403

Sorry!!

Error! We're sorry, but the page you were

looking for doesn't exist.

Bank Of Canada Is Not Afraid Of Diverging From The Fed

(MENAFN- ING)

A dovish cut

Source: ING, Bank of Canada, Federal Reserve BoC doesn't seem concerned about Fed divergence

The bank of Canada cut rates by 25bp to 4.50% today, in line with our call and market pricing. The accompanying statement and press conference opening remarks by Governor Tiff Macklem reinforced market expectations for more rate cuts.

Macklem put more emphasis on downside risks for the economy:“We need growth to pick up so inflation does not fall too much, even as we work to get inflation down to the 2% target”. That is a rather dovish point, further reinforced by this remark:“it's reasonable to expect further cuts”. At the same time, some words of caution on disinflation were understandably included in the statement and the meeting-by-meeting, data-dependent approach remains the basis for further policy decisions.

New quarterly projections were released, and include headline and core inflation hitting the 2.0% target by the end of next year. GDP for 2024 was revised lower from 1.5% to 1.2% and from 2.2% to 2.1% in 2025.

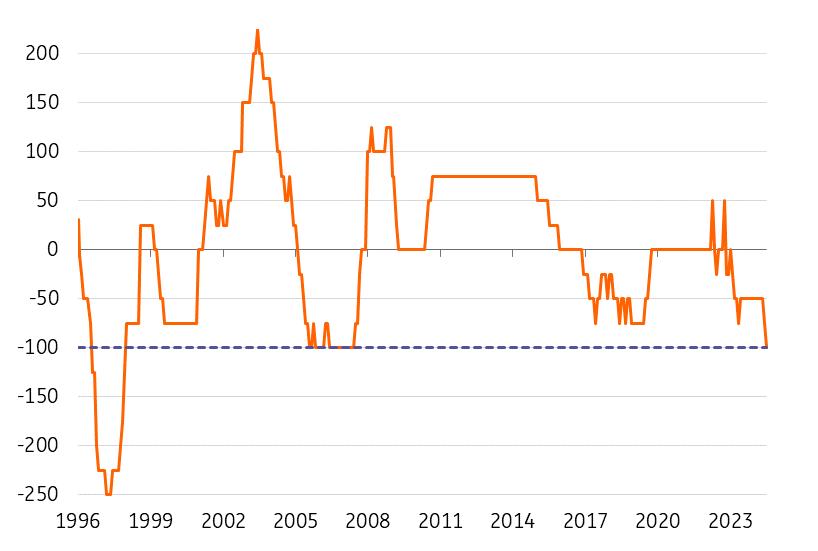

BoC-Fed policy rate differential (bp)Source: ING, Bank of Canada, Federal Reserve BoC doesn't seem concerned about Fed divergence

One concern that had led some analysts to call for a hold today is the widening gap between BoC and Fed rates, which currently stands at -100bp. That is the widest negative spread since 2007, and should the BoC cut again before the Fed, it would be the widest in over 25 years. But is this really a concern for the BoC?

Governor Macklem said today that he does not expect policy divergence from the Fed to be a serious issue. This is understandable, considering the disinflation process is at a more advanced state in Canada compared to the US, and the jobs market is crucially looser, with Canadian unemployment at 6.4%, which is 2.3% above the US one.

On the FX side, there may be some concerns that that CAD weakens excessively against USD on the back of BoC-Fed divergence. However, we must note that the latest BoC statement and monetary policy reports make no mentions of FX-related risks for inflation. Incidentally, the USD/CAD rally since mid-July and after the BoC cut has been a mere 1.2% compared to much wider moves in other G10 pairs. Discussions on an excessively weak currency shouldn't arise as long as USD/CAD stays below 1.40 (currently 1.38), if not more – in our view.

Two more cuts, risk of threeDespite a dovish meeting today, markets are pricing in only -15bp for the 4 September meeting, probably since the BoC meeting is two weeks before the Fed one. The pricing for year-end has been hovering around -45bp after the cut.

Our latest BoC call was in line with market expectations, as we saw a pause in September followed by back-to-back 25bp reductions in October and December. However, today's relaxed comments by Macklem on Fed decoupling mean higher chances of a September cut. Much will depend on whether inflation continues to edge lower in Canada and probably even more if the jobs market and broader economy show further signs of deterioration. After all, it appears that Macklem has pivoted to a less inflation-focused to a more growth-focused approach today.

Obviously, Fed pricing will have some effect: if markets price out a September Fed cut, they may also partly price out a September BoC cut. In our base case, however, the Fed will cut in September, and if domestic conditions allow the BoC may well reduce rates two weeks before the Fed then. At that point, risks would be skewed for two more BoC cuts by year-end (so 125bp in total for 2024).

CAD: Still protectedThe Canadian dollar hasn't really taken a hit from the BoC cut, which was fully priced in. The loonie has recently been significantly more protected than the likes of AUD, NZD, NOK and SEK (more on those last two here ). That will probably continue in the near term as the risks associated with a new Trump term hit the loonie exponentially less than other high-beta G10 currencies, and the better liquidity of CAD shields it more against risk-off moves.

That said, the widening USD-CAD rate differential means that there will be pressure on USD/CAD to keep appreciating. A break above 1.380 is very much possible and the move can extend to 1.390 should markets price in a September BoC cut. Beyond the near term, USD/CAD is still probably due a correction once the Fed easing come through. A return below 1.350 remains our medium-term call.

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

- Manuka Honey Market Report 2024, Industry Growth, Size, Share, Top Compan...

- Modular Kitchen Market 2024, Industry Growth, Share, Size, Key Players An...

- Acrylamide Production Cost Analysis Report: A Comprehensive Assessment Of...

- Fish Sauce Market 2024, Industry Trends, Growth, Demand And Analysis Repo...

- Australia Foreign Exchange Market Size, Growth, Industry Demand And Forec...

- Cold Pressed Oil Market Trends 2024, Leading Companies Share, Size And Fo...

- Pasta Sauce Market 2024, Industry Growth, Share, Size, Key Players Analys...

Comments

No comment