403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Bank Of England To Push Back Against Rising Tide Of Rate Cut Expectations

(MENAFN- ING) Markets are pricing three rate cuts in 2024 and we doubt the Bank will be too happy about that. Expect policymakers to reiterate that rates need to stay restrictive for some time. But with services inflation coming down and wage growth set to follow suit, we think investors are right to be thinking about a summer rate cut. We expect 100bp of cuts next year In this article Markets are ramping up rate cut bets, and Governor Bailey isn't happy about it Expect rate cut pushback on Thursday, but investors are right to be thinking about easing Sterling benefits from the BoE position

Shutterstock

Bank Of England, London Markets are ramping up rate cut bets, and Governor Bailey isn't happy about it

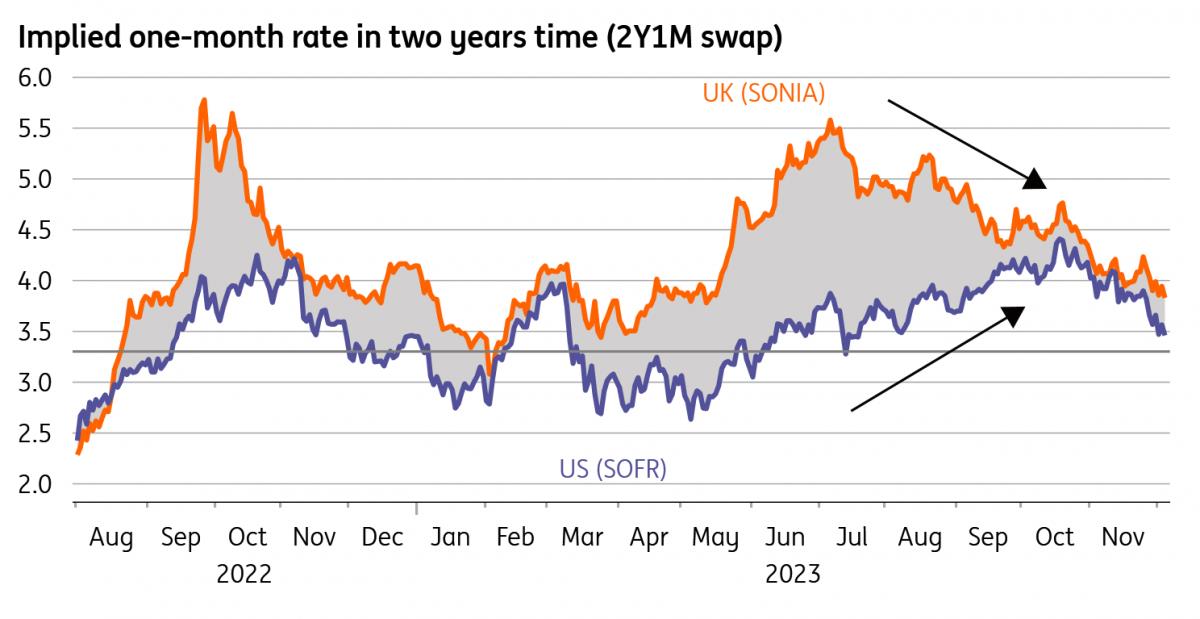

Macrobond, ING calculations Expect rate cut pushback on Thursday, but investors are right to be thinking about easing

Bank of England

Shutterstock

Bank Of England, London Markets are ramping up rate cut bets, and Governor Bailey isn't happy about it

Financial markets are rapidly throwing in the towel on the“higher for longer” narrative that central banks have been pushing hard upon for months. Even more remarkably, a small but growing number of policymakers from the Federal Reserve to the European Central Bank seem to be getting second thoughts too.

So far, that market repricing has been less aggressive for the Bank of England. Investors are expecting three rate cuts next year compared to more than five over at the ECB. The first move is seen in June, as opposed to March over in Frankfurt.

Despite that more modest adjustment, the Bank of England is starting to sound the alarm. Governor Andrew Bailey said in recent days that he is pushing back“against assumptions that we're talking about cutting interest rates".

Those comments followed a firming up of the Bank's forward guidance back in early November, where it said it expected rates to stay restrictive for“an extended period”. Its November forecasts, premised on rate cut expectations at the time, indicated that inflation may still be a touch above 2% in two years' time. That was a hint, if only a mild one, that markets were prematurely pricing easing - and rate cut bets have only been ramped up since.

Rate cut expectations are building, though less rapidly than in the US/eurozoneMacrobond, ING calculations Expect rate cut pushback on Thursday, but investors are right to be thinking about easing

That gives us a flavour of what we should expect next week. While the chances of a surprise rate hike have long since faded away, there's a good chance that the three hawks on the committee once again vote for another 25bp rate increase, leaving us with a repeat 6-3 vote in favour of no change. We only get a statement and minutes on Thursday, and no press conference or forecasts, so the opportunity to shift the messaging is fairly limited. But we expect the same hawkish forward guidance as last time, including the line on keeping rates restrictive for a prolonged period of time.

Could the Bank be tempted to go further still and formally say that markets have got it wrong? The BoE has shown itself less willing than some other central banks to either comment directly on market pricing in its post-meeting statements, or make predictions about how it'll vote at future meetings. The last time it did this was in November 2022, where disfunction in UK markets meant rate hike pricing had reached an extreme level.

We doubt they'll do something similar this month. Policymakers may be uneasy about the recent repricing of UK rate expectations, but central banks globally have learned the hard way over the last couple of years that trying to predict and commit to future policy, with relative certainty, is a fool's game.

The Bank will also be gratified that the data is at least starting to go in the right direction. Services inflation came in below the Bank's most recent forecast, and while one month doesn't make a trend, we think there are good reasons to expect further declines over 2024. Admittedly, we think services CPI will stay sticky in the 6% area through the early stages of next year, but by the summer, we expect to have slipped to 4% or below. Likewise, the jobs market is clearly cooling and that suggests the days of private-sector wage growth at 8% are behind us. We expect this to get back to the 4-4.5% area by next summer too.

Markets may be right to assume that the BoE will be a little later to fire the starting gun on rate cuts than its European neighbours. But when the rate cuts start, we think the BoE's easing cycle will ultimately prove more aggressive. We expect 100bp of rate cuts from August next year, and another 100bp in 2025.

Sterling benefits from the BoE positionSterling has enjoyed November. The Bank of England's trade-weighted exchange rate is about 2% higher. The rally probably has less to do with the UK government's stimulus and more to do with the fact that investors have been falling over themselves to price lower interest both in the US and particularly in the eurozone.

In terms of the risk to sterling market interest rates and the currency from the December BoE meeting, we tend to think it is too early for the Bank of England to condone easing expectations - even though those expectations are substantially more modest than those on the eurozone. This could mean that EUR/GBP continues to trade on the weak side into year-end - probably in the 0.8500-0.8600 range.

Into 2024, however, we expect market pricing to correct - less to be priced for the ECB, more for the UK and EUR/GBP should head back up to the 0.88 area. But that's a story for next year.

Sterling trade-weighted index edges higherBank of England

Author:James Smith, Chris Turner

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment