403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Spine X-Ray And Computed Tomography Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

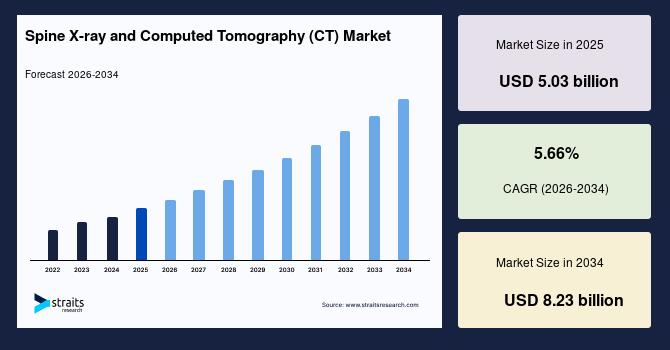

| 2025 Market Valuation | USD 5.03 billion |

| Estimated 2026 Value | USD 5.30 billion |

| Projected 2034 Value | USD 8.23 billion |

| CAGR (2026-2034) | 5.66% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | GE HealthCare, Siemens Healthineers, Koninklijke Philips N.V., Canon Medical Systems Corporation, Fujifilm Holdings Corporation |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Spine X-ray and Computed Tomography (CT) Market AI-powered Opportunistic Spine Screening in Routine CT ScansIntegration of AI for opportunistic screening during routine scans is a key trend for market growth. Companies like GE Healthcare and Siemens Healthineers develop AI tools that automatically review CT images taken for unrelated conditions to identify vertebral fractures and osteoporosis risks. Research presented by the Radiological Society of North America shows AI solutions like QCT Pro improve early detection accuracy. This approach adds diagnostic value without extra scans, supports preventive care, and improves overall imaging efficiency in hospitals.

Ultra-low Dose CT Protocols for Repeat Diagnostic CasesThe market is shifting towards advanced ultra-low-dose CT scanning in sensitive and repeat diagnostic cases. Earlier imaging methods exposed patients to higher radiation levels, but new protocols now prioritize safety while maintaining diagnostic accuracy. Modern CT systems use improved detectors and dose modulation software to reduce radiation significantly during spine evaluations. This transition supports safer long-term monitoring of spinal disorders and increases physician confidence in repeat imaging. It also aligns with stronger global regulations focusing on minimizing cumulative radiation exposure in diagnostic radiology practices across hospitals and imaging centers.

Market Drivers Rising Prevalence of Degenerative Spinal Disorders and Expansion of Hospital-Based Diagnostic Infrastructure Drives Spine X-ray and Computed Tomography (CT) MarketThe spine X-ray and CT market grows due to increasing cases of degenerative spine diseases, fractures, and spinal injuries. Aging populations and sedentary lifestyles increase conditions such as disc degeneration and spinal stenosis, which require frequent imaging for diagnosis and monitoring. For example, low back pain affects about 619 million people globally, making it a leading cause of disability and increasing demand for spinal imaging. Hospitals use CT and X-ray scans to assess injury severity in trauma cases from road accidents and falls. This rising clinical burden increases imaging volume across emergency and orthopedic departments and supports steady demand for advanced spinal diagnostic systems globally.

The market is driven by rapid expansion of hospital imaging infrastructure and emergency care facilities. Hospitals invest in advanced CT scanners and digital X-ray systems to enable faster and more accurate diagnosis of spinal injuries in trauma and critical care cases. Growth of multispecialty hospitals improves access to radiology services in urban and semi-urban regions. Integration of imaging equipment with hospital information systems enhances workflow efficiency and reporting speed. This infrastructure development increases scan volumes and strengthens demand for spine imaging systems across healthcare settings worldwide.

Market Restraints High Radiation Exposure and High Capital Cost Restrain Spine X-ray and Computed Tomography (CT) Market GrowthThe spine X-ray and CT market faces restraint due to concerns about repeated radiation exposure from multiple scans. CT scans expose patients to higher radiation levels than standard X-rays, which raises safety concerns for children and patients needing long-term spine monitoring. Guidelines from radiology organizations such as the American College of Radiology encourage doctors to avoid unnecessary imaging. Because of this, physicians often choose MRI instead of CT in some cases. This reduces the number of CT scans performed and limits the overall growth of spine imaging demand in healthcare systems.

The high capital cost of advanced imaging systems restrains market growth. A multi-slice CT scanner costs between USD 400,000 and USD 2 million, depending on features and slice capacity. Installation, shielding, maintenance, and software upgrades further increase total investment. Small hospitals and diagnostic centers delay purchasing these systems due to budget limitations. In developing regions, high upfront costs reduce adoption rates and limit access to advanced spine imaging. This financial barrier slows market penetration and restricts the expansion of CT-based diagnostic services in healthcare facilities.

Market Opportunities Rise of Dual-Energy CT for Advanced Spine Tissue and Expansion of Value-based Healthcare Offer Growth Opportunities for Spine X-ray and Computed Tomography (CT) MarketThe spine X-ray and computed tomography market grows with the adoption of dual-energy CT systems for advanced spine evaluation. This technology clearly separates bone, soft tissue, and inflammation compared to standard CT scans. Hospitals use it to detect spinal infections, fractures, and tumors spread more accurately. Dual-energy CT reduces the need for multiple imaging tests, which improves diagnostic efficiency and saves time. Its use increases in oncology and trauma centers, where doctors need detailed imaging for treatment planning. This approach improves clinical outcomes in complex spinal cases where conventional imaging has limited accuracy.

The market is benefiting from the global shift toward value-based healthcare systems. Hospitals and healthcare providers are focused on improving patient outcomes while reducing overall treatment costs. This increases demand for accurate and early diagnosis of spinal conditions using CT and digital X-ray imaging. Insurance companies and public health systems also support early detection because it helps prevent costly surgeries and long-term complications. As a result, healthcare facilities are adopting advanced imaging technologies and efficient diagnostic workflows. Imaging centers are investing in upgraded spine imaging systems that deliver faster, more precise results, creating new opportunities for market expansion.

Regional Insights North America: Market Leadership Driven by Advanced Cold Chain Logistics and Robust Public Funded Healthcare SystemThe North America spine X-ray and computed tomography (CT) market accounted for a revenue share of 38.16% in 2025 due to advanced trauma care systems and high imaging utilization in emergency departments. The region has a high rate of road accidents and sports injuries, especially in the US, which increases demand for rapid spinal CT diagnostics. For example, large health systems such as HCA Healthcare and Kaiser Permanente operate extensive hospital and diagnostic networks, enabling centralized imaging services and fast referral pathways. Early adoption of AI-enabled CT systems and favorable reimbursement policies for diagnostic imaging further support market growth in North America.

The US spine X-ray and computed tomography (CT) market growth is driven by high-throughput outpatient radiology networks, where imaging intensity is significantly higher than global averages. Recent US radiology utilization analysis shows that a single radiologist in high-volume centers can interpret nearly 50-60 imaging studies per day, with CT contributing the largest share of workload due to its role in trauma and emergency spine assessment. The US has one of the highest sports injury rates globally, with the CDC reporting millions of emergency visits annually related to sports and recreation injuries, many requiring spinal imaging. This structured trauma-care ecosystem ensures continuous, high-volume utilization of CT and X-ray systems across emergency workflows.

Canada's spine X-ray and CT market benefits from a strong publicly funded healthcare system that ensures wide access to diagnostic imaging services across provinces. High prevalence of spine disorders linked to an aging population, especially in provinces like Ontario and British Columbia, increases demand for CT and X-ray scans. Canada's cold climate contributes to higher fall-related injuries and spinal trauma cases during winter months, driving emergency imaging utilization. Integration of advanced imaging systems in hospital networks and government investments in reducing diagnostic wait times further support steady market growth across the country.

Asia Pacific: Fastest Growth Driven by Government-led Mass Immunization Campaigns and Booming Geriatric PopulationThe Asia Pacific spine X-ray and computed tomography (CT) market is expected to register the fastest growth with a CAGR of 7.53% during the forecast period due to the rising burden of road traffic accidents in densely populated countries such as India, China, and Indonesia, which significantly increases demand for emergency spinal imaging in trauma care centers. Another factor is the large-scale expansion of government healthcare infrastructure, including new tertiary hospitals and diagnostic imaging centers under national health schemes in countries like India's Ayushman Bharat program. Increasing medical tourism in countries such as Thailand, Singapore, and Malaysia boosts the adoption of advanced CT imaging systems in private hospitals.

The China spine X-ray and computed tomography (CT) market grows due to rapid expansion of tier-3 and tier-4 hospitals under China's“Healthy China 2030” initiative, which is significantly increasing access to advanced CT imaging in semi-urban and rural regions. Strong integration of AI-enabled radiology platforms by domestic companies such as United Imaging Healthcare and Mindray, which improves spine fracture detection efficiency in high-volume hospitals. China's extremely high aging population base, with over 280 million people aged 60+, according to national statistics, is driving a surge in degenerative spine disorder diagnoses requiring frequent CT and X-ray imaging.

The Japan spine X-ray and computed tomography (CT) market benefits from a high proportion of elderly population, with over 29% of citizens aged 65 and above, leading to a high incidence of osteoporosis-related vertebral compression fractures that require frequent CT and X-ray imaging. Widespread integration of robot-assisted orthopedic and spine surgery planning systems in major hospitals in Tokyo and Osaka increases pre- and post-operative spinal imaging demand, strengthening consistent utilization of CT and X-ray diagnostics across healthcare facilities. These factors collectively drive the market growth in Japan.

By ProductThe X-ray devices segment is expected to grow at a CAGR of 5.94% during the forecast period, due to the increasing demand for portable and digital radiography systems, which allow quick bedside imaging in emergency and trauma cases without moving patients. Rising adoption of digital X-ray systems is replacing analog units, improving image quality, storage, and workflow efficiency. Expansion of outpatient orthopedic clinics increases routine spine screening demand, as X-ray remains the first-line imaging tool before advanced CT or MRI, supporting consistent segment growth.

The computed tomography devices segment is expected to grow at a CAGR of 6.19% during the forecast period due to high-resolution spinal imaging in trauma and emergency care cases. Rising incidence of road accidents and sports injuries drives rapid adoption of CT systems in hospital emergency departments for fast and accurate diagnosis of spinal fractures. Growing integration of AI-based image reconstruction and expanding hospital infrastructure in emerging economies further accelerate CT system installation.

By IndicationSpinal injuries dominated the indication segment with a share of 29.31% in 2025, the routine use of emergency spinal CT protocols for rapid fracture detection, orthopedic and neurosurgery planning for spinal fixation and recovery monitoring, and medico-legal documentation in trauma cases. These clinical applications make spine imaging essential in emergency departments, increasing consistent scan utilization across hospitals.

The spinal tumors segment is expected to have the fastest growth, registering a CAGR of 6.37% during the forecast period, due to the increasing use of contrast-enhanced CT and high-resolution spinal imaging protocols that improve detection of metastatic lesions in vertebrae at earlier stages. Growing adoption of multidisciplinary oncology workflows combining radiology and surgical planning systems increases repeated imaging demand for treatment evaluation and post-therapy assessment.

By End UserThe hospitals segment dominated the market, accounting for 39.65% revenue share in 2025 due to centralized emergency, radiology, and surgical services enabling immediate spine imaging. High patient inflow in inpatient and outpatient departments increases scan volume. Integrated multidisciplinary teams use CT and X-ray for real-time diagnosis and treatment planning in trauma, orthopedic, and neurosurgical cases.

The diagnostic imaging centers segment is projected to grow at a CAGR of 6.70% during the forecast period, driven by increasing preference for outpatient and cost-efficient spine imaging services. Patients are shifting from hospitals to standalone centers for faster appointments, shorter waiting times, and lower diagnostic costs. Rising demand for routine spinal screening and follow-up scans further supports utilization. Expansion of chain-based radiology networks and adoption of advanced digital X-ray and CT systems improve service quality and accessibility, driving strong growth of diagnostic imaging centers.

Competitive LandscapeThe spine X-ray and computed tomography (CT) market is moderately consolidated, with strong competition among global medical imaging companies such as Siemens Healthineers, GE HealthCare, Philips Healthcare, and Canon Medical Systems. These players dominate through advanced CT scanners, digital X-ray systems, and continuous innovation in low-dose imaging and AI-based diagnostic tools. They focus on expanding product portfolios and strengthening hospital partnerships worldwide. Emerging players and regional manufacturers compete by offering cost-effective imaging systems and service-based solutions. Growing demand for AI integration and portable imaging systems further intensifies competition across developed and developing healthcare markets.

List of Key and Emerging Players in Spine X-ray and Computed Tomography (CT) Market GE HealthCare Siemens Healthineers Koninklijke Philips N.V. Canon Medical Systems Corporation Fujifilm Holdings Corporation Carestream Health Inc. Agfa-Gevaert Group Shimadzu Corporation Hitachi Medical Systems Mindray Medical International Limited Neusoft Medical Systems Planmed Oy Ziehm Imaging GmbH Recent Developments-

In December 2025, Canon Medical Systems received FDA 510(k) clearance for its Alphenix 4D CT with Aquilion ONE/INSIGHT Edition, a hybrid CT–angiography system designed for integrated interventional and diagnostic imaging workflows.

In November 2025, Canon Medical Systems launched the Mobirex i9/Smart Edition mobile X-ray system, targeting hospital radiography workflows, including spine and trauma imaging, to enhance bedside imaging and orthopedic diagnostics.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.03 billion |

| Market Size in 2026 | USD 5.30 billion |

| Market Size in 2034 | USD 8.23 billion |

| CAGR | 5.66% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product Type, By Indication, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Spine X-ray and Computed Tomography (CT) Market Segments By Product Type-

X-ray Devices

-

Digital X-ray Systems

Analog X-ray Systems

-

Single-slice CT

Multi-slice CT

-

Spinal Injuries

Spinal Fractures

Spinal Tumors

Other Indication

-

Hospitals

Diagnostic Imaging Centers

Other End User

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment