(MENAFN- ING) Recent growth pace has returned to pre-Covid norm

Indonesia's Economy grew by 5.05% in 2023 , with growth returning to the pre-Covid norm of roughly 5% of expansion. Household consumption remained a key support for overall economic activity, delivering a healthy 4.5% year-on-year gain, while government spending also managed to contribute to the rise in economic activity. Meanwhile, capital formation was a modest surprise as it managed to expand despite elevated borrowing costs. On the other hand, net exports delivered a less potent push with global demand for the country's exports waning.

We predict that growth will remain positive this year, slightly above average at 5.2% YoY. The recent intensification of global headwinds, however, could pare this estimate closer to the pre-Covid average of roughly 5% YoY should threats prove persistent.

Flare up in inflation to derail growth?

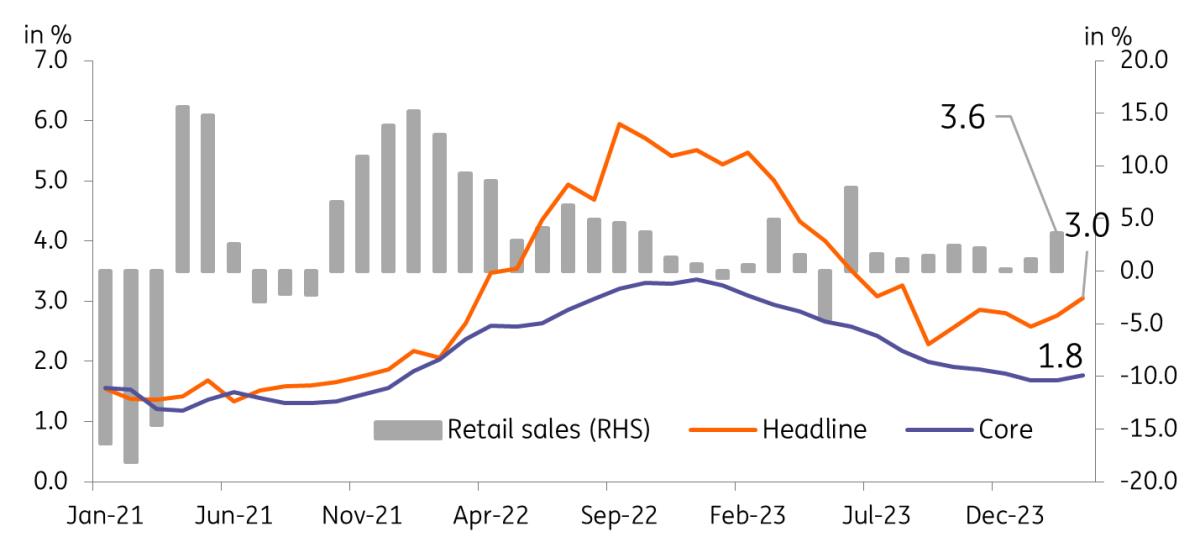

Household spending has been a major contributor to growth, and we could see a modest boost coming from election-related spending for the first quarter 2024. We've noted a brief improvement in Bank Indonesia's (BI) retail sales survey for February, which was up 3.6% YoY, coinciding with the national election and subdued core inflation.

The recent pickup in price pressures could, however, be a potential headwind for the economy, with both headline and core inflation inching up to start 2024. BI has flagged a potential flare up for inflation due to faster food and energy inflation. Unfortunately, the reacceleration in inflation is happening at a time when the central bank lowered its official inflation target band to 1.5-3.5% (from 2-4% in 2023).

Faster inflation threatens to cap retail sales outlook?

Source: Bank Indonesia and Badan Pusat Statistik Retail sales have been largely flat even ahead of inflation rebound

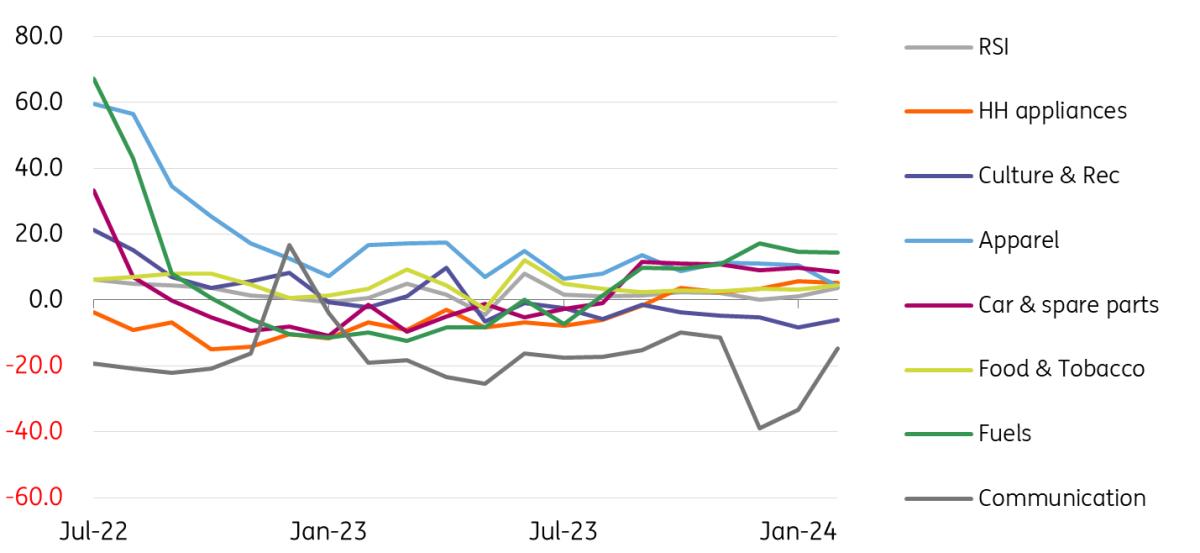

Retail sales have been in expansion, but have been largely flat even during a period of subdued inflation. One exception was spending on communications, which dipped in late 2023 before recovering sharply at the start of the year possibly due to the availability of lower-priced handsets and service plans.

In the coming months, the El Nino weather phenomenon will likely ensure food costs are elevated while the recent increase in crude oil prices could also fan price pressures. Should inflation continue to accelerate in the coming months, we may see retail sales and overall household spending weighed down by higher prices as consumers adjust to faster inflation.

Retail sales have been largely flat of late

Source: CEIC Export struggles have been pronounced

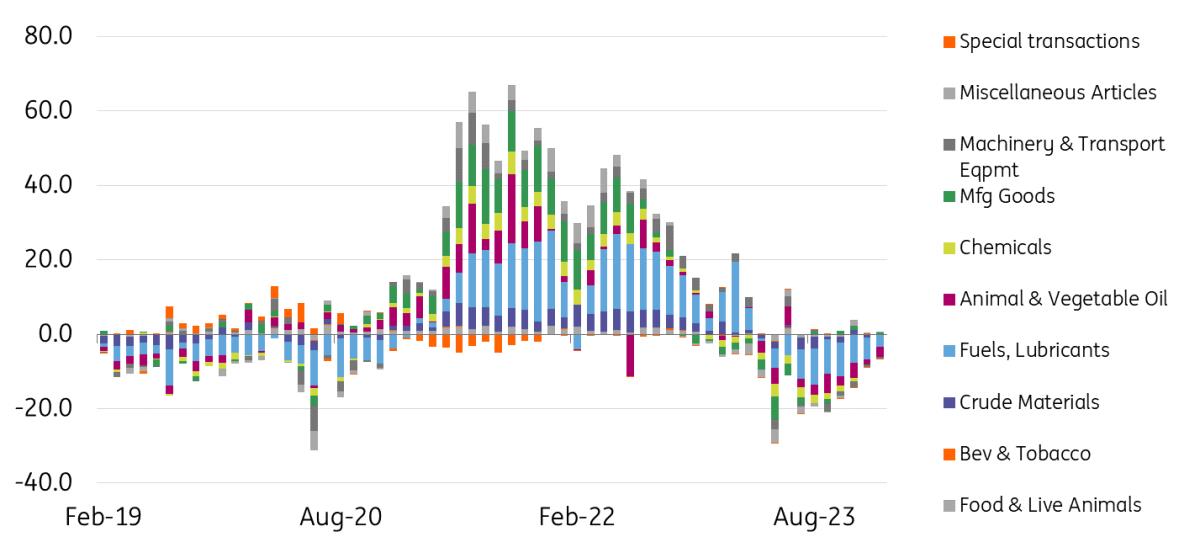

Once a source of stability and growth, Indonesia's export sector has struggled due to softer global demand and lower global prices for top export commodities. Furthermore, the strong performance of the economy's export sector powered a record wide trade surplus in 2022, which provided support for the IDR with the currency displaying resilience during those periods due to the strong dollar inflows.

More recently, exports have struggled. Almost all subsectors have contracted, with both the fuel and lubricants and animal and vegetable oils subsectors falling the most. The stark drop in the international price for both coal and palm oil, coupled with a decline in global demand, resulted in the almost eight-month decline.

Should demand for Indonesia's commodity exports improve while global prices remain elevated, we could see a decent recovery for the export sector in 2024. Meanwhile, the recent rise in global prices for both coal and palm oil could boost export receipts further if prices remain on an uptrend.

Exports have been in contraction since mid-2023

Source: CEIC Industrial production feels heat from softer export numbers

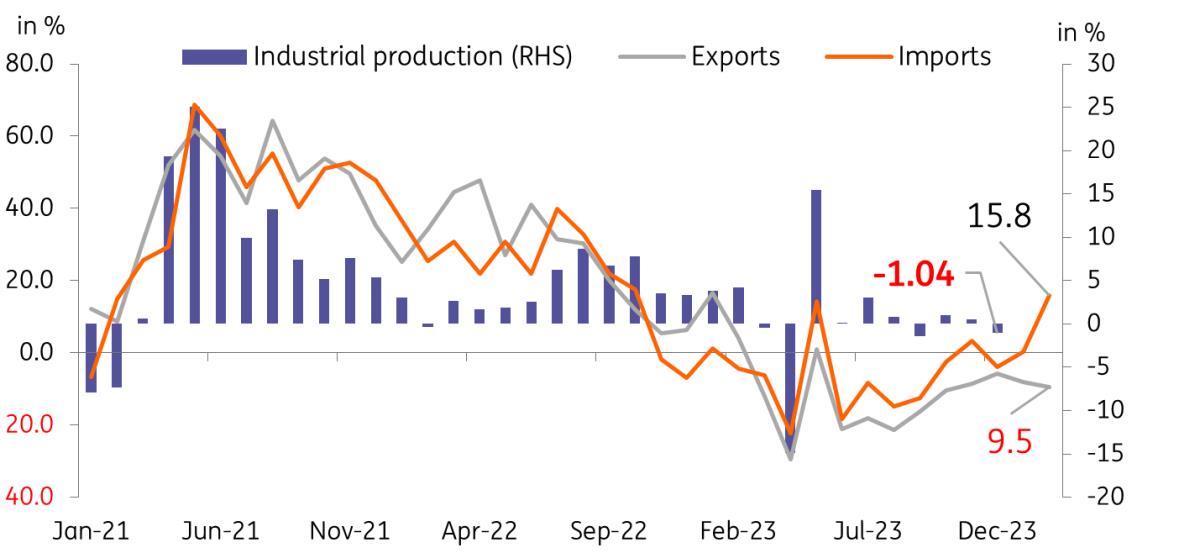

As mentioned previously, the fate of Indonesia's export sector has a direct link to other sectors in the economy, such as the industrial sector. Strong exports recorded between 2021 and 2022 translated to a similar rise in industrial production during the same period. Because of the struggles of the export sector last year, we've seen a similar decline in industrial production as manufacturing slowed considerably once demand for Indonesia's exports dried up.

For 2024, we can say that any potential recovery for industrial output will be tied to a similar improvement in prospects for the country's export sector.

Industrial production tracks export performance

Source: CEIC External outlook no longer as resilient

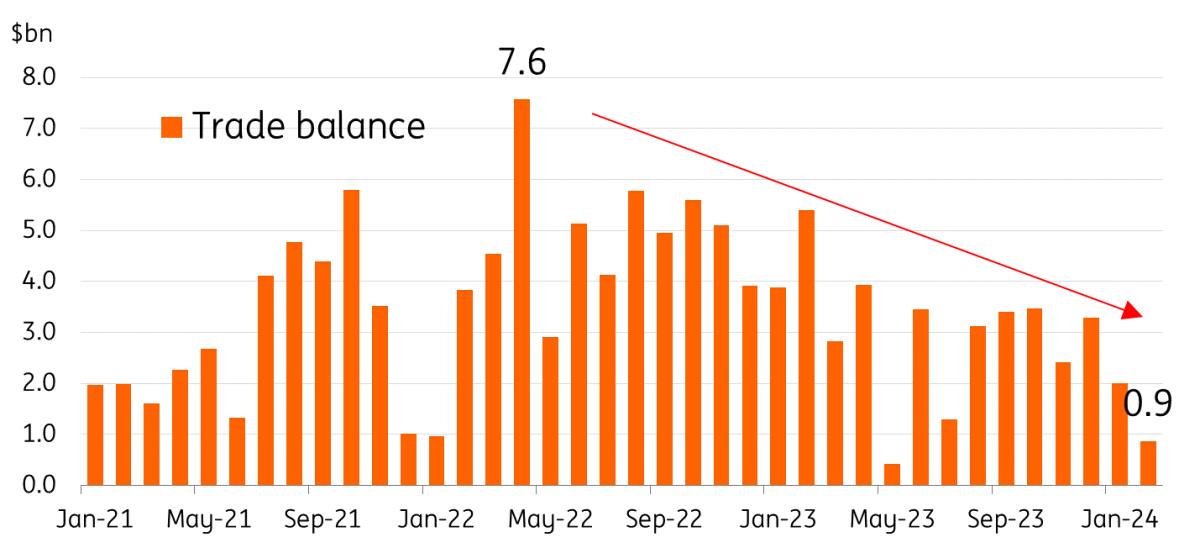

Indonesia's current account balance has managed to eke out months of surplus by virtue of a sustained run of trade surpluses. However, with the trade surplus now much more modest – averaging $3bn a month in 2023 and down to $867m as of February – the support it provided previously has diminished somewhat. Indonesia's current account surplus has waned from $15.3bn in the first quarter of 2023 down to a deficit of $1.6bn by the end of 2023, according to Bank Indonesia.

With the outlook for the export sector positive but not overly optimistic, we can expect the trade surpluses and the current account in deficit, which should mean limited support for the IDR – if any at all. We therefore expect the currency to come under pressure for most of the year, with the IDR likely to lag any potential rally by regional peers.

Support delivered by trade surplus just not what it used to be

Source: Badan Pusat Statistik Bank Indonesia rate cuts in 2H?

BI Governor Perry Warjiyo has remained balanced in his assessment of the current monetary policy stance. Inflation has, for the most part, remained contained. However, risks remain tilted to the upside and the lower target could force BI to remain prudent for now.

On top of the inflation threat, the loss of support coming from the current account surplus will also likely convince BI to maintain interest rate differentials to help ensure IDR stability and offset the sharp narrowing of the trade surplus.

We therefore believe that any BI easing may only take place in the second half of the year, with the central bank opting for a more shallow reduction of up to 50bp worth of rate cuts. The main determinant for the timing of BI cuts, however, remains tied to IDR stability. We only see the central bank easing when pressure on the IDR is minimal.

Fiscal consolidation ahead of schedule

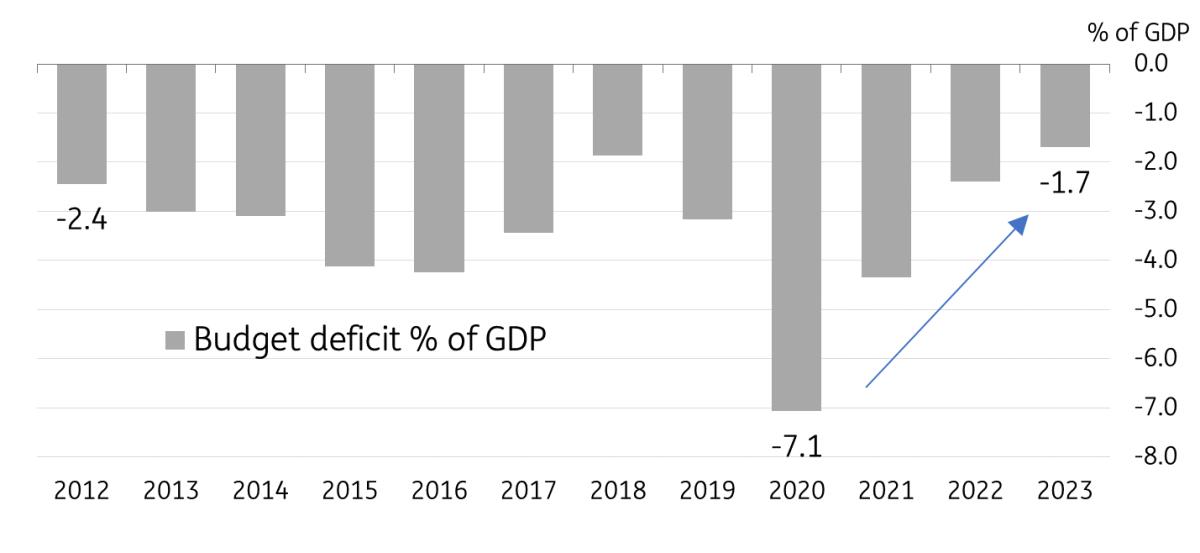

Indonesia's fiscal metrics continued to improve, with the deficit-to-GDP ratio falling sharply to 1.7% last December 2023, lower than the target of 2.3% for the year. Indonesia had previously planned to bring the deficit-GDP ratio back below 3% by 2024, but robust economic performance helped restore revenue streams. Meanwhile, pressure on fiscal support to the population has receded, resulting in the improved fiscal position.

Fiscal consolidation achieved sooner than target

Source: BI Enter Prabowo, eye on fiscal sustainability

Defence Minister Prabowo Subianto was recently proclaimed the official winner of the 2024 election, and he will have the task of proving that he was indeed a continuity candidate. One of Prabowo's campaign promises was to provide free lunch to students and teachers, fuelling concerns over the fiscal sustainability of such a programme.

Prabowo attempted to alleviate these concerns, vowing to maintain fiscal discipline during a televised speech after his election win was apparent. Economic Minister Airlangga Hartarto indicated the incoming president would strive to maintain pre-set targets for both public debt (60% of GDP) and the budget deficit ceiling (3% of GDP). This year, the deficit to GDP ratio will likely hit 2.8% of GDP, with next year's projection expected to settle between 2.5-2.8% of GDP.

An early test for incoming President Prabowo's governance would be his ability to fulfill his campaign promises (such as the free lunch programme) while still ensuring fiscal sustainability. Maintaining fiscal discipline will be key to safeguarding investor sentiment as improved fiscal metrics remain a key factor in supporting the positive outlook for the economy.

Overall 2024 outlook

The baseline growth outlook for Indonesia is positive overall, with household spending expected to remain healthy as inflation stays within target despite a projected acceleration in the first half of the year.

Subdued inflation should be supportive of consumption, while capital formation could remain robust as bank lending sustains double digit growth as of February 2024. For the rest of the year, we will be keeping our eye on two key factors that could determine whether economic growth can hit our projected 5.2% YoY rate.

The first is the performance of the export sector given its substantial link to other sectors in the economy, such as the industrial sector. A renewed pickup in exports should be positive for Indonesia's industrial sector while also providing added stability for the IDR.

Secondly, we will be keeping a close watch on fiscal sustainability in particular once Prabowo begins his term. The current healthy state of the fiscal balances has been a key driver of positive sentiment towards Indonesia, and a quick deterioration could spark concerns about the fiscal sustainability of the economy.

In terms of financial markets, we expect Bank Indonesia to extend its pause well into the year, with potential rate cuts only coming about in the second half of the year. BI will prefer to maintain interest rate differentials to compensate for the now smaller trade surpluses. This means that borrowing costs and local bond yields could stay elevated in the near term, while the IDR remains on the backfoot until the projected rebound in exports can push the trade surplus back to more substantial levels.

MENAFN12042024000222011065ID1108086969

Author:

Nicholas Mapa