403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

THINK Ahead: Gatecrashing The IMF My Top 3 Questions

(MENAFN- ING)

THINK Ahead: Gatecrashing the IMF – My top 3 questions

Source: CEIC, ING (Lynn Song) Will central bankers give us any juicy insights?

In the coming week, Washington's corridors of economic power will be bustling with the finance world's movers and shakers. It's the IMF's annual get-together, and sadly, I don't seem to have made the guest list. My invitation must be lost in the post...

But were a last-minute VIP ticket miraculously to appear on my doorstep, these would be my three burning questions:

What happens immediately after the US election?It's hard to imagine many conversations in Washington next week that don't start or end with November's looming Presidential vote. But to ask who will win feels like a wasted question. The experts tell us it'll hinge on a few tens of thousands of voters in the key swing states. And there's no easy way of guessing which way those ballots will go.

Here's a more pressing question: how do markets react in the days immediately after the vote?

The impact could be big. Our team's FX scenarios suggest EUR/USD could end the year anywhere between 1.02 and 1.12.

But it's complicated. Our US guru, James Knightley, like most analysts, reckons a Trump presidency would be more inflationary than a Harris one. The only question is whether tariffs or tax cuts come first. And, frankly, we might not know for sure for some time, particularly if some of the Congressional races go to run-offs and recounts.

Then there's the day-to-day macro story. That's still going to be a dominant force for markets, and judging from my recent chats here in London, it's hard to find many people with strong convictions about the US economy.

The data is unhelpfully mixed, and the tail risk of faster Fed easing over the winter is still there. But, as James K argues , strong retail sales and job growth numbers make it hard to see the Fed doing anything other than a 25bp rate cut next month.

The election could change a lot of things for the Fed. But the number of rate cuts we get before year-end probably isn't one of them.

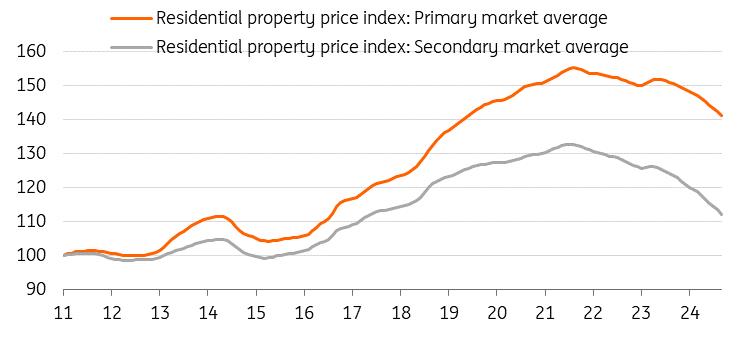

Can China's stimulus plans generate faster growth?Recent news-or the lack thereof-on China's fiscal stimulus plans has disappointed many investors. But listening to our China expert Lynn Song, recent announcements have demonstrated a renewed urgency among policymakers, even if they've so far lacked the big numbers markets crave. Lynn expects more details after the National People's Congress meets, perhaps as soon as later this month, with some reports pointing at a package of 6 trillion renminbi (845 billion USD) over three years.

Will that be enough to turn the tide? September's data reveals the fall in property prices is showing few signs of slowing, despite slightly better news on GDP. Lynn has argued for some time that stabilising the property market and increasing household earnings growth is key to restoring confidence in the domestic economy.

Whatever happens, this is a big deal for Europe. By cutting rates this week , the ECB has shown it's under no illusions about the risks to growth. The manufacturing cycle hasn't turned a corner this year, thanks in no small part to weaker global growth. Good news is needed from somewhere. Without it, as our team argued this week , Europe's surprisingly resilient jobs market is increasingly at risk.

It's worth keeping an eye on next week's purchasing managers' indices, too. Above all, it was these numbers that pushed the ECB into its rate cut this week. Further weakness would only add to the pressure to ease policy.

Chart of the week: China's property prices continue to fallSource: CEIC, ING (Lynn Song) Will central bankers give us any juicy insights?

Don't get me wrong, I'm all for chatting about big economic trends in Washington-especially if champagne is involved. But let's face it, what we're really after are some fresh insights from the central bank speakers next week, especially the ones who rarely speak up. And yep, I'm looking at you, Bank of England.

We'll hear twice from Governor Andrew Bailey, and he's already let slip that he thinks rate cuts could go faster. I expect to hear more of that next week, particularly after the welcome news on services inflation . Markets are warming to our view of back-to-back rate cuts from November onwards.

There's no shortage of ECB speakers, either. And it'll be interesting to hear if the support for this week's rate cut was quite as unanimous as President Lagarde suggested. Investors are toying with the idea of a 50bp rate cut in December. I suspect the hawks might have something to say about that...

Anyway, that's what I'll be asking next week. Well, I would if I were going. But I'm not.

Are you heading to Washington? Send your answers on a postcard...

THINK Ahead in developed marketsUnited States (James Knightley)

- Following the Federal Reserve's 50bp interest rate cut in September, the data has generally come in on the stronger side of expectations. Nonetheless, we don't think the Fed has any regrets. We see it as a risk management move. Inflation is looking better behaved, and this is giving them the flexibility to put more focus on their second target of maximising employment. By moving policy from restrictive territory towards neutral policy, they are giving the economy a bit more room to breathe in an effort to achieve its long-stated aim of a“soft landing”.

- Fed's Beige Book survey (Wed): This report collates anecdotal evidence of the state of the economy from trusted contacts and has proven to be an increasingly influential report, particularly when data quality is often questioned. Four months ago, it suggested that 9 of the 12 regional Fed banks were experiencing economic growth. The last report, published September 4, indicated that only three Fed banks reported growth, meaning that 75% (9 of 12) were experiencing either stagnant or contracting local economies. This rapid slowdown over the summer months was a likely major catalyst behind the Fed's decision to go by 50bp last month. Further evidence of weakness here should cement expectations of ongoing policy easing from the Fed.

Eurozone (Bert Colijn)

- PMI (Thu): PMIs will be key in the eurozone next week. Since May, the composite PMI has been on a declining trend, with the brief exception of August's Olympics-related bump. The September reading was below 50, signalling contraction, which has further fuelled concerns about a possible recession. These worries look overdrawn, but a slowdown is a realistic prospect for the economy. The October numbers will tell us whether the data are improving again, and if not, slowdown concerns will only grow larger.

United Kingdom (James Smith)

- PMI (Thu): Like the wider eurozone, the services PMIs have been ticking lower, consistent with more modest growth rates in the second half of the year. Last month's data also showed service-sector output prices rising at the slowest pace in over three years. If that continues, and given the latest slowdown in services inflation, the BoE can hopefully speed up the pace of rate cuts. Look out for any hints of this during Governor Bailey's appearances in Washington next week.

Canada (James Knightley)

- Policy rate (Wed): The Bank of Canada has lowered the target for the overnight rate at its past three policy meetings and is expected to follow up with a fourth consecutive cut next week. The question is, will it be another 25bp move, or will the bank follow the Federal Reserve's lead and cut by 50bp? The market favours a large move given soft inflation and weaker activity, but we think it will be a very close call and sense that a narrow majority of officials will be wary of going too far too fast.

Poland (Adam Antoniak)

-

Industrial Production (Mon): Poland's manufacturing output remains weak due to sluggish external demand, particularly from the German automotive sector and softer demand for electric cars. Rising labour costs, expensive energy, and a stronger exchange rate add to the pressure. We forecast a 0.8% YoY decline in September.

-

PPI (Mon): Producer prices have stabilised, with annual declines mainly due to high base effects from 2023. We expect a MoM decline in manufacturing prices for September, especially in coke and refined petroleum products, thanks to lower petrol prices. Lower coal costs will hit mining prices too.

-

Construction Output (Mon): Construction activity is weak, impacted by slow EU fund absorption, delayed recovery fund inflows, and the EU's highest mortgage rates. Demand for housing has eased with the expiration of the previous government's mortgage subsidies. We estimate an 11.7% YoY decline in September, following a 1.5% YoY drop in August.

-

Wages (Mon): Wage growth has eased but remains in double digits. We forecast an 11.5% YoY increase in average wages and salaries in the enterprise sector for September. We expect wage growth to slow to high single digits by 2025, potentially as soon as January, but probably not in 2024.

-

Employment (Mon): Employment levels have been slightly declining since the start of the year. We forecast a 0.6% YoY decrease in September, compared to a 0.5% decline in August, particularly in manufacturing.

-

Retail Sales (Tue): Retail sales growth slowed in Q3 2024 due to decelerating wage growth, stagnant employment, and rising inflation. Higher electricity and gas bills from July may further constrain spending. We project a 2.5% YoY sales growth for September 2024, thanks partly to a high reference base.

-

Unemployment Rate (Tue): Despite employment weakness and easing wage pressure, we expect the unemployment rate to remain low at 5.0%, unchanged from August. This is due to a shrinking domestic working-age population and slower immigration, including from Ukraine.

Hungary (Peter Virovacz)

-

Key Rate (Tue): The National Bank of Hungary is expected to keep the key rate at 6.50% next week. Despite strong verbal intervention, EUR/HUF remains in the 400-402 range, and this is the dealbreaker for the NBH. The recent inflation surprise doesn't alter this outlook. We anticipate a hawkish stance, with minimal room for further cuts due to financial market instability and rising Fed rate expectations.

-

Labour Market (Tue/Fri): The unemployment rate is expected to be 4.3%, indicating a tight labour market. Wage growth remains high at 13.6% YoY, though recent months have seen some upside surprises, so a higher figure is possible.

Czech Republic (David Havrlant)

- Confidence (Thu): Czech consumer sentiment likely softened in October due to robust service and food price rises. Increased mandatory expenditure in education and groceries are tightening household budgets. Business confidence may also see a slight correction after a previous rebound. While Czech industry is showing signs of stabilising, weak demand from European trading partners is tempering optimism.

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

More Story

Comments

No comment