403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Satellite Commercial-Off-The-Shelf (COTS) Components Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

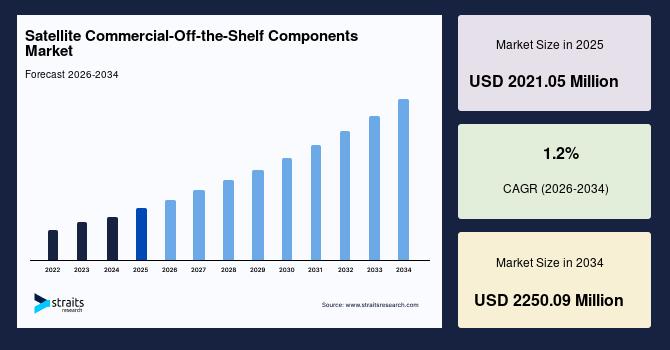

| 2025 Market Valuation | USD 2021.05 Million |

| Estimated 2026 Value | USD 2045.3 Million |

| Projected 2034 Value | USD 2250.09 Million |

| CAGR (2026-2034) | 1.2% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Europe |

| Key Market Players | Analog Device, Microchip Technology, Micropac, BAE System, Curtiss-Wright |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Satellite Commercial-Off-the-Shelf (COTS) Components Market Growing Inclination toward AI-enabled Onboard Edge ProcessingA key satellite commercial-off-the-shelf (COTS) components market trend is the shift toward AI-enabled onboard edge processing to transform satellite systems, enabling real-time data analysis directly in orbit. Satellites are increasingly using commercial processors and AI modules to process images, communication signals, and sensor data without relying heavily on ground stations. This reduces latency and improves mission responsiveness for time-sensitive applications such as surveillance and earth observation. COTS-based AI hardware also allows faster deployment of intelligent satellite functions at lower development cost and supports continuous software updates, making satellites more adaptive to changing mission needs.

Rising Adoption of Modular Plug-and-Play Satellite Bus ArchitectureThe adoption of modular plug-and-play satellite bus architecture is emerging as another satellite commercial-off-the-shelf (COTS) components market trend. Satellite manufacturers are increasingly designing standardized bus systems that allow quick integration of different subsystems without extensive redesign and reduce development time and simplify mission customization for varied applications. It also enables faster upgrades of payloads and electronics during production cycles. Companies benefit from lower engineering complexity and improved scalability in satellite manufacturing.

Satellite Commercial-Off-the-Shelf (COTS) Components Market Drivers Rising Demand for Reconfigurable Satellite Payloads and Expanding Small Satellite and CubeSat-based Missions Drives MarketThe increasing adoption of reconfigurable satellite payloads is driving the satellite commercial-off-the-shelf (COTS) components market demand, as operators seek flexible, software-defined, and cost-efficient space systems. Modern satellites are increasingly designed to adjust communication frequencies, processing loads, and mission functions after launch, which require highly adaptable and rapidly upgradable electronic components. COTS components support this need by offering standardized, readily available, and lower-cost alternatives to fully custom space-grade hardware, enabling faster development cycles and improved mission agility. This shift toward software-defined and reprogrammable satellite architecture is significantly boosting the uptake of COTS-based solutions in both commercial and defense space programs.

A key satellite commercial-off-the-shelf (COTS) components market driver is the rising expansion of small satellite and CubeSat-based missions. These missions reduce overall mission cost by using compact and lightweight systems that rely heavily on standardized electronic parts. Faster development cycles of CubeSats encourage the use of readily available COTS components to accelerate deployment timelines. Space agencies and private companies are increasingly adopting these small platforms for Earth observation, communication, and scientific experiments. The modular design of small satellites supports easy integration of multiple COTS-based subsystems.

Satellite Commercial-Off-the-Shelf (COTS) Components Market Restraints Limited Space-validated Long-term Performance Data and Rapid Component Obsolescence Restrain MarketLimited space-validated long-term performance data restrains the satellite commercial-off-the-shelf (COTS) components market, as newer components often lack proven reliability in extended orbital conditions. This creates hesitation among satellite manufacturers when selecting components for critical missions. Without sufficient historical performance records, it becomes difficult to predict durability under radiation, thermal cycling, and vacuum stress. Space agencies and commercial operators therefore depend on conservative design approaches that slow adoption of newer COTS technologies. The uncertainty also increases testing requirements, which raises development time and cost.

A major satellite commercial-off-the-shelf (COTS) components market restraint is obsolescence risk. Frequent upgrades in semiconductor and processing technologies make existing components outdated within short product cycles. This forces satellite manufacturers to redesign systems or secure long-term inventories before launch and increases planning complexity for space missions that require stable and consistent hardware over many years. The issue also raises concerns about compatibility between new and older satellite subsystems.

Satellite Commercial-Off-the-Shelf (COTS) Components Market Opportunities Expansion of Space-based IoT Connectivity Networks and Rising Adoption of COTS in Space Robotics Offer Growth OpportunitiesThe expansion of space-based IoT connectivity networks is creating opportunities for satellite commercial-off-the-shelf (COTS) component integration across global communication systems and enables seamless data transmission from remote sensors, ships, aircraft, and industrial assets through satellite-linked IoT infrastructure. This growth increases demand for cost-efficient and scalable electronic components that can support large satellite constellations. COTS solutions help reduce deployment time while maintaining functional reliability in connected space systems and support industries such as agriculture, logistics, and environmental monitoring by improving real-time data access.

A key opportunity for the satellite commercial-off-the-shelf (COTS) components market growth stems from space robotics. This presents opportunities in satellite servicing, in-orbit maintenance, and autonomous mission operations. These components help reduce system complexity in robotic arms, inspection units, and docking mechanisms used in space environments. Their availability supports faster development of cost-efficient robotic platforms for satellite repair and debris removal missions. Space agencies and private players are increasingly integrating COTS-based electronics to enhance flexibility and reduce development time and enable scalable robotic systems for future orbital infrastructure management.

Regional Insights North America: Market Leadership through Rising Investment in Dual-use Space Technologies and Expansion of Aerospace Engineering HubsThe North America satellite commercial-off-the-shelf (COTS) components market accounted for a share of 45.32% in 2025 due to a highly advanced and commercially active space industry. The high adoption of private space commercialization and reusable launch ecosystems across the region is driving companies to reduce launch costs and improve mission frequency through reusable rockets and standardized satellite architectures. This shift has significantly boosted the demand for COTS components, as they enable faster integration, lower production timelines, and scalable satellite manufacturing. This ecosystem is led by strong participation from private aerospace firms and satellite constellation operators, supported by expanding commercial satellite programs.

The satellite commercial-off-the-shelf (COTS) components market in the US is driven by rising investment in dual-use space technologies. This increasing alignment between civilian space missions and defense-oriented applications enables shared infrastructure and faster technology deployment. The use of COTS components plays a vital role in reducing development costs and accelerating mission readiness for such dual-purpose systems and allows manufacturers to scale production efficiently while maintaining performance standards for both commercial and defense requirements.

Canada's satellite commercial-off-the-shelf (COTS) components market is supported by the expansion of aerospace engineering hubs across the country. These hubs are strengthening capabilities in satellite design, testing, and integration, enabling faster development of cost-efficient space systems. Increasing collaboration between universities, research institutions, and private aerospace companies is driving innovation in modular satellite technologies.

Asia Pacific: Fastest Growth Driven by Rapid Scaling of Domestic LEO Satellite Networks and Rapid Growth of Startup-driven ManufacturingThe Asia Pacific satellite commercial-off-the-shelf (COTS) components market is expected to grow at a CAGR of 18.3% during the forecast period, driven by rapid expansion of national satellite launch programs, and is witnessing accelerated satellite deployment supported by government-backed space missions and increasing private sector participation in low-cost satellite manufacturing. Rapid growth in communication, earth observation, and navigation satellite programs is pushing demand for standardized and cost-efficient COTS components and is focusing on building self-reliant satellite ecosystems, which is further strengthening launch frequency and production scalability. The expanding investment in small satellite constellations and reusable launch capabilities is enhancing operational efficiency across missions.

The satellite commercial-off-the-shelf (COTS) components market in China is advancing through rapid scaling of domestic LEO satellite networks designed for communication, earth observation, and navigation applications. The increasing shift toward standardized and modular satellite architecture has significantly boosted the adoption of COTS components to enable faster production cycles and cost-efficient deployment, and a focus on building self-reliant space infrastructure encourages the integration of commercial-grade electronic systems across both government and private missions.

The India satellite commercial-off-the-shelf (COTS) components market is led by the rapid growth of a startup-driven small satellite manufacturing ecosystem and a surge in private space startups focused on designing, building, and deploying low-cost small satellites for communication, earth observation, and analytics applications. This ecosystem is supported by increasing participation in launch services, satellite bus development, and modular component manufacturing under government-backed reforms.

Satellite Commercial-Off-the-Shelf (COTS) Components Market Segmentation Analysis By Mass ClassBased on mass class, small satellites (0–500 kg) accounted for a dominant share of 53.16% in 2025 due to rising demand for low-power electronic architectures in miniaturized spacecraft, as compact satellites require energy-efficient processors, sensors, and communication modules to maximize operational performance within limited power capacity. COTS-based low-power components help improve thermal efficiency, extend mission duration, and support lightweight satellite designs.

The medium satellites (501–1,000 kg) segment is expected to register a CAGR of 9.11% during the forecast period, driven by rising investment in next-generation weather and climate monitoring satellites. Medium satellites provide higher payload capacity and longer mission endurance, making them suitable for continuous atmospheric analysis, disaster forecasting, and environmental monitoring missions using scalable COTS-based electronic systems.

By Orbit TypeBy orbit type, the low earth orbit (LEO) segment accounted for the largest share of 72.16% in 2025. This dominance is driven by strong suitability for small satellite constellations and commercial broadband expansion, enabling large-scale network deployment with faster connectivity. It supports scalable infrastructure for high-speed data services and encourages frequent satellite launches for continuous coverage improvement and benefits from growing demand for global digital connectivity solutions.

The medium earth orbit (MEO) segment is expected to grow at a CAGR of 7.2% during the forecast period, supported by growing investment in resilient communication infrastructure for global connectivity. MEO satellites are increasingly used in navigation and communication systems that require balanced coverage with fewer satellites than LEO networks.

By ComponentCommunication led the component segment, accounting for a share of 33.12% in 2025 due to higher integration of secure communication electronics for defense missions. COTS-based communication components support secure real-time connectivity between military satellites, ground stations, and tactical networks while reducing subsystem development complexity and deployment timelines.

The command & data handling system is expected to grow at a CAGR of 8.4% during the forecast period, driven by the rising integration of high-speed onboard data processing systems. This enhances real-time decision-making and improves overall mission responsiveness without relying heavily on ground-based processing.

By ApplicationBased on application, earth observation accounted for a share of 56.21% in 2025 due to the strong adoption of real-time land-use change detection systems. COTS-based electronic components support faster data acquisition and processing, allowing timely insights for government agencies, environmental bodies, and commercial mapping providers.

The communication segment is expected to grow at a CAGR of 13.6% during the forecast period, fueled by rising adoption of direct-to-device satellite communication services. Increasing demand for high-performance COTS communication components supports seamless signal transmission, low-latency connectivity, and scalable satellite network expansion.

By End UserBy end user, government & space agencies accounted for a share of 48.19% in 2025, supported by large-scale national space programs. Continuous procurement of standardized satellite systems for long-duration missions for consistent mission performance also drive segment growth.

The commercial space companies segment is expected to grow at a CAGR of 22.4% during the forecast period, driven by growing investment in scalable satellite platforms. This enables private operators to rapidly expand constellation size, optimize production efficiency, and support diversified commercial space applications through flexible and cost-effective COTS-based satellite architecture.

Competitive LandscapeThe satellite commercial-off-the-shelf (COTS) components market is moderately fragmented, with the presence of large aerospace electronics companies, semiconductor manufacturers, satellite subsystem providers, and emerging private space technology firms competing across different application areas. Established players mainly compete on factors such as radiation-tolerant performance, long-term reliability, mission qualification capabilities, advanced processing technologies, and strong relationships with defense and space agencies. These companies also focus heavily on scalable production capacity and integration support for complex satellite missions. Emerging players compete through rapid innovation, cost-efficient component development, flexible manufacturing models, and faster customization for small satellite and CubeSat applications. Startup-driven firms are increasingly targeting low-cost commercial space programs with modular and software-defined solutions that shorten deployment timelines.

List of Key and Emerging Players in Satellite Commercial-Off-the-Shelf Components Market Analog Device Microchip Technology Micropac BAE System Curtiss-Wright Data Device Corporation GSI Technology Inc Honeywell International Infineon Technologies Mercury Systems Inc. EchoStar MDA Space Airbus Safran Data Systems (Syrlinks) Eutelsat Recent Developments-

In August 2025, EchoStar selected MDA Space as prime contractor for a 200+ satellite LEO direct-to-device constellation, with design emphasizing software-defined architecture and modular COTS-based subsystems for mass production scalability.

In June 2025, Airbus selected Safran Data Systems (Syrlinks) to supply TT&C (Tracking, Telemetry & Command) systems for ~100 LEO satellites in Eutelsat's constellation, using COTS-based architectures to reduce cost and improve scalability in mass satellite production.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2021.05 Million |

| Market Size in 2026 | USD 2045.3 Million |

| Market Size in 2034 | USD 2250.09 Million |

| CAGR | 1.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Mass Class, By Orbit Type, By Component, By Application, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Satellite Commercial-Off-the-Shelf Components Market Segments By Mass Class-

Small Satellites (0–500 kg)

Medium Satellites (501–1,000 kg)

Large Satellites (Above 1,000 kg)

-

Low Earth Orbit (LEO)

Medium Earth Orbit (MEO)

Geostationary Orbit (GEO)

-

Payload

Electrical & Power Subsystems

Command & Data Handling Systems

Communication Subsystems

Propulsion Subsystems

Others

-

Earth Observation

Communication

Navigation & Positioning

Scientific Research

Deep Space Missions

Others

-

Commercial Space Companies

Government & Space Agencies

Defense Organizations

Academic & Research Institutions

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment