403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

The Purchasing Power Of Hungarian Wages Is Slowing

| 14% | Average wage growth (Feb) ING Forecast 14.4% / Previous 14.7% |

| Lower than expected |

According to the latest Hungarian Central Statistical Office (HCSO9 earnings statistics), the pace of year-on-year wage growth in Hungary slowed further in February. However, the still rather high growth rate of 14% year-on-year (based on the full range of employers) is still much more reflective of economic developments in 2023 than of what has happened this year. Given that many companies now follow a spring-to-spring wage cycle (i.e., wage increases take place between March and April rather than in January as in the past), the February figures still largely capture high wage increases to compensate for the extreme inflationary environment in 2023.

Meanwhile, the continued moderation in wage dynamics suggests that where wage adjustments have already taken place this year, they may have been significantly smaller than last year. This was partly foreshadowed by the 10% increase in the guaranteed minimum wage, which is a minimum wage scheme for skilled workers that affects around 750,000 workers out of a labour market of 4.7 million. According to Randstad's 2024 Wage Expectations Survey, while 91% of employees hope for a minimum wage increase of 11%, 63% of employers would implement a maximum wage increase of 11%. Against this backdrop, we expect that the overall pace of wage growth may slow down more markedly in the coming months, and that real wage growth may decelerate, so there is little reason to fear a possible price-wage spiral.

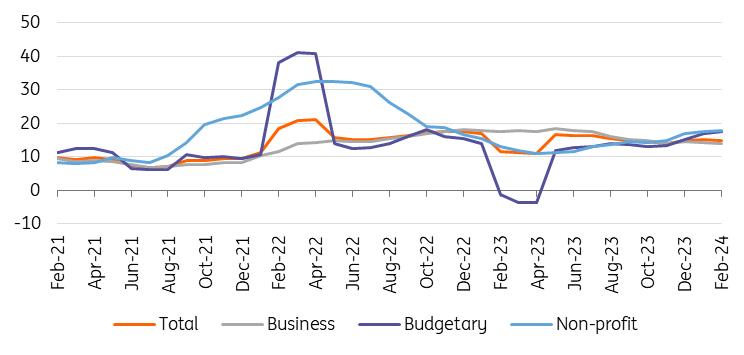

Hungary's wage dynamics3-month moving average, % YoY

Source: HCSO, ING

The detailed data also shows that the public sector recorded above-average wage growth dynamics in February (17.2% YoY), mainly reflecting the impact of stronger wage outflows in the education sector. In the business sector, the pace of wage growth slowed in many areas, with overall growth now standing at“just” 12.8% on a yearly basis. However, some sectors have shown particularly surprising wage dynamics. This is the case in construction, where the growth outlook remains somewhat gloomy, but the rate of wage growth has accelerated to an above-average level. In the services sector, although wage growth is below average in many areas, there was some acceleration between January and February.

Real wage growth in Hungary (% YoY)

Source: HCSO, ING

It is also worth noting that the gap between the average and median wage has continued to narrow, presumably reflecting the impact of the minimum wage increase and the trend towards below-average wage growth in higher-paid sectors. In other words, firms are trying to make some headway on wage costs.

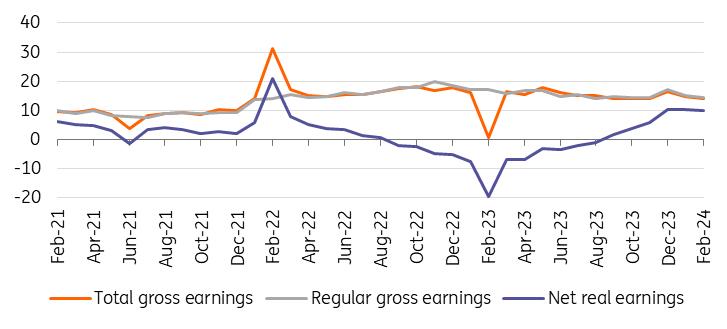

Nominal and real wage growth (% YoY)

Source: HCSO, ING

As inflation slowed further in February, but the pace of average wage growth slowed more, real wage growth fell below 10% on an annual basis. Looking ahead to the rest of the year, wage growth is likely to continue to erode purchasing power. On the one hand, wage outflows will slow down and, on the other hand, inflation may pick up. This was also pointed out by the National Bank of Hungary at its April rate-setting meeting. The central bank expects real wage growth of around 6% for 2024 as a whole, which is roughly in line with our own expectations. With average wage growth of around 10%, inflation is expected to be 4.5%.

The only remaining glaring question is when and how this growth in household purchasing power will translate into increased consumption. So far this year, retail sales have underperformed, with a flat month in January and a 0.6% month-on-month decline in February. It seems that, despite strong wage growth, consumer confidence needs to improve further and precautionary saving needs to ease, which will take more time than previously expected.

Author:Peter Virovacz, Dávid Szőnyi

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment