(MENAFN- ING) Both the retail and industrial sectors started the fourth quarter on a weaker footing than expected. The Hungarian Economy is still lacking the positive impact of domestic demand, and we don't see a sudden recovery taking place any time soon In this article Export sectors disappoint and industry fails to deliver sustainable recovery Real wage growth not an immediate remedy, retailers still suffering

Budapest, Hungary. Both industry and retail sales surprised to the downside The Hungarian Central Statistical Office (HCSO) released the October figures for the industrial and retail sectors. Both industry and retail sales surprised to the downside, although at least the latter showed growth on a monthly basis. The common denominator in both sectors is the lack of consumption and investment activity by manufacturers and retailers, which is suffering from the lost years of real wages, high interest rates and lack of fiscal leeway.

Export sectors disappoint and industry fails to deliver sustainable recovery

| -2.8% | Industrial production (YoY, wda) ING estimate: -0.2% / Previous: -5.8% |

| Worse than expected |

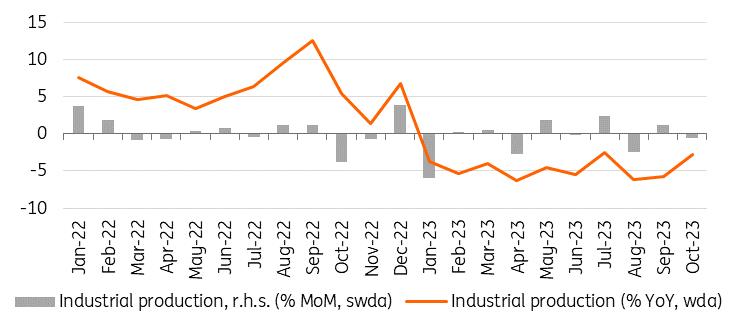

Industrial production in October was well below expectations. While output was only 2.8% lower than a year earlier on a calendar-adjusted basis, it was still a weak performance overall. Last year's low base was the reason for this improvement. This is reflected in the fact that, on a month-on-month basis, production volumes fell again by 0.6%. There is still no change in the trend for industrial production. Since the autumn of 2022, the downward trend has continued, and total output is still unable to exceed the level of output recorded after the Covid-19 pandemic at the beginning of 2021.

Performance of Hungarian industry

HCSO, ING

Detailed data is yet to be released, but according to preliminary data from the HCSO, there was no significant change in the structure of industrial production. While most sub-sectors contributed to the decline in output, the exceptions remain the manufacture of electrical equipment (battery production) and transport equipment. Capacity utilisation in industry, therefore, seems to have stabilised in October after a rebound in September following the summer shutdowns. This is surprising in view of the start-up of a new industrial capacity (Denso - Székesfehérvár ), although it is possible that production in October was still on a trial basis with minimal output.

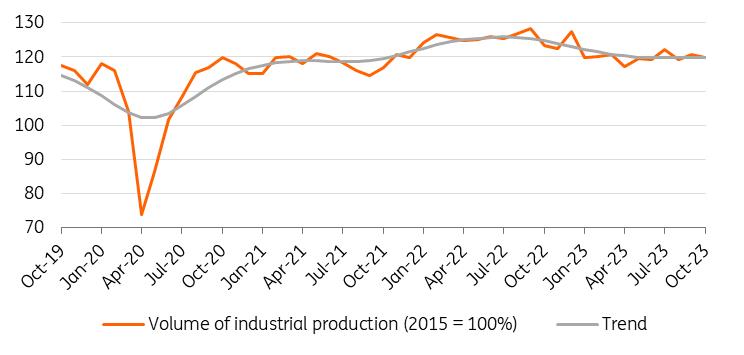

In our view, in the absence of sustained change in the economic environment, industrial production will hover around the production levels seen since the beginning of the year, with some upside risk if new capacity is able to break through the "glass ceiling". This also means that there is no reason to change our forecast for industrial production for the year as a whole. We still expect industrial production to contract by around 5-6% in 2023.

Volume of industrial production

HCSO, ING

As far as 2024 is concerned, we have seen a slight deterioration in the overall outlook over the past month. The clouds are gathering on the external demand side – notably the export-producing sectors – as European industrial performance continues to struggle to find its footing. German industry, in particular, which is still important for the Hungarian economy, is performing poorly. In addition, the Chinese economy is becoming more inward-looking, which is not really conducive to a recovery in world trade.

As a sign of the weakening external environment, the total volume of orders in industry at the end of the third quarter was only 0.3% higher than a year earlier. If new orders fall behind in the coming months, we cannot expect further significant growth from export sectors next year. However, domestic demand may try to compensate for this. while there are no signs at present that output in sectors producing for the domestic market is likely to grow rapidly in the short term, new investment (helped by the expected inflow of EU funds) and a gradual recovery in consumption should help to revive domestic demand in the second half of next year.

Real wage growth not an immediate remedy, retailers still suffering

| -6.5% | Volume of retail sales (YoY, wda) ING estimate: -5.9% / Previous: -7.3% |

| Worse than expected |

Like industry, the retail sector failed to meet market expectations in October. On a monthly basis, retail sales turnover (adjusted for seasonal and working day effects) contracted again, and the improvement in the annualised index is only a consequence of an even worse performance last October. Compared with the same period last year, sales were 6.5% lower in the tenth month of 2023.

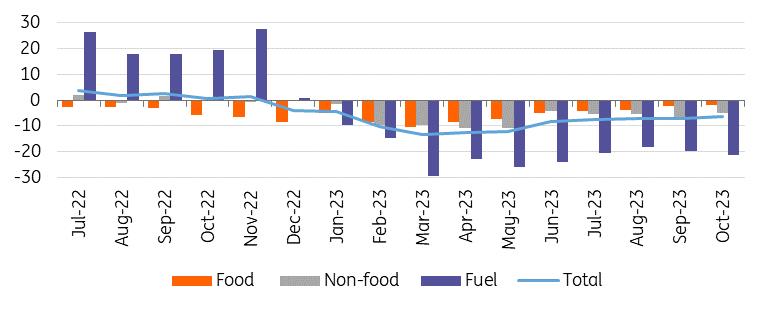

Looking at the details, we do not see much change in the structure of retail trade, but there are still some surprises. On a monthly basis, the volume of sales in food stores fell by 0.1% compared with September, meaning that the small growth of the previous month could not be maintained. So, despite a general fall in food prices, consumers remain rather cautious. This may be explained by the fact that households' purchasing power (based on real wages) is still around 2020 levels.

In contrast, it is somewhat surprising that non-food sales rose on a monthly basis in October. However, much of the 0.5% month-on-month increase was due to rising sales in second-hand shops and clothing stores. Otherwise, we continue to see a rather declining and weakening performance across the board. Where a more significant change in sales might have been expected, however, is in the fuel retailing sector. However, despite the significant fall in prices in October, total fuel sales rose only by 0.3% on a monthly basis.

Breakdown of retail sales (% YoY, wda)

HCSO, ING

The overall development of retail sales in October also shows that the increase in real wages alone is only a statistical change – and that the fact that the indicator has turned positive after a year does not change the behaviour and overall financial situation of households.

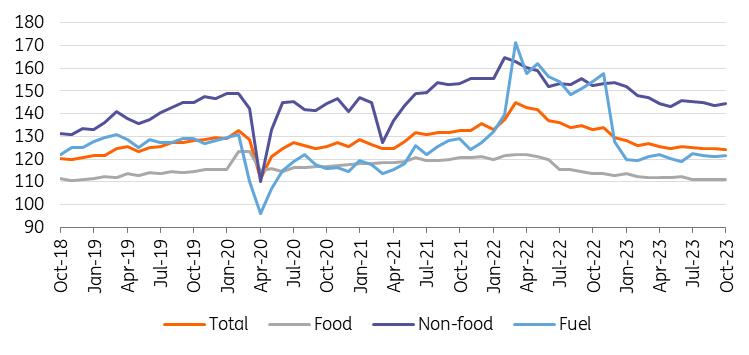

Retail sales volume in detail (2015 = 100%)

HCSO, ING

We can't see any significant and sustainable improvement in any of the segments of the retail sector that could be described as clearly encouraging and positive. The weaker-than-expected start to the fourth quarter suggests that the retail sector has a long and painful road ahead before it can make up for lost years. After all, let's not forget that the current volume of retail sales corresponds to the average volume of retail sales in 2020.

Real wages will continue to rise in the coming months, but this is unlikely to translate into dynamic consumption growth. Even so, we might still be surprised on the upside, considering the 10% and 15% minimum wage increases from December 2023 for skilled and unskilled workers, respectively. These low earners might have a higher propensity to consume, thus bringing a possible upside risk to the table.

Generally speaking, however, households will mainly deleverage and rebuild their reserves before consumption picks up. This is also reflected in the fact that consumer confidence remains at an almost 10-year low. Consumer confidence will, therefore, have to recover before households start to spend in a meaningful way. As a result, the impact of rising purchasing power is not expected to be reflected in retail sales data until 2024.

MENAFN06122023000222011065ID1107548462

Author:

Peter Virovacz, Dávid Szőnyi

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.