403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Rates Spark: Yields Remain Vulnerable To A Reversion Higher Ahead

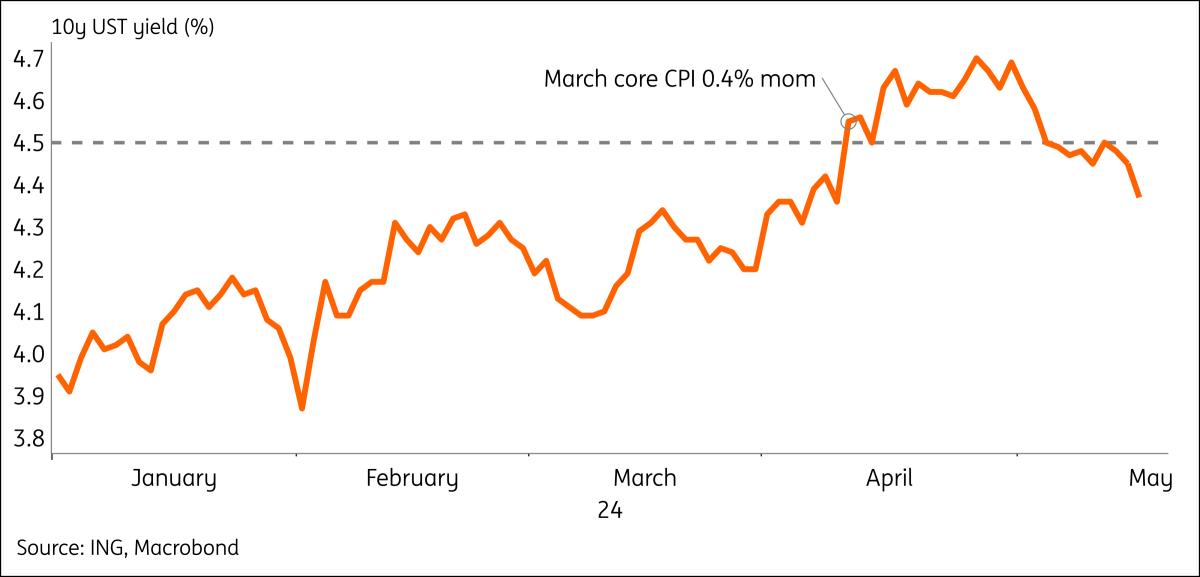

(MENAFN- ING) Better data helps 10y UST yield stay below 4.5%

Thursday's events and market view

Latest US CPI inflation data don't change this narrative, as it remains too hot for a Fed cut (despite the dramatic dip in rates and risk-on reaction). We agree that 0.3% month-on-month is a significant improvement, but this number is still hot on an annualised basis for the Fed. Next data point to watch would be the PCE deflator later this month, which should benefit from weaker PPI subcomponents and a lower CPI. Markets are close to pricing in two cuts for 2024, but those inflation numbers will still need to come down from where we stand.

With ECB rate cuts after June still up in the air, euro markets remain sensitive to US moves. Comments from ECB speakers are also not very helpful, with the bottom line being that the June cut is certain but nothing thereafter. The fact that little new information is shared reflects the data-dependent approach by central banks currently, means markets will also have to show patience and monitor data closely. In the eurozone the next key data points would be PMIs next week. So far the eurozone is following a gradual recovery, but weaker US growth would not bode well for the outlook.

Weaker data helps 10y UST yield move away from 4.5% handleThursday's events and market view

Thursday's data slate does not feature any top tier data, but given markets' sensitivity to inflation the US import prices might still elicit some reaction. But it might actually be the initial jobless claims that could see a larger reaction, as markets are also on the lookout for weakness in the hard data and more hints of job market cooling more specifically. The initial claims had ticked up last week and are now expected to drop back, while continuous claims had remained steadier.

In the eurozone, ECB speakers remain prominent on the calendar – with appearances by Panetta, de Guindos, de Cos and Centeno. Thursday's slate looks a little more dovish, although we have Nagel and Villeroy scheduled as well.

In primary markets we have France issuing up to €12bn in short- to medium-term bonds and another €2bn in inflation linked bonds. Spain issues up to €5.5bn in three bond lines including its 18Y green bond.

Author:Padhraic Garvey, CFA, Michiel Tukker, Benjamin Schroeder

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment