Date

11/30/2023 11:09:27 PM

(MENAFN- ING) Further oil supply cuts were agreed at yesterday's OPEC+ meeting, which should fully erase the surplus in 1Q24. However, the market was still left disappointed

In this article What was agreed? What does this mean for the market?

Shutterstock What was agreed?

After delaying their meeting due to a disagreement over 2024 production quotas for a handful of African members, OPEC+ finally met yesterday to discuss output policy for next year. Instead of seeing further cuts distributed amongst the whole group, it was left up to individual members to decide whether they would make deeper voluntary supply cuts.

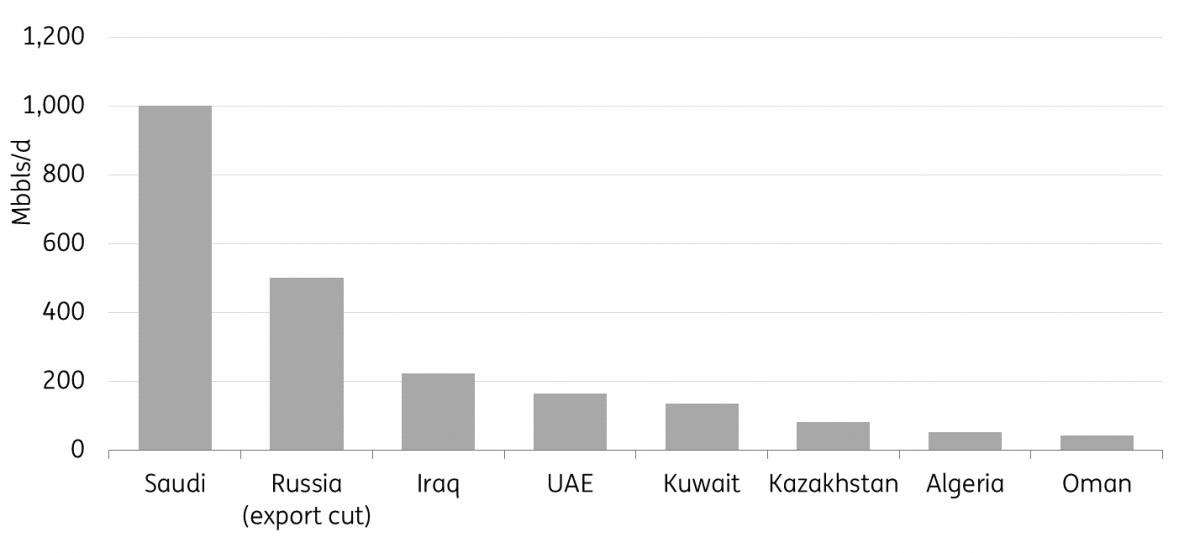

Eight members of OPEC+ decided to announce further additional cuts totalling almost 2.2MMbbls/d for 1Q24. However, this includes the rollover of Saudi Arabia's current additional voluntary cut of 1MMbbls/d, as well as Russia's export cut of 500Mbbls/d (deeper than their current 300Mbbls/d cut). We had already assumed the rollover of the Saudi and Russian cuts into 1Q24, as had most of the market. Therefore, new additional cuts of a little under 900Mbbls/d will be seen in 1Q24. These additional voluntary cuts will be brought back gradually to the market after 1Q24 depending on market conditions.

One of the key issues in the lead-up to the meeting was the production quotas set for Angola and Nigeria earlier this year. These countries were not happy with their lower output target for next year. Following an independent assessment of what these countries would be capable of producing next year, Nigeria's production target was raised from 1.38MMbbls/d to 1.5MMbbls/d. However, Angola's target was cut further from 1.28MMbbls/d to 1.11MMbbls/d. Angola has said it will not follow its new quota and will pump at 1.18MMbbls/d from January.

OPEC+ members announce additional voluntary cuts of almost 2.2MMbbls/d in 1Q24

OPEC, ING Research What does this mean for the market?

Our balance sheet shows that the additional voluntary cuts announced yesterday ensure that the marginal surplus that had been forecast for 1Q24 will be erased, and in fact, we now see a small deficit. This suggests that there is some upside to our current 1Q24 ICE Brent forecast of US$82/bbl and full-year 2024 forecast of US$88/bbl. However, this will largely depend on how OPEC+ goes about unwinding these cuts and obviously on how demand plays out next year.

The market reaction to these additional supply cuts suggests that the market was underwhelmed with the action taken by the group. The ICE Brent Feb'24 contract settled 2.44% lower on the day.

A concern for the market is the fact that these announced cuts were voluntary rather than OPEC+ wide cuts. These voluntary cuts suggest that it is becoming difficult for members to agree on OPEC+ cuts. Therefore, if further action is needed in future, it will become increasingly difficult for the group to respond.

MENAFN30112023000222011065ID1107518897

Author:

Warren Patterson

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.