403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Plumbing Component Market Size, Share & Trends Report By 2034

| Timeline | Company | Activity | Focus | Value |

|---|---|---|---|---|

| January 2025 | Infra | Pre-IPO funding round | Expansion of construction materials business including pipes, fittings, plumbing components, and manufacturing operations | USD 121 million |

| January 2025 | Captain Pipes Limited | Private placement financing | Expansion of UPVC and CPVC plumbing pipes and fittings manufacturing operations | Not publicly disclosed |

| June 2025 | Ganga Bath Fittings Ltd. | IPO funding | Capital expenditure for plumbing and bath fitting equipment, machinery purchase, and working capital expansion | USD 2.1 million |

| June 2025 | Brasscraft Engineering Private Limited | Strategic capital investment | Expansion of brass plumbing fittings and sanitary fittings manufacturing | USD 0.0012 million |

| Market Metric | Details & Data (2025-2034) |

|---|---|

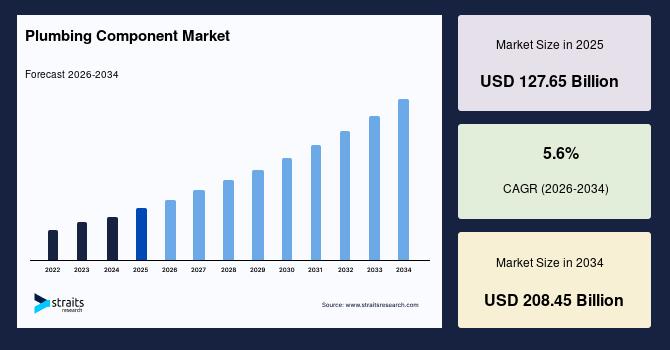

| 2025 Market Valuation | USD 127.65 Billion |

| Estimated 2026 Value | USD 134.8 Billion |

| Projected 2034 Value | USD 208.45 Billion |

| CAGR (2026-2034) | 5.6% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Aalberts N.V. (Netherland), Central States Industrial (US), Finolex Industries Ltd. (India), McWane Inc. (US), Morris Group Acorn (US) |

Download Free Sample Report to Get Detailed Insights.

Plumbing Component Market Dynamics Market DriversIncreasing Demand for Leak-resistant Plumbing Installations and Rising Adoption of Water-efficient Sanitary Systems Drives Market

The growing focus on building durability is pushing higher demand for plumbing systems that reduce leakage risks. Construction projects now prioritize strong sealing materials and advanced jointing methods to prevent water loss. Urban areas face higher pressure on water supply networks, which increases the need for reliable piping systems. The US Environmental Protection Agency (EPA) WaterSense program highlights the household leaks that can waste nearly 10,000 gallons of water annually in an average home, encouraging the use of efficient plumbing components to reduce water loss.

Water scarcity concerns are driving stronger adoption of water-efficient sanitary systems across residential and public infrastructure. Governments and urban planners are encouraging the use of low-flow faucets, dual-flush toilets, and sensor-based systems to reduce water consumption. These systems are becoming a standard feature in modern building designs due to sustainability goals, significantly driving plumbing component market growth.

Market RestraintsVolatile Raw Material Prices and Susceptibility of Low-grade Components to Water Pressure Damage Restrain Market Growth

Fluctuations in the prices of key raw materials such as metals (brass, copper, and stainless steel) and plastics used in plumbing components create significant cost uncertainty for manufacturers. These price variations impact production planning, squeeze profit margins, and make it difficult to maintain stable pricing for end products. As a result, manufacturers may face challenges in long-term contract commitments and inventory management, while customers may delay purchases due to price instability, thereby restraining the growth of the plumbing component market.

Low-grade plumbing components often show poor resistance when exposed to continuous or high water pressure conditions. Inferior materials and weak manufacturing standards can lead to leaks, cracks, or early product failure in water distribution systems. This creates maintenance challenges for residential and commercial infrastructure where consistent water flow is required. Repeated pressure stress reduces the lifespan of fittings and pipes, increasing replacement frequency.

Market OpportunitiesAdoption of Smart Water Management Systems and Expansion of IoT-enabled Leak Detection Systems Offer Growth Opportunities for Market Players

Smart water management systems are increasingly being integrated into modern building infrastructure to improve efficiency and reduce wastage. Building developers are adopting automated water control technologies that monitor usage patterns in real time and help optimize water distribution across residential and commercial spaces with better precision. Digital meters and connected control units support data-driven decision-making for facility managers. Energy-efficient building certifications are also encouraging the use of smart water solutions in new construction projects.

IoT-enabled leak detection systems are gaining importance as buildings move toward smarter and safer water infrastructure. These systems continuously monitor pipelines and alert users to leakage or abnormal water flow in real time. Early detection helps reduce water loss, property damage, and maintenance costs in residential and commercial properties. Building owners are increasingly investing in connected sensors to improve system reliability and operational control. Integration of mobile alerts and cloud-based dashboards further enhances response speed during water-related faults.

Market ChallengesComplex Compliance with Building Regulations and Shortage of Skilled Workforce Act as Challenges in Plumbing Component Market

Plumbing component manufacturers face continuous challenges in meeting changing regional construction codes, water efficiency standards, and product certification requirements. Different countries and municipalities follow separate plumbing regulations, making product standardization difficult for global suppliers. Frequent regulatory updates increase testing, redesign, and approval costs for manufacturers. Smaller companies often struggle to adapt quickly due to limited technical and compliance resources.

The plumbing component market is also challenged by the shortage of trained professionals capable of handling modern installation systems. Advanced piping networks, sensor-based fixtures, and smart water technologies require specialized technical knowledge during installation and maintenance and are experiencing an aging workforce while fewer younger workers are entering skilled plumbing trades. Improper installation can reduce system efficiency and increase long-term maintenance issues.

Regional Analysis North America: Market Dominance Led by Strong Presence of Organized Retail Channels and Growth in Multi-unit Residential ComplexesThe North America plumbing component marketaccounted for the largest regional share of 39.26% in 2025 due to the high replacement rate of aging residential water distribution systems across major cities and suburban areas. Many existing residential pipelines and fittings are reaching the end of their operational life, which is increasing systematic renovation and upgrade activities. Homeowners and property developers are actively replacing outdated plumbing networks with modern, durable, and efficient systems. Commercial infrastructure also contributes to steady demand through continuous refurbishment cycles.

US Plumbing Component Market

The plumbing component market in the USis driven by the strong presence of organized retail channels for plumbing components and a well-established distribution ecosystem where home improvement stores, specialized plumbing outlets, and digital platforms support easy product availability. Large retail chains such as Home Depot and Lowe's expand access to advanced plumbing products across urban and suburban regions, enabling faster consumer adoption. The residential renovation activities are frequently supported through these organized retail networks, improving product visibility and purchase convenience.

Canada Plumbing Component Market

The plumbing component market expansion in Canada is led by growing multi-unit residential complexes in urban centers. Rapid urban densification in cities is increasing demand for high-rise apartments and rental housing projects. According to the Canada Mortgage and Housing Corporation (CMHC), Canada recorded 259,028 housing starts in 2025, marking a 5.6% increase over 2024, with significant contribution from multi-unit construction activity. These developments require large-scale installation of pipes, fittings, valves, and integrated plumbing networks at the construction stage.

Asia Pacific: Fastest Growth Driven by Investments in Water Infrastructure Modernization and Growth in Affordable Housing & Smart City InitiativesThe Asia Pacific plumbing component market is expected to grow at a CAGR of 7.8% during the forecast period, showcasing the fastest regional growth. The growing adoption of modern plumbing systems in newly built residential clusters. Developers are integrating advanced plumbing networks in new residential projects to improve water efficiency and long-term durability. Smart housing layouts and organized township developments are increasing the demand for standardized plumbing components.

China Plumbing Component Market

The plumbing component market in China is driven by strong government investment in water infrastructure modernization, upgrading its municipal water supply systems to improve distribution efficiency and reduce leakage losses. Large-scale urban redevelopment projects are replacing outdated pipeline networks with advanced and durable materials. Government initiatives focusing on smart city development are also integrating modern plumbing systems into residential and commercial infrastructure.

India Plumbing Component Market

The plumbing component market ecosystem in India is experiencing rapid growth in affordable housing and smart city initiatives. The market expansion is closely linked with large-scale urban transformation programs that focus on improving residential infrastructure and public utilities. For instance, nearly 8,000 Smart Cities Mission's projects have been completed as of 2025, reflecting strong execution of urban development works across selected cities. This significantly improved water supply systems, sanitation networks, and housing infrastructure in multiple urban regions.

Plumbing Component Market Segmentation Analysis By ProductBy product, pipes dominated the market with a share of 40.48% in 2025 due to continuous replacement demand in aging water supply and drainage infrastructure. Many existing municipal pipelines are outdated and require systematic upgrades to prevent leakage and water loss. This replacement activity increases consistent procurement of pipes across urban and rural infrastructure projects.

The valves segment is expected to grow at a CAGR of 6.8% during the forecast period, driven by strong replacement demand due to upgrades in traditional manual valve systems. Older infrastructure is being replaced with modern control valves that offer better precision and operational efficiency. This transition supports automation in water flow regulation across residential, commercial, and industrial applications.

By Material TypeBy material type, plastic accounted for a share of 32.16% in 2025 due to high suitability for both cold and hot water distribution systems and commercial plumbing networks. This versatility allows consistent performance under varying temperature conditions, making it widely preferred in modern construction projects.

The composite materials segment is expected to grow at a CAGR of 7.2% during the forecast period, driven by better thermal stability compared to conventional single-material pipes. This stability ensures reliable performance under fluctuating temperature conditions in advanced plumbing systems. It reduces deformation risks and improves system durability, leading to increasing adoption in modern infrastructure and high-performance water distribution applications.

By ApplicationFaucets account for the largest application segment share of 36.49% in 2025 due to increasing preference for designer and aesthetic fixture installations. Consumers are focusing more on visual appeal and modern interior styling in kitchens and bathrooms. This shift is encouraging demand for premium, customized, and stylish faucet designs across residential and commercial projects.

The HVAC & water heating systems segment is expected to grow at a CAGR of 9.5% during the forecast period, driven by increasing integration with smart temperature control systems in residential spaces. These systems allow precise regulation of water heating based on user preferences and energy efficiency needs.

By Distribution ChannelIn 2025, wholesale distributors accounted for the largest share of 62.29% in the distribution channel segment. This is due to strong bulk procurement demand from construction contractors and large infrastructure projects. This channel supports uninterrupted material flow for ongoing construction activities, ensuring timely availability of pipes, fittings, and fixtures in residential and commercial development projects.

The online sales channels segment is expected to grow at a CAGR of 13.6% during the forecast period, fueled by increasing use of e-commerce platforms for renovation and repair purchases. Customers are shifting toward digital platforms for quick product selection and doorstep delivery to improve accessibility for small contractors and homeowners.

By End UserBy end user, the residential segment accounted for the largest share of 54.30% in 2025, advancing through continuous demand from renovation and bathroom/kitchen modernization activities. Household upgrades regularly require replacement of faucets, pipes, and fittings to improve functionality and design appeal. This ongoing improvement cycle in homes sustains steady consumption across both new housing developments and existing residential refurbishments.

The infrastructure & public utilities segment is projected to grow at a CAGR of 9.9% during the forecast period, fueled by increasing focus on sustainable water resource management systems. Governments and municipal bodies are investing in efficient water distribution, recycling, and drainage systems to reduce waste. These initiatives support large-scale installation of advanced plumbing components across public utilities.

Competitive LandscapeThe plumbing component market landscape is moderately fragmented, with multinational manufacturers, regional suppliers, niche brands, and local producers competing across varied price and application segments. Established players compete through strong distribution networks, certified product quality, advanced material technologies, and long-term contracts with construction and infrastructure developers. Emerging manufacturers compete through cost-effective offerings, customization flexibility, faster delivery, and strong presence in local construction demand. Smaller players are further expanding through online channels and renovation-driven residential sales.

List of Key and Emerging Players in Plumbing Component Market-

Aalberts N.V. (Netherland)

Central States Industrial (US)

Finolex Industries Ltd. (India)

McWane Inc. (US)

Morris Group Acorn (US)

Mueller Industries (US)

Nupi Industrie Italiane S.p.A. (Italy)

Reliance Worldwide Corporation Ltd. (US)

Turnkey Industrial Pipe & Supply Inc. (US)

Uponor Oyj (Finland)

ITT Inc. (US)

SPX FLOW (US)

Installed Building Products (US)

CKV Finished Products LLC (US)

Vortex Companies (US)

PrimeLine Products (US)

Thermador Groupe (France)

Quilinox (Spain)

Southside Plumbing (US)

Supreme Industries (India)

Orbia Wavin (Mexico)

December 2025: ITT Inc. announced an agreement to acquire SPX FLOW for approximately USD 4.8 billion, strengthening its portfolio in pumps, valves, and engineered flow components.

December 2025: Installed Building Products acquired CKV Finished Products LLC, a company involved in the installation of plumbing-related interior products, including bath accessories and fixtures.

October 2025: Vortex Companies acquired PrimeLine Products to expand its portfolio of trenchless pipe rehabilitation equipment, materials, and contractor-focused plumbing solutions.

September 2025: Thermador Groupe completed the acquisition of Quilinox, a company specializing in stainless steel components used in plumbing, heating, and fluid systems.

August 2025: GHK Capital Partners completed the acquisition of Rogers Building Solutions, strengthening its presence in specialty mechanical HVAC and plumbing infrastructure services for commercial and industrial end markets.

August 2025: Kingsway Financial Services acquired Southside Plumbing for up to USD 6.75 million as part of the expansion of its Kingsway Skilled Trades platform focused on commercial and residential plumbing services.

August 2025: Supreme Industries completed the acquisition of Orbia Wavin's India pipes and fittings business for USD 30 million and simultaneously entered a long-term technology partnership agreement to strengthen water management and plumbing infrastructure solutions across India and SAARC markets.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 127.65 Billion |

| Market Size in 2026 | USD 134.8 Billion |

| Market Size in 2034 | USD 208.45 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product, By Material Type, By Application, By Distribution Channel, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Plumbing Component Market Segments By Product-

Pipes

Valves

Fittings

Faucets

Connectors & Manifolds

-

Plastic

Metal (Copper, Brass, Stainless Steel)

Composite Materials

Others

-

Faucets

Water Supply Systems

Drainage & Wastewater Systems

HVAC & Water Heating Systems

Irrigation Systems

-

Wholesale Distributors

Retail Stores

Online Sales Channels

Specialty Plumbing Outlets

-

Residential

Commercial

Industrial

Infrastructure & Public Utilities

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment