403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Joint Pain Injections Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

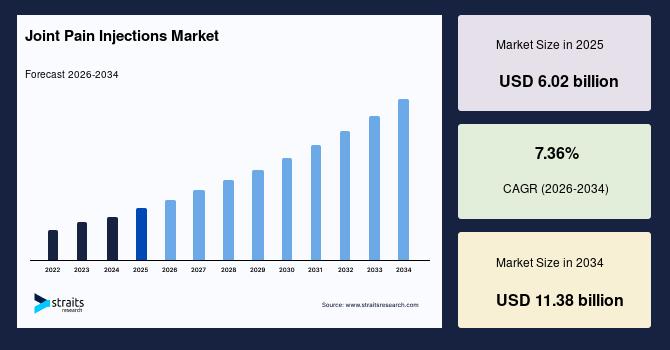

| 2025 Market Valuation | USD 6.02 billion |

| Estimated 2026 Value | USD 6.45 billion |

| Projected 2034 Value | USD 11.38 billion |

| CAGR (2026-2034) | 7.36% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Pfizer Inc., Sanofi S.A., Zimmer Biomet Holdings, Johnson & Johnson Services Inc., Bioventus LLC |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Joint Pain Injections Market Growing Shift toward Extended-release Injectable FormulationsThe shift toward extended-release injectable formulations is a key joint pain injections market trend, addressing longer-lasting pain relief in fewer clinical visits. These formulations use microsphere technology or cross-linked carriers to slowly release corticosteroids or hyaluronic acid into the joint space over weeks to months. This improves patient adherence, reduces repeat procedures, and lowers overall treatment burden in osteoarthritis management. Orthopedic clinics and hospitals increasingly prefer these products as they enhance efficiency, optimize workflow, and provide more sustained symptom control for chronic joint disorders.

Increasing Use of Ultrasound-guided Intra-articular InjectionsThe increasing use of ultrasound-guided intra-articular injections in outpatient orthopedic and sports medicine clinics is improving accuracy in delivering corticosteroids and PRP directly into knee and shoulder joints. This technique reduces procedural errors associated with blind injections and enhances clinical precision through real-time imaging. Clinics are investing in portable musculoskeletal ultrasound systems to support point-of-care visualization during procedures. Favorable reimbursement policies in developed markets are accelerating adoption, while ambulatory care centers benefit from improved patient throughput, reduced repeat injections, and better overall treatment outcomes in musculoskeletal pain management.

Joint Pain Injections Market Drivers Increasing Focus on Personalized Pain Management and Growing Sports Medicine Boom Drive MarketThe increasing focus on personalized pain management protocols is emerging as a key joint pain injections market driver, as clinicians increasingly tailor treatment regimens based on individual inflammation profiles, cartilage degradation stages, and patient comorbidities such as diabetes and obesity. This precision-based approach is moving away from standardized“one-size-fits-all” injections toward differentiated therapeutic strategies that optimize efficacy and safety for each patient segment. As a result, there is rising demand for diversified injectable portfolios, including corticosteroids, hyaluronic acid, PRP, and combination biologics, allowing physicians to match specific formulations to disease severity and progression. This personalization trend is also encouraging more frequent follow-up treatments and protocol adjustments, thereby increasing overall procedure volumes and sustained market demand.

The growing sports medicine boom, combined with a rising incidence of ligament injuries, meniscus tears, and early-onset osteoarthritis in the 30–50 age group, is emerging as a key driver for the joint pain injections market demand. Increasing participation in recreational sports and high-intensity fitness activities is leading to higher rates of joint trauma and degenerative stress at younger ages. This is driving demand for minimally invasive injectable therapies that enable faster pain relief, reduced inflammation, and quicker return to mobility without the downtime associated with surgical interventions. As a result, clinicians and patients are increasingly adopting injection-based treatments as a preferred early intervention strategy in active populations.

Joint Pain Injections Market Restraints Lack of Standardized PRP Preparation Protocols and Storage Limitations for Advanced Viscosupplementation Restrain Market GrowthA significant joint pain injections market restraint is the absence of universally accepted protocols for platelet-rich plasma preparation. Variations in centrifugation speed, platelet concentration, leukocyte content, and activation methods lead to inconsistent product quality across clinics. This lack of standardization results in highly variable clinical outcomes, making it difficult for physicians to predict efficacy or compare results across studies. Regulatory bodies and insurers remain cautious due to this inconsistency, limiting broader reimbursement and slowing integration of PRP into standardized orthopedic treatment guidelines.

Strict storage and handling requirements of high-molecular-weight hyaluronic acid formulations used in joint injections are limiting their widespread clinical adoption. These products often need controlled temperature maintenance and have restricted usability once opened, increasing the risk of wastage in routine practice. Smaller orthopedic clinics and rural healthcare facilities face operational challenges in maintaining consistent cold-chain logistics. This raises inventory costs and reduces willingness to stock premium viscosupplementation products, especially in emerging markets. As a result, access remains concentrated in advanced hospitals, restricting procedural growth in decentralized musculoskeletal care settings.

Joint Pain Injections Market Opportunities Growing Interest in Regenerative Therapies and Expansion of Employer-Sponsored Musculoskeletal Care Programs Offer Growth Opportunities for Market PlayersThe joint pain injections market opportunity is shifting toward regenerative injection therapies that aim not just to relieve pain but to actively modify disease progression through cartilage repair and joint tissue regeneration. Advances in PRP enhancements, stem-cell–adjacent biologics, and growth factor–based formulations are enabling more targeted biological healing within the joint environment. Even partial demonstration of disease-modifying osteoarthritis treatment (DMOAT) potential can significantly elevate clinical adoption and justify premium pricing. This transition is creating strong long-term repeat-use demand, as patients move from episodic symptom management to sustained joint restoration strategies.

Growing integration of employer-sponsored musculoskeletal care programs within large corporate health systems is creating a strong market opportunity for joint pain injections. Companies in IT, manufacturing, logistics, and warehousing sectors are increasingly investing in structured orthopedic care to reduce productivity loss from chronic joint disorders and workplace injuries. These programs emphasize early intervention using corticosteroid, hyaluronic acid, and PRP injections to minimize downtime and prevent long-term disability claims. This employer-driven healthcare model is strengthening demand for rapid recovery injectable therapies within occupational health frameworks and corporate wellness ecosystems.

Regional Analysis North America: Market Leadership through High Adoption of Outpatient Orthopedic Surgery and Strong Integration of Medicare Advantage PlansThe North America joint pain injections market accounted for the largest regional share of 36.27% in 2025, supported by employer-sponsored orthopedic care programs in large corporations, especially in the US, where workplace injury management prioritizes rapid-return injection therapies. High adoption of outpatient orthopedic surgery centers performing bundled injection procedures under value-based care models also supports regional dominance. Sports medicine infrastructure linked to professional leagues and collegiate athletics accelerates PRP and hyaluronic acid injection utilization for injury recovery and performance rehabilitation across the region.

The joint pain injections market in the US is growing due to strong integration of Medicare Advantage plans with value-based musculoskeletal care pathways, increasing coverage for outpatient injection procedures. High adoption of physician-owned orthopedic ASCs, which prioritize injection-based treatments for faster turnover and profitability, also supports market growth. Additionally, direct-to-specialist referral networks from urgent care and sports clinics accelerate early PRP and viscosupplementation use, supporting rapid procedural uptake across the US healthcare system.

The joint pain injections market expansion in Canada is driven by the increasing collaboration between Indigenous health services and mobile orthopedic outreach units, which improves access to joint injections in remote northern communities. Rising use of centralized provincial imaging referral systems accelerates early diagnosis of osteoarthritis, directly channeling more patients into injection-based treatment pathways before surgical consultation. Rising demand for hyaluronic acid injections and preference for minimally invasive joint pain relief also support market growth in Canada.

Asia Pacific: Fastest Growth Driven by Expansion of Private Diagnostic Imaging Chains and Increasing Adoption of Hyaluronic Acid InjectionsThe Asia Pacific joint pain injections market is expected to register the fastest growth with a CAGR of 10.85% during the forecast period, due to rapid expansion of private diagnostic imaging chains and rising adoption of outpatient orthopedic clinics in Tier-1 APAC cities. Increasing sports-related ligament injuries in countries like India, China, and Australia are driving strong demand for joint pain injections. Additionally, growing medical tourism for cost-effective PRP and hyaluronic acid therapies in Thailand and South Korea is accelerating procedural volumes and driving market growth in Asia Pacific.

China's joint pain injections market is expanding due to the expansion of tertiary orthopedic hubs in cities such as Shanghai, Beijing, and Shenzhen, which is significantly increasing adoption of hyaluronic acid and PRP injections. Integration of internet hospital platforms is accelerating follow-up injection scheduling and repeat viscosupplementation cycles. China's high prevalence of post-traumatic knee injuries among recreational badminton and table tennis players is driving demand for early intra-articular injection therapy.

The Japan joint pain injections market is led by strong adoption of locomotive syndrome screening programs, promoted by the Japanese Orthopaedic Association. High penetration of clinic-based orthopedics, where outpatient injection procedures are preferred over hospital visits due to convenience and aging demographics. Japan's cultural preference for preserving mobility without surgical intervention supports repeated viscosupplementation cycles as a long-term joint preservation strategy in elderly care pathways.

Joint Pain Injections Market Segmentation Analysis By Injection TypeBy injection type, the hyaluronic acid injections segment accounted for the largest share of 46.65% in 2025 due to its ability to improve joint lubrication, reduce pain and stiffness, enhance mobility in osteoarthritis patients, and delay the need for surgical intervention. It offers a minimally invasive, outpatient-based treatment with a good safety profile and repeat administration capability.

The platelet-rich plasma injections segment is expected to grow at a CAGR of 8.46% during the forecast period, driven by increasing demand for autologous regenerative therapy in ligament tears and tendon damage. Rising preference for biologic treatments with minimal immunogenic risk and expanding use in orthopedic clinics for early osteoarthritis management. Adoption in sports medicine and rehabilitation centers for faster tissue healing and reduced recovery time further supports demand.

By ApplicationBased on application, the knees & ankles segment accounted for the largest share of 44.20% in 2025 due to the increasing use of image-guided intra-articular injections for knee procedures. Rising adoption in post-operative rehabilitation and fracture repair further supports segment growth. Joints also show a strong response to hyaluronic acid and PRP therapies, boosting clinical preference.

The hip joints segment is expected to grow at a CAGR of 9.21% during the forecast period, fueled by the increasing incidence of avascular necrosis of the femoral head. The rising adoption of ultrasound and fluoroscopy injection techniques is improving procedural accuracy. Expanding use of injections in pre-arthroplasty pain management protocols also boosts the segment's growth.

By End UserHospitals led the end-user segment with a share of 38.82% in 2025 due to the high availability of fluoroscopy and ultrasound-guided injection infrastructure, allowing precise intra-articular delivery for complex joints. They also manage high-risk osteoarthritis and post-surgical cases requiring multidisciplinary oversight. Institutional reimbursement pathways and emergency orthopedic admissions drive higher procedural volumes compared to clinics.

The ambulatory surgical centers segment is expected to grow at a CAGR of 10.37% during the forecast, driven by increasing preference for minimally invasive joint injections requiring a short recovery time. Adoption of bundled payment models encourages cost-efficient outpatient care for corticosteroid and hyaluronic acid injections. Integration of portable ultrasound-guided injection systems in ASC settings improves procedural precision for knee and shoulder treatments.

Competitive LandscapeThe joint pain injections market landscape is moderately fragmented, involving global pharmaceutical companies, orthopedic device manufacturers, and specialized regenerative medicine firms. Major players such as Johnson & Johnson, Pfizer, Sanofi, Zimmer Biomet, and Stryker compete through established corticosteroid and viscosupplementation portfolios supported by strong clinical distribution channels. Companies like Bioventus, Anika Therapeutics, and SEIKAGAKU CORPORATION focus on hyaluronic acid-based and orthobiologic injection solutions. Competition is increasingly driven by innovation in extended-release formulations, PRP standardization systems, and minimally invasive delivery techniques.

List of Key and Emerging Players in Joint Pain Injections Market Pfizer Inc. Sanofi S.A. Zimmer Biomet Holdings Johnson & Johnson Services Inc. Bioventus LLC Anika Therapeutics Inc. Seikagaku Corporation Ferring Pharmaceuticals Fidia Farmaceutici S.p.A. Chugai Pharmaceutical Co. Ltd. Teva Pharmaceutical Industries Ltd. Viatris Inc. Reddy's Laboratories LG Chem AbbVie Inc. Lilly Arthrex Inc. Pacira BioSciences OrthogenRx Emcyte Corporation Arthrosi Avanos InduPro Therapeutics Eli Lilly and Company Novartis AG Recent Developments-

In February 2026, Sobi acquired Arthrosi Therapeutics.

In December 2025, Sanofi entered a strategic equity investment + research collaboration with InduPro Therapeutics to strengthen the immunology pipeline relevant to inflammatory joint disorders.

In October 2025, Arthrosi raised USD 153 million in Series E funding to complete Phase 3 development to support biologics/targeted therapy development for joint disease.

In July 2025, Avanos sold its hyaluronic acid (HA) knee injection line (TriVisc, GenVisc 850) to Channel-Markers Medical, LLC.

In July 2025, Pacira entered a strategic collaboration with Johnson & Johnson MedTech to expand commercialization of ZILRETTA, an extended-release corticosteroid injection for knee osteoarthritis.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.02 billion |

| Market Size in 2026 | USD 6.45 billion |

| Market Size in 2034 | USD 11.38 billion |

| CAGR | 7.36% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Injection Type, By Application, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Joint Pain Injections Market Segments By Injection Type-

Steroid Joint Injections

Hyaluronic Acid Injections

Platelet-Rich Plasma Injections

Placental Tissue Matrix & MSC Injections

Others

-

Knees & Ankles

Shoulders & Elbows

Hip Joints

Spinal Facet & SI Joints

Others

-

Hospitals

Ambulatory Surgical Centers

Orthopedic Clinics

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment