased on materials, the global market is bifurcated into fiber, resin, nanomaterials, ceramic matrix composites (CMC) and metal matrix composites (MMC), and others. The fiber segment owns the highest market share and is predicted to grow at a CAGR of 11.60% over the forecast period. In terms of fiber types, the global market has been categorized into carbon fiber and glass fiber. These fibers are used in space applications such as satellites and launch vehicles. For instance, in 2019, as part of the European Space Agency's (ESA) Clean Space initiative, a magnetotorquer was designed to interact magnetically with Earth's magnetic field to shift satellite orientation. It was kept in a plasma wind tunnel at the German Aerospace Center's (DLR) facility, then reproduced re-entry conditions, melting it into vapor. This magnetotorquer was made of an external carbon fiber reinforced polymer composite with copper coils and an internal iron-cobalt core.

By Manufacturing ProcessesBased on manufacturing processes, the global market is divided into automated fiber placement (ATL/AFP), compression molding, additive manufacturing, and others. The compression molding segment is the highest contributor to the market share and is anticipated to exhibit a CAGR of 11.8% during the forecast period. Compression molding is the process of molding wherein a preheated polymer is positioned into an open, heated mold cavity. The mold is then closed with a top plug and compressed to have the material contact all areas of the mold. This molding procedure is suitable for fabricating complicated, high-strength composite structures of carbon fiber, aramid fiber, or fiberglass in uniform numbers. Aircraft and space will remain significant sources of compression-molded composite parts applications.

By ServicesBased on services, the global market is divided into repair and maintenance, manufacturing, and design and modeling. The manufacturing segment dominates the global market and is expected to exhibit a CAGR of 11.76% over the forecast period. Composites have become part and parcel of the manufacturing of space systems. As such, several companies provide their advanced composite manufacturing capabilities for space applications. For instance, Applied Composites has five facilities that are engaged in the development of advanced composites. These facilities are in California (U.S.) and Indiana (U.S.). These facilities focus on developing high-quality materials and structures technology, product development, testing services, and producing spacecraft parts for the aerospace and defense sector.

Competitive LandscapeThe advanced space composites market is moderately consolidated at the top but highly fragmented overall, with global aerospace OEMs, defense contractors, specialized composite material manufacturers, and advanced materials startups competing across spacecraft, satellite, and launch vehicle applications. Established players compete primarily on advanced material R&D capabilities, high-performance structural engineering, space-grade certification compliance, long-term contracts with space agencies, and integration with aerospace manufacturing ecosystems. Emerging players focus on lightweight composite innovation, rapid prototyping, niche material specialization, and cost-efficient production methods, especially for small satellite and commercial space applications. Competition is increasingly driven by deep materials science innovation and integration with digital engineering tools.

List of Key and Emerging Players in Advanced Space Composites Market-

RUAG Group

Toray Advanced Composites

Hexcel Corporation

Airbus S.A.S

Boeing

GomSpaceA/S

HyPerComp Engineering

Infinite Composites Technologies

Matrix Composites Applied Composites

Airborne

CST Composites

Peak Technology

ACPT Inc.

AdamWorks, LLC.

December 2025, Airbus completed the acquisition of selected Spirit AeroSystems industrial assets linked to its aircraft programs. These assets include production for A220 wings (Belfast), A350 fuselage sections, A320/A350 structural components, and A220 components across multiple sites.

October 2025, Teijin Limited and A&P Technology introduced the IMS65 PAEK bimax braided composite fabric in Oct 2025 for high-performance aerospace and space structural applications.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1466.23 Million |

| Market Size in 2026 | USD 1641.29 Million |

| Market Size in 2034 | USD 4046.4 Million |

| CAGR | 11.94% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Platform, By Component, By Material, By Manufacturing Process, By Service |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Advanced Space Composites Market Segments By Platform-

Satellite

Launch Vehicles

Deep Space Probes and Rovers

-

Payloads

Structures

Antenna

Solar Array Panels

Propellent Tank

Spacecraft Module

Sunshade Door

Thrusters

Thermal Protection

Others

-

Fiber

Resin

Nanomaterials

Ceramic Matrix Composites (CMC) and Metal Matrix Composites (MMC)

-

Automated Fiber Placement

Compression Molding

Additive Manufacturing

Others

-

Repair and Maintenance

Manufacturing

Design and Modeling

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment