(MENAFN- ING) LME copper prices are now close to where they were a year ago. Prices have fallen throughout 2023 as global monetary tightening has weighed on developed economies. The short-term demand outlook for the red metal remains weak amid recession fears, China's slowdown in the property sector, and weakening global manufacturing activity

In this article China's recovery is still uncertain Fed loosening will support copper Comfortable balance to persist in 2024 Downside risks remain short-term A strategic need for copper

Long term, the outlook for copper remains bullish because of its key role in the energy transition. But for 2024, it will be the supply and demand balance that drives the price. China's recovery is still uncertain

China was anticipated to be a bright spot for copper demand after last year's Covid lockdowns ended. Despite efforts from Beijing to stimulate the economy, China's economic recovery has mostly disappointed this year. That lacklustre recovery has weighed on copper. LME prices are now down around 11% from the year-to-date highs of $9,550.50/t in January following China's reopening after Covid lockdowns.

Over the last couple of months, the Chinese government has moved forward with a series of stimulus measures to turn around its ailing economy. But there are still concerns, particularly related to the property sector. We believe this will continue to cap gains for copper.

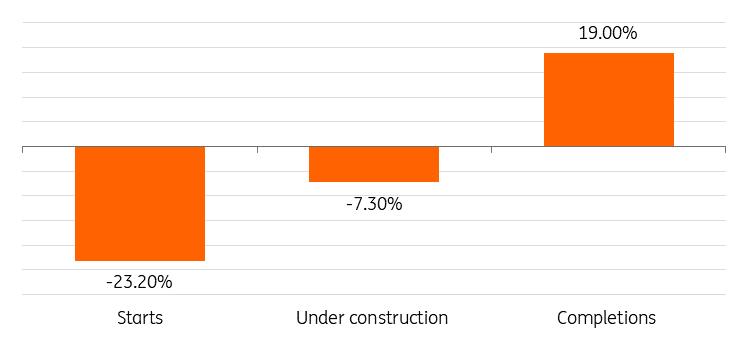

A slump in China's property market has been a major headwind to copper demand this year and a continued slowdown in the sector remains the main downside risk for the metal. While housing starts are down more than 23% this year, completions, a key source of copper consumption, have been rising. However, the 19% year-to-date rise hasn't been enough to lift copper prices. Under-construction numbers are also down, falling more than 7% year-to-date.

We believe that until the market sees signs of a sustainable recovery and economic growth in China, we will struggle to see a long-term move higher for copper prices.

Slump in Chinese property market remains a headwind to copper demand

(YTD September, % growth)

National Bureau of Statistics, ING Research Fed loosening will support copper

Elevated rates and a stronger dollar have been a drag on industrial metals in the past two years. Looking forward to 2024, copper prices will be supported by a weaker US dollar on the back of US Federal Reserve easing. We believe the Fed's interest rate path will continue to drive copper's short-term price outlook.

Our US economist expects the starting point for Fed rate cuts in the second quarter of 2024. Copper prices will benefit from looser monetary policy, which will alleviate the financial strain on manufacturers and construction companies by reducing borrowing costs. But if US rates stay higher for longer, this would lead to a stronger US dollar and weaker investor sentiment, which in turn, would translate to lower copper prices.

Comfortable balance to persist in 2024

The copper concentrates market is expected to tighten this year with smelters around the world increasing capacity, while political risks continue to increase for mining operations globally. For example, in Panama, Canada's First Quantum mine has ignited massive protests in the country and was recently forced to shut down activity. The spark for the protests was the government's decision to award the Canadian miner a renewed 20-year lease to mine the facility. Cobre Panama copper mine, an open pit mine, is one of the world's largest sources of copper, accounting for 1% of global copper output. About half of First Quantum's 750,000 tonnes of annual production comes from the flagship Cobre Panama mine. The shutdown is likely to tighten global mine supply further, however, there is still uncertainty about how long it will last.

In Peru, protests also threaten to dent the supply outlook for copper. Mining projects in Peru have long been met with opposition from communities across the country, who are concerned about the potential damage to the environment and water resources. Peru's central bank forecasts mining investments in the country will drop 18% this year and almost 8% in 2024 due to the lack of big mining projects. After Chile, Peru is the world's second-largest producer of copper.

In Chile, the world's biggest supplier of copper, Codelco is struggling to return production to pre-pandemic levels of about 1.7 million tonnes a year by the end of the decade from around 1.3 million tonnes this year, which marks the lowest level in a quarter century amid ageing assets and declining ore grade.

In a sign that the copper ore market is tightening as smelters expand, copper-concentrate supply contracts for 2024, that set processing charges, have been set 9% lower for 2024. Treatment charges are a key sign for copper's future direction. This marks the first decline in treatment and refining fees in three years and follows a six-year high set for 2023.

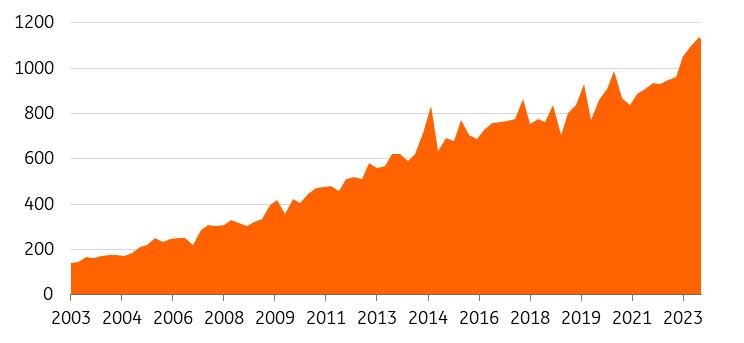

However, despite supply disruptions looming, refined metal is forecast to be in a surplus next year with Chinese production of refined copper heading for a record this year after the country's expansion of its smelting and refining capacity. The shift is largely driven by China's strategic need for copper as demand from the green energy sector grows for the red metal.

China's refined copper output hits record as smelters expand

(Thousand tonnes)

National Bureau of Statistics, ING Research

The increase in smelting is making China less dependent on imported copper metal, which might lead to an oversupply of refined metal, which sets the LME price.

China is expected to contribute around 50% of the refined global copper production in 2024. China's annual copper smelting capacity is about 8.8 million tonnes. A near-30% expansion of 2.4 million tonnes is set for completion by 2026, according to data from Antaike.

Chile's sales volumes of refined copper to China, China's traditional supplier, have been under pressure as China's own output of the metal grows. China is the biggest consumer of copper and accounts for 40% of the world's total copper imports.

Chile's Codelco recently said that Asia will represent at least 40% of its copper sales in the future, compared to 47% last year and around 60% a decade ago.

China's total imports of refined copper from Chile are on track to be the lowest since 2008 in annual volume terms. Instead of metal, China is buying more copper concentrates.

China's imports of refined copper from Chile

(metric tonnes)

General Administration of Customs, ING Research

Elsewhere, Indonesia, India, Chile and the Democratic Republic of Congo (DRC) have been expanding their copper smelter capacities, adding to concerns around oversupply. The International Copper Study Group (ICSG) forecasts copper mine supply to grow 3.7% in 2024 compared to 2023.

The DRC is set to become the second largest producer, surpassing Peru. Kamoa Kakula mine is expected to reach around 680,000 tonnes of production by 2028, becoming the fourth largest mine after Escondida, Collahuasi and Grasberg. Chinese companies own around 50% of the country's production.

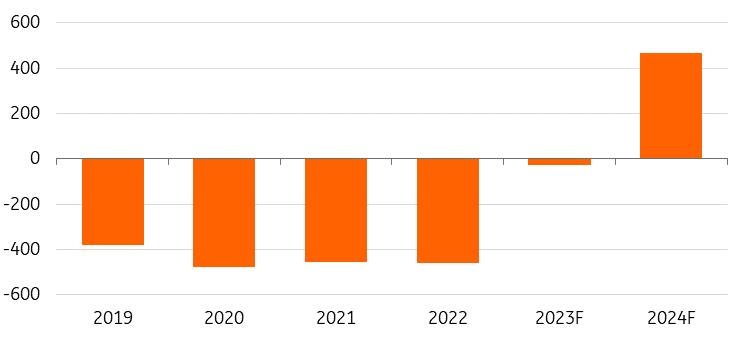

The ICSG forecasts an oversupply of 467,000 tonnes of refined metal in 2024, following a 27,000-tonne deficit this year.

Global copper market balance

(Thousand

tonnes)

ICSG, ING Research

On the demand side, copper usage is expected to contract by 1% from last year's level mainly due to weaker refined usage in the EU and North America. However, in China, apparent usage is forecast to grow by 4.3% in 2023 as green energy sectors, including power and electric vehicles, have softened the broader decline in the manufacturing sector. In 2024, global usage growth is forecasted at 2.7%.

The ICSG reports Chinese apparent demand using only reported data such as domestic production, net trade and changes in visible stocks.

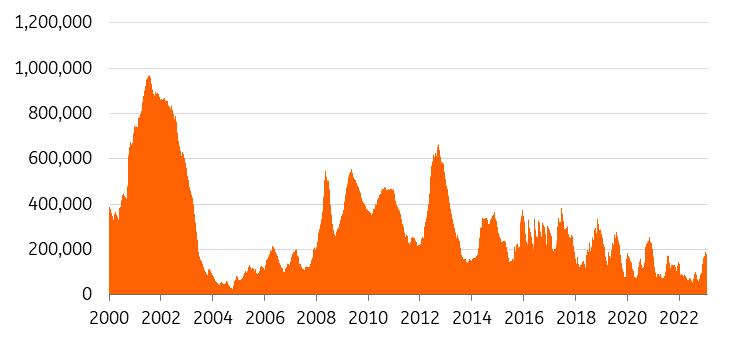

LME stocks are low, but rising

(metric tonnes)

LME, ING Research

Weak demand for copper this year has also translated into rising inventories in LME-registered warehouses, the market of last resort. LME inventories have grown from 55,000 tonnes in July to more than 180,000 currently, with the bulk of the build-up in the Americas and Europe. They now stand at the highest level in two years.

By historical standards, however, LME stockpiles of copper remain low. We believe low inventories raise the possibility of spot prices increasing rapidly if consumption picks up sooner than expected.

Meanwhile, the gap between cash prices and three-month futures has been growing. The cash three-month spread has recently hit the widest contango since the 1990s, signalling ample near-term supplies. With rising LME inventories and loosening nearby spreads, more weakness may lie ahead for copper prices.

Downside risks remain short-term

For copper, risks remain to the downside heading into the new year as the outlook for the global economy is subdued.

In particular, the uncertain outlook for China's property sector will put downward pressure on the copper market. China will continue to be the key driver of global copper demand. We believe commodity-intensive stimulus is needed to support short to medium-term demand growth. We forecast an average of $8,450/t in 2024.

Although in the longer term, the outlook for copper remains bullish because of its key role in the energy transition, for 2024, it will be the supply and demand balance that will drive the copper price, with lagging Western demand and surging Chinese production dampening the outlook in the short-term.

We believe the short-term outlook remains bearish to neutral for copper demand and we do not foresee a substantial recovery in prices before the second quarter of the year, which should mark the starting point for Fed rate cuts. We see prices averaging $8,300/t in 1Q before moving higher to $8,400/t in 2Q. Prices are likely to remain volatile through the year as markets will continue to react to macro drivers.

A strategic need for copper

Copper's future looks bright longer term as demand from green industries will continue to grow. Copper is used in everything from EVs to wind turbines and power grids.

In EVs, copper is a key component used in the electric motor, batteries, and wiring, as well as in charging stations. Copper has no substitute for its use in EVs, wind and solar energy, and its appeal to investors as a key green metal will support higher prices over the next few years.

This year, rising demand for renewables and EVs in China has already offset the slump from the more traditional sectors, like the property market.

ING forecast ING Research

MENAFN04122023000222011065ID1107533434

Author:

Ewa Manthey