403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

THINK Ahead: Tariffs Are Back And They're Giving Main Character Energy

(MENAFN- ING)

Tariffs are back – and they're giving Main Character Energy

Source: USATrade, White House, ING analysis

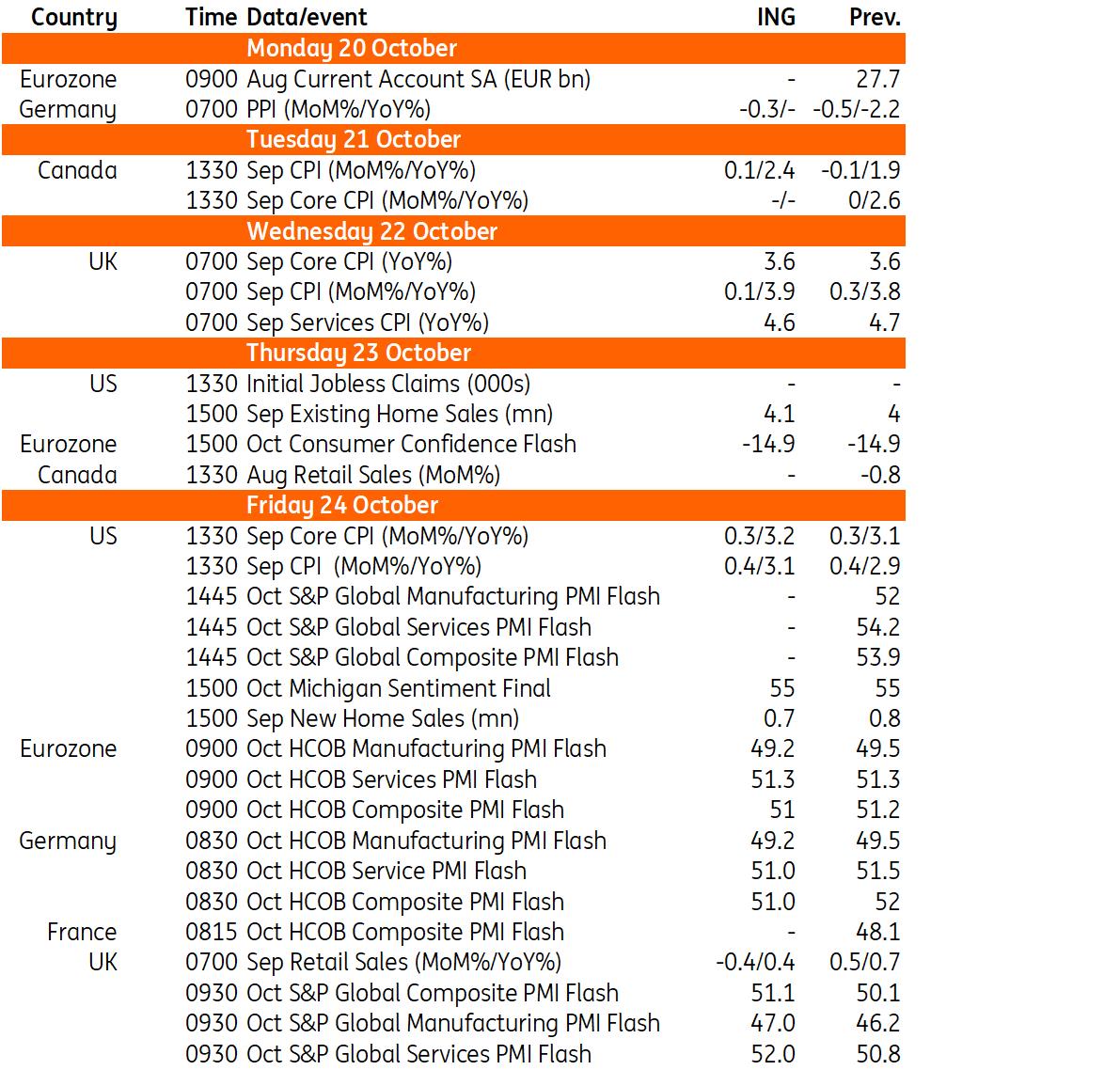

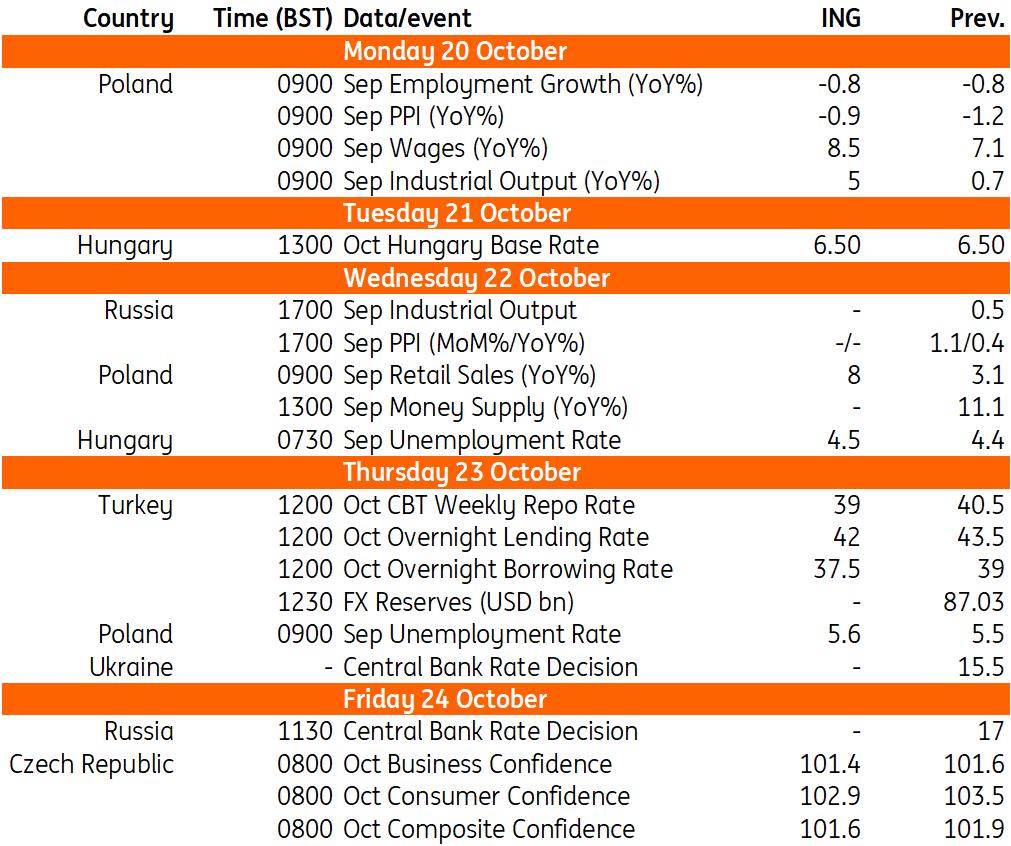

Source: Refinitiv, ING Key events in EMEA next week

Source: Refinitiv, ING

The vibes are off. Everyone's low‐key panicking and it's giving recession energy. That's how Gen Z traders would describe markets today – if I knew any. I don't, so I asked our AI overlords to translate the mood instead. They replied:“grim, bestie” (?????)

Anyway, you get the picture. As we stumble into the weekend, the straws in the wind are blowing ominously. Regional bank nerves are back. US funding markets are strained. The notoriously opaque private credit markets are giving investors the ick (am I doing this right?)

Volatility is rising. Equities are down. Oil prices are falling. Gold still looks unstoppable. And markets have begun dabbling with bigger Fed rate cuts.

That's before we talk about tariffs. Will President Trump follow through on his threat to impose more 100% tariffs on China, ahead of his one-to-one with President Xi at the end of the month?

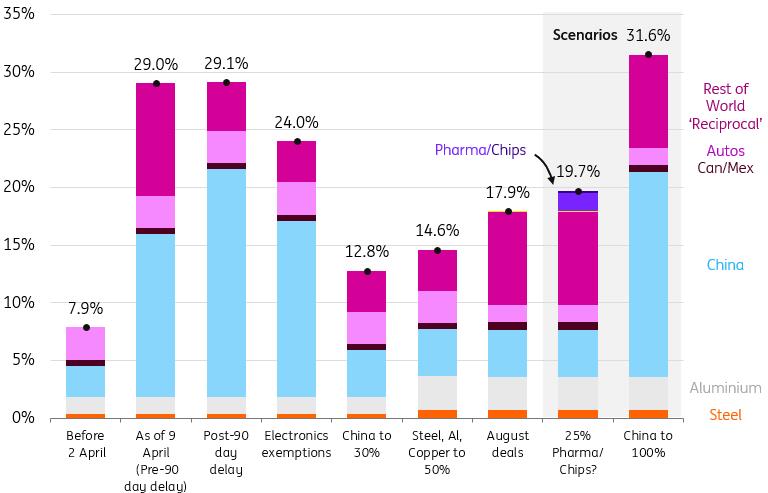

Most investors would say no, I imagine. Certainly, if he did, it would take the US average tariff rate up to 31%, if my maths is right, surpassing the levels seen around 'Liberation Day'. Back then, it was quickly evident that those sorts of levels were unsustainable.

The average US tariff rate would surpass 'Liberation Day' levels under 100% China leviesSource: USATrade, White House, ING analysis

Yet the market reaction to his threat last week was interesting, no cap (another Gen-Z-ism, apparently).

Interesting that there was a reaction, given that many of Trump's recent tariff threats have fallen on deaf ears. It hints that some are watching the tail-risk of a miscalculation in US-China tensions. Lynn Song argues that China has proven incredibly resilient to US tariffs, helped by offsetting demand from elsewhere in the world, and backed by its higher-value export industries, which are less dependent on American demand.

Whatever the reasoning, US equities and short-dated yields both fell on the news, and the dollar weakened. It's telling that investors think further tariffs would require more Fed easing, not less. Six months on from 'Liberation Day', the evidence so far shows the jobs market creaking and inflation remarkably benign.

That thinking will be tested next Friday, because good news, folks, we finally have some official US data! Savour it, because Washington is showing little sign of bringing the shutdown and the resultant data drought to a close...

Chatting to James Knightley, our US economist, he reckons there is more tariff-induced price pressure to come. Tariff revenues over the summer amounted to 10% of imports, a significant undershoot on the 18% we'd expect based on what's been announced and 2024 import data.

Whatever the reason for that, we expect revenue collection to improve over the coming months. Either corporates will have to keep absorbing that extra hit in their margins, or more likely, we'll start to see more evidence of firms passing on the costs.

Knightley particularly highlights car prices – a significant area of US tariffs, yet new vehicle prices have remained essentially flat. Price increases feel like a matter of time, and a fire at a key aluminium supplier to the auto industry won't help matters.

That said, the fact that the tariff hit has been more spread out means we're looking at a lower, but more drawn-out peak for US inflation. And that means the disinflationary forces at work – chiefly slowing rental inflation – will have a more noticeable effect. That's ultimately why we're still expecting a further four Fed rate cuts, more than the committee itself indicated at the time of its September meeting.

But what happens if the President's tariffs are ruled illegal? We won't have to wait much longer to find out; the Supreme Court will start hearing arguments in early November against the use of emergency powers to impose sweeping country-level tariffs. There are plenty of legal voices out there who have“deeped it” – my younger colleague informs me this means“thought carefully” – and reckon it won't go Trump's way.

If that happens and the majority of tariffs imposed this year are struck down, then the president does have means of replacing them. Section 122 lets the Administration apply 15% tariffs for up to 150 days. Other sectoral tariffs are possible too. Yet the net result would still probably be a lower effective tariff rate across US imports.

That would take the pressure off inflation and, in theory, the jobs market too. If markets are right that the latter matters more to the Fed right now, then it's tempting to conclude that all of this would mean fewer rate cuts.

Yet it's complicated AF. A ruling against tariffs imposed under emergency powers would presumably spark chaos, given that firms would likely be due a refund on the bulk of the tariffs paid so far. And uncertainty about what tariffs would come in their place would likely keep a lid on sentiment. That's before we talk about the impact of lower tariff revenues on America's perilous 6%+ fiscal deficit.

Whatever happens, tariffs have re‐entered the chat, and they're giving main character energy this autumn. As for me, I'm off to sip a matcha latte and rehearse a TikTok dance apology, just in case Gen Z drag me and this article to the Supreme Court as well...

James Smith

THINK Ahead in developed marketsUnited States (James Knightley)

-

September CPI (Fri): With no imminent end in sight to the government shutdown, we will again be lacking clarity on how the economy is performing, given that statistical agencies remain shuttered. Even if we do see a re-opening, it will likely take a couple of weeks to get back on track with all the sampling that is required. That said, it has been confirmed that resources have been put in place to publish the September consumer price inflation report. This is not because the Fed desperately needs to see it ahead of the 29 October FOMC meeting, but rather because the number is needed to determine the Social Security Administration's 2026 cost-of-living adjustment. We don't disagree with the consensus that headline prices will rise around 0.4%MoM and 0.3% for the core measure. Tariffs may start to become a little more obvious, but given the Fed's primary worry right now is a cooling in the jobs market, this won't block a 25bp rate cut later this month. The Fed's Beige Book remains somewhat downcast on the economy's prospects, while private sector jobs data has been weak.

United Kingdom (James Smith)

-

Inflation (Wed): Headline CPI is set to nudge higher, though mainly because the sharp fall in petrol prices this time last year wasn't matched to the same degree this September. This release should mark the peak in headline inflation, even if it's unlikely to fall materially before year-end. In better news, we expect services inflation to move lower, undershooting the Bank of England's August forecasts. In theory, that should move the dial towards further cuts, though for now officials are more focused on rising food inflation. We think that limits the chances of further BoE easing before February next year.

Poland (Adam Antoniak)

-

September industry (Mon): A more favourable calendar and a low reference base from September 2024 provide a solid foundation for a strong annual reading of industrial output. Unfortunately, the short-term outlook has once again become more uncertain, following the recent disappointing performance of German manufacturing and weak automotive export figures. Some local manufacturers from the automotive industry have announced temporary production pauses or plant shutdowns due to insufficient demand. This is likely to weigh on industrial output in the final quarter of the year. Moreover, renewed downward pressure on manufacturing prices suggests that, contrary to our earlier expectations, producer price index (PPI) deflation is unlikely to come to an end this year.

September labour market (Mon): An additional working day and a low base effect should result in a somewhat stronger wage reading. However, the overall downward trend is expected to persist, despite elevated volatility in the monthly data. Although some automotive plants plan production pauses, employers have confirmed that workers will continue to receive compensation during these periods. Employment in larger enterprises continues to decline slightly, driven by a shrinking labour supply – primarily due to retirements – and weakening demand for labour.

September retail (Wed): Brace for a strong set of September retail sales data. Recent months have shown a continued recovery in demand for durable goods. Combined with a higher number of trading days and an exceptionally low base from September 2024 – when the southern part of the country was affected by flooding – this creates a favourable backdrop for robust trade figures. Consumption once again emerged as the main driver of GDP growth in the third quarter of 2025.

Hungary (Peter Virovacz)

-

Base rate (Tue): The most important event in Hungary next week is the central bank's October rate-setting meeting. What's our advice for this time? Don't hold your breath waiting for a dovish shift. Headline and core inflation remain elevated, as do inflation expectations. Additionally, the forint has weakened since the previous meeting. This is partially due to the dollar, but also due to local factors, such as dovish remarks from the government regarding monetary policy. Therefore, we believe the Monetary Council will attempt to appear as hawkish as possible to restore the market's confidence in its hawkish stance.

Turkey (Muhammet Mercan)

-

Rate decision (Thur): Higher-than-expected inflation data for September shows the impact of pressure in food prices and challenges in services inflation, while indicators for October imply further upside risks to the outlook. The Central Bank has a hawkish forward guidance, pledging to tighten policy if the inflation outlook deviates from interim targets. Therefore, the question is whether the bank would stop or adjust the pace of cuts with the recent deterioration in the underlying trend. Given the high level of the policy rate and likely decline in inflation ahead, we expect gradual rate cuts to continue with a 150bp cut to 39% in the October MPC, though risks are tilted to the upside with a lower or no cut.

Czech Republic (David Havrlant)

-

Sentiment (Tue): Both business and consumer sentiment are expected to have remained above the long-term 100-point average in October; however, both will likely see some correction from previous relatively upbeat readings. The Czech industry seemed to have stabilised somewhat, yet the subdued demand from its main euro trading partners will temper business mood. The consumer is doing well, while the mediocre situation in manufacturing casts question marks about job security for low-skilled workers and weighs on sentiment.

Source: Refinitiv, ING Key events in EMEA next week

Source: Refinitiv, ING

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

- Xmoney Launches $XMN On Sui, Expands Listings Across Global Exchanges

- Ozzy Tyres Grows Their Monsta Terrain Gripper Tyres Performing In Australian Summers

- Cregis And Kucoin Host Institutional Web3 Forum Discussing Industry Trends And Opportunities

- Superiorstar Prosperity Group Russell Hawthorne Highlights New Machine Learning Risk Framework

- Dexari Unveils $1M Cash Prize Trading Competition

- Xdata Group Named Among The Top 66 Saas Innovators In Techround's 2025 List

More Story

Comments

No comment