403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Ready-To-Drink (RTD) Tea Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

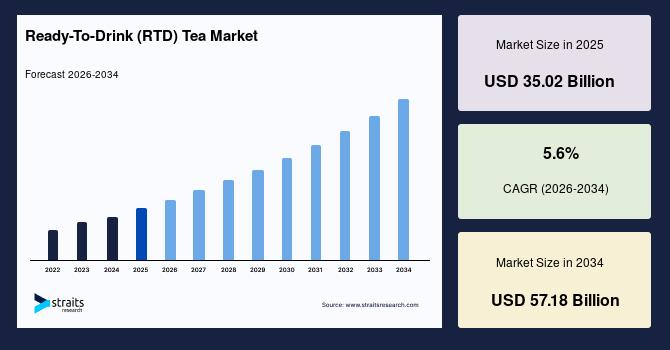

| 2025 Market Valuation | USD 35.02 Billion |

| Estimated 2026 Value | USD 36.98 Billion |

| Projected 2034 Value | USD 57.18 Billion |

| CAGR (2026-2034) | 5.6% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Danone, Harney and Sons Fine Teas, Nestle S.A., Snapple Beverage Corp., Starbucks Corporation |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Ready-To-Drink (RTD) Tea Market Rising Shift toward Tea Mocktails and Alcohol-alternative RTD BeveragesTea mocktails and alcohol-alternative RTD beverages are gaining popularity as consumers seek healthier, low- or zero-alcohol drink options. Brands are introducing botanical infusions, adaptogens, and functional ingredients to appeal to wellness-focused Gen Z and millennial consumers. Rising demand for premium non-alcoholic social beverages is accelerating innovation in clean-label, low-sugar RTD tea products. Convenient canned and bottled formats are further supporting growth across retail and café channels.

Growing Adoption of Botanical and Floral Fusion Tea BlendsA key ready-to-drink tea market trend is the shift toward botanical and floral fusion tea blends featuring ingredients such as hibiscus, lavender, chamomile, jasmine, and rose for unique flavors and wellness benefits. Social media trends and café culture are boosting demand for visually appealing and aromatic tea infusions. Premium herbal teas offering relaxation, digestion support, and stress-relief benefits are gaining traction in urban markets. Companies are also focusing on organic ingredients, clean-label formulations, and sustainable packaging to enhance product appeal. For instance, Tata Consumer Products has expanded its premium herbal tea portfolio to address rising demand for healthier beverages.

Ready-To-Drink (RTD) Tea Market Drivers Increasing Use of Smart Packaging and Rise of Hybrid Tea-based Functional Beverage Formulations Drives MarketThe increasing use of smart packaging with freshness monitoring labels is rising as brands focus on improving product transparency, which drives ready-to-drink tea market demand. These labels help consumers easily track product freshness, which increases trust in packaged beverages. They also support better quality assurance by indicating storage conditions and shelf-life status in real time and benefit by reducing product returns and improving supply chain efficiency through better inventory control. Retailers gain improved shelf management as near-expiry products can be quickly identified and managed.

A key ready-to-drink tea market driver is the rise of hybrid tea-based functional beverage formulations, which combines traditional tea extracts with functional ingredients. These products are designed to deliver both refreshment and added health benefits such as energy support and improved focus and are blending tea with vitamins, minerals, and plant-based compounds to enhance product value. It also benefits busy professionals and young consumers who prefer convenient wellness solutions in a single beverage. Overall, this innovation is helping brands differentiate their offerings and strengthen the growth in the market.

Ready-To-Drink (RTD) Tea Market restraints Flavor Stability Issues and Intense Competition from Energy and Sports Drinks Restrain Market GrowthFlavor stability in long shelf-life products remains a key ready-to-drink tea market restraint due to the breakdown of volatile compounds over time. Oxidation, temperature fluctuations, and moisture or oxygen exposure during storage can cause off-flavors and weaken taste consistency. Packaging limitations and preservative interactions further affect flavor integrity. Maintaining a stable taste profile across extended shelf life therefore requires highly sensitive formulations.

The ready-to-drink tea market also faces intense competition from established energy and sports drink brands with strong consumer loyalty and extensive distribution networks. Aggressive marketing, price promotions, and bundled offerings reduce visibility for emerging beverage players. Consumers often prefer familiar products that provide quick energy or hydration benefits, limiting brand switching. This creates significant barriers for new entrants and alternative beverage categories.

Ready-To-Drink (RTD) Tea Market Opportunities Rising Popularity of RTD Coffee and Increasing Adoption of Premium Sparkling Tea Formats Offer Growth OpportunitiesThe rapid growth of RTD coffee consumption is creating strong opportunities for ready-to-drink tea market growth, as consumers increasingly adopt convenient, on-the-go caffeinated beverages. Consumers familiar with bottled and canned coffee are becoming more open to ready-to-drink tea variants such as iced tea, green tea, and herbal blends that offer added health benefits like antioxidants and lower sugar content. This crossover trend is encouraging manufacturers to introduce premium flavors, functional ingredients, and innovative hybrid beverage formats to capture evolving consumption preferences. The Coca-Cola Company has leveraged its RTD beverage expertise with brands like Gold Peak and Honest Tea, expanding iced tea offerings to compete directly with the growing RTD coffee segment by emphasizing convenience and flavor variety.

The growing adoption of premium sparkling tea formats is creating opportunities among health-conscious consumers seeking low-sugar and natural beverages. Rising demand for alcohol-free social drinks offers a significant ready-to-drink tea market opportunity. Sparkling tea is positioned as a premium alternative for social occasions. Brands are also innovating with exotic flavors and botanical blends to attract younger urban consumers. Expanding café culture and premium retail beverage sections are further improving product visibility and accessibility.

Regional Insights North America: Market Leadership through Expansion of Private Label Ready-to-drink Tea and Fast-paced Urban LifestyleThe North America ready-to-drink tea market accounted for the largest regional share of 49.3% in 2025 supported by the high preference for standardized packaged beverages among consumers across the region. Busy urban lifestyles encourage people to choose ready-made tea products that offer consistent taste, quality, and convenience. The well-established retail and convenience store network further strengthens product availability, making ready-to-drink tea an easy grab-and-go option. Consumers also trust branded packaged beverages due to strict quality regulations and labeling standards, which enhances confidence in repeat purchases.

The ready-to-drink tea market expansion in the US is driven by private-label offerings across major retail chains targeting price-sensitive consumers. Retailers are introducing diverse variants such as unsweetened, lightly sweetened, and fruit-infused teas to match evolving preferences. Increased shelf space for store brands is further improving product visibility and purchase frequency.

The Canada ready-to-drink tea market growth is supported by rising demand for convenient and healthier beverage alternatives among urban consumers. Strong retail penetration and the expansion of premium and organic RTD tea variants are boosting accessibility and consumer interest. Seasonal demand, along with innovation in herbal and botanical-infused flavors, is further strengthening market growth.

Asia Pacific: Fastest Growth Driven by Expansion of Domestic Tea Chains and Rising Adoption of Flavored and Chilled TeaThe Asia Pacific ready-to-drink tea market is expected to grow at a CAGR of 11.8% driven by strong demand for flavored and sweetened tea variants. The region shows exceptional acceptance of sweetened RTD tea due to its alignment with local taste, rapid urban expansion which supports higher consumption of convenient bottled tea products across daily routines. Expanding youth population further strengthens demand for fruit-infused and dessert-style tea beverages with varied sweetness levels and strong penetration of modern retail and quick-service outlets, increasing product visibility and trial frequency.

China's ready-to-drink tea market is driven by domestic tea chains expanding into bottled beverage formats to commercialize their popular freshly brewed offerings. Strong brand loyalty, urban lifestyles, and expanding retail and convenience store networks are supporting product demand. Digital platforms and delivery services are further accelerating sales of RTD beverages.

The India ready-to-drink tea market is growing due to rising demand for flavored and chilled tea among urban consumers. Younger consumers are increasingly preferring fruit-infused, masala, and herbal tea variants for convenience and taste variety. Expansion of quick-commerce, modern retail, café culture, and awareness of packaged beverage hygiene is further boosting branded ready-to-drink tea consumption.

Ready-To-Drink (RTD) Tea Market Segmentation Analysis By TypeBlack tea led the type segment in the ready-to-drink tea market with a share of 30.22% in 2025 due to its deep cultural integration as a primary beverage in traditional tea-drinking regions and its established acceptance across households, foodservice, and institutional settings. The segment benefits from strong familiarity, routine consumption patterns, and wide consumer preference across age groups.

The specialty & functional tea segment is expected to grow at a CAGR of 7.8% during the forecast period, driven by rising consumer preference for wellness-oriented beverages, where buyers actively seek drinks that support immunity, energy, and overall well-being. Increasing health consciousness among urban populations is encouraging a shift from conventional sugary beverages toward functional tea options with added benefits.

By Sweetening TypeThe sweetened tea segment accounted for the largest share of 62.66% in 2025 in the sweetening type segment. Strong consumer preference for taste-enhanced beverages in mass-market consumption and higher appeal across age groups due to palatable taste drive segment growth.

The low/zero sugar tea segment is expected to grow at a CAGR of 8.4% during the forecast period, fueled by increasing focus on metabolic health, reduced sugar intake in daily beverages, and rising awareness of lifestyle-related health risks.

By Tea ConcentrationBy tea concentration, brewed tea accounted for a share of 58.62% in 2025 due to its wide usage in large-scale bottling and mass production systems. Uniform quality across high-volume production lines, established processing infrastructure, and strong scalability for mass-market distribution drive segment growth.

The tea concentrates segment is expected to grow at a CAGR of 8.3% during the forecast period, fueled by its strong suitability for on-demand mixing in foodservice and QSR outlets. It enables operators to serve large volumes efficiently while maintaining standardized taste across multiple servings.

By CategoryBy category, the conventional segment is expected to grow at a CAGR of 13.8% during the forecast period. Higher shelf stability supporting long-distance distribution and bulk stocking strengthens its dominance across large retail and wholesale networks. This stability allows manufacturers to maintain consistent supply chains, reduce wastage risks, and efficiently distribute products to both urban and rural markets.

The organic segment is expected to grow at a CAGR of 6.5% during the forecast period, driven by the expansion of specialty health-focused retail outlets and organic stores. This channel provides better visibility and targeted access to health-conscious consumers, enabling brands to position organic RTD tea as a premium and trustworthy option.

By AdditivesBy additives, flavors accounted for a dominant share of 55.39% in 2025 due to their cost-effective formulation to enhance taste appeal without significantly increasing production costs. This allows scalable product development, wider pricing flexibility, and strong penetration across both premium and value-driven consumer segments in global markets.

The nutraceuticals segment is expected to grow at a CAGR of 11.6% during the forecast period, driven by its positioning as having preventive health benefits, encouraging regular consumption beyond basic hydration needs. Beverage manufacturers are integrating vitamins, minerals, and plant-based bioactive into RTD formulations to enhance perceived functional value.

By PackagingBased on packaging, PET bottles accounted for a share of 48.52% in 2025 due to their high compatibility with automated filling and packaging lines. PET bottles support continuous manufacturing processes, improve production speed, and ensure consistent packaging quality. Their adaptability to high-throughput systems strengthens cost efficiency and supports widespread industrial adoption.

The cartons segment is expected to grow at a CAGR of 7.8% during the forecast period, supported by increasing adoption in shelf-stable beverage formats with extended usability. Carton packaging supports efficient storage and transport while preserving product integrity in diverse climatic conditions.

By Price RangeEconomy led the price range segment with a share of 56.43% in 2025 due to high affordability that aligns with daily consumption habits of price-sensitive consumers. This benefits from strong demand among mass-market buyers who prioritize low-cost beverage options for regular use. It also supports high-volume sales through widespread availability in local retail outlets and convenience stores.

The premium segment is expected to grow at a CAGR of 16.8% during the forecast period, fueled by increasing preference for high-quality beverage experiences among urban consumers. Rising disposable income and evolving lifestyle choices are encouraging consumers to trade up from standard beverages to premium offerings with superior taste and ingredient quality.

By Distribution ChannelThe offline distribution channel is expected to grow at a CAGR of 18.2% during the forecast period, driven by the strong presence of established retail infrastructure such as supermarkets, hypermarkets, convenience stores and extensive networks. It also supports frequent purchase cycles through routine shopping behavior in organized retail outlets. The availability of chilled storage in modern retail formats further enhances product appeal and encourages immediate consumption.

The online distribution channel is expected to grow at a CAGR of 9.7% during the forecast period, driven by the growing preference for home delivery convenience and busy urban lifestyles. This channel enables seamless access to a wide variety of RTD tea products through mobile applications and e-commerce platforms. Scheduled delivery options and doorstep fulfillment further enhance consumption convenience for daily beverage needs.

Competitive LandscapeThe ready-to-drink tea market landscape is highly fragmented, with the presence of multinational beverage giants, regional tea manufacturers, niche wellness brands, and emerging startup players competing across different price and product segments. Established players mainly compete on strong distribution networks, consistent product quality, brand loyalty, and large-scale retail partnerships that ensure wide availability. They also focus on product portfolio expansion, packaging innovation, and strategic marketing to maintain dominance in mature markets. Emerging players in the ready-to-drink tea market is competing by targeting niche demand areas such as functional tea, organic ingredients, unique flavor combinations, and locally inspired recipes, while also leveraging digital-first sales channels and agile product development. Price competitiveness and rapid innovation cycles further help smaller brands in the ready-to-drink tea market gain visibility.

List of Key and Emerging Players in Ready-To-Drink (RTD) Tea Market Danone Harney and Sons Fine Teas Nestle S.A. Snapple Beverage Corp. Starbucks Corporation Beam Suntory Inc. Tata Consumer Products Limited The Coca-Cola Company The Republic of Tea Unilever Plc. Gardens of India Grand Hyatt Gurgaon Reliance Consumer Products Naturedge Beverages Suntory Holdings Limited Recent Developments-

In August 2025, Gardens of India and Grand Hyatt Gurgaon entered an exclusive tea partnership supplying curated premium RTD-style tea experiences across hospitality formats.

In August 2025, Reliance Consumer Products (RCPL) acquired a majority stake in a joint venture with Naturedge Beverages to strengthen its entry into the herbal and tea-based functional RTD beverage segment, including green tea–infused Ayurvedic drinks under its“Shunya” portfolio.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35.02 Billion |

| Market Size in 2026 | USD 36.98 Billion |

| Market Size in 2034 | USD 57.18 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Sweetening Type, By Tea Concentration, By Category, By Additive, By Packaging, By Price Range, By Distribution Channel |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Ready-To-Drink (RTD) Tea Market Segments By Type-

Green Tea

Black Tea

Herbal Tea

Oolong Tea

Matcha Tea

Specialty & Functional Tea

White Tea

Fruit Tea

-

Sweetened

Unsweetened

Low/Zero Sugar

-

Brewed Tea

Tea Concentrates

Powder-Mix RTD Tea

-

Organic

Conventional

-

Flavors

Artificial Sweeteners

Acidulants

Nutraceuticals

Preservatives

Others

-

Glass Bottles

Cans

PET Bottles

Cartons

Fountain Dispensing

Pouches

Others

-

Economy

Mid-range

Premium

-

Offline

Online

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment