(MENAFN- ING) construction outperformed expectations in 2023

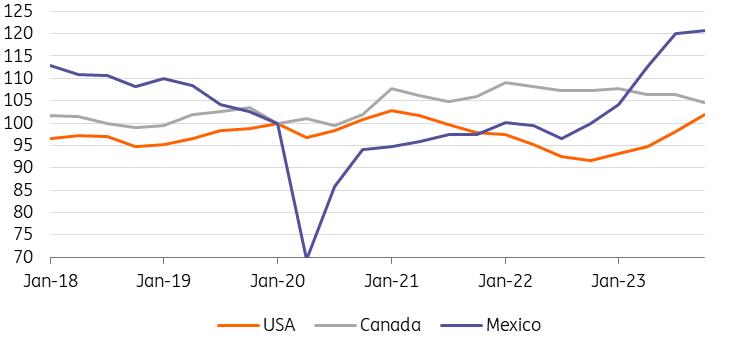

Given the backdrop of high interest rates, tight credit availability and worries about a potential financing crunch in the wake of US banking failures in March of last year, the North American construction sector performed well in 2023. Mexico was top, experiencing rapid growth, led by accelerated public infrastructure spending ahead of this year's Presidential election. In the US, a lack of existing homes for sale meant demand for new homes remained resilient despite high mortgage rates. At the same time, government support to incentivise the reshoring of manufacturing activity has seen construction activity in the non-residential sector perform even more strongly than for home building.

Canada was the underperformer with housing starts falling, led by declines in single-family home construction. Non-residential construction was stronger, led by industrial and institutional investment spending, but commercial construction, such as offices and retail which make up half of non-residential construction, was lower and is currently down around 3.5%YoY.

Construction value added

Constant prices 4Q19=100

Source: Macrobond, ING 2024 constrained by reduced government support and high borrowing costs

2024 is also expected to see a mixed performance. In the case of Mexico, inflation is slowing and the central bank cut interest rates for the first time in this cycle in March. Markets expect the policy rate to be lowered to 9.5% by year-end, having peaked at 11.25% in 2023. Lower borrowing costs should allow the economy to continue growing close to trend, with unemployment remaining around 3%. This backdrop should support both private residential and non-residential construction. However, public construction should contract sharply after the rapid growth seen in 2023.

In the US, interest rates remain elevated with 30Y fixed-rate mortgages back above 7%, but they are expected to fall in 2H 2024 as the Federal Reserve becomes more comfortable with the inflation backdrop and cooling of the jobs market triggers looser monetary policy towards the end of the year. Government support programmes for manufacturing-related construction activity will continue throughout the year, but the incremental increase in spending will slow markedly. Uncertainty over the impending presidential election and potential policy shifts may also see more reluctance to put money to work, but overall we should still see positive growth.

Canada looks more difficult to call with elevated house price-to-income ratios and the structure of the Canadian mortgage market acting as a headwind for construction. Subdued economic growth relative to the US and Mexico and the general uptrend in the unemployment rate over the past 12 months may mean we see a slowing in growth in the non-residential construction sector. Longer term, the outlook is more positive, given immigration has boosted population growth.

US residential construction supported by a lack of existing homes for sale

In the case of the US, the fact that home prices have risen 46% nationally since December 2019 combined with mortgage rates more than doubling to 7% has severely compromised affordability. In January 2021, a $350,000 mortgage charging 2.9% interest would result in a monthly repayment of just over $1,450. At today's mortgage rate of 7%, if you could only afford that $1,450 monthly payment, you would be limited to borrowing $220,000.

Ordinarily, this should mean bad news for homebuilders, but with existing homes in extremely limited supply, those who need to move and want to buy have to increasingly opt for a newly built home. After all, with so many homeowners locked into 30Y mortgages between 3 and 4%, it makes little sense to move home and have to transfer to a 7%+ mortgage rate, and there is certainly little incentive to sell and rent. As a result, new home sales now account for 16% of all housing transactions, up from 12% before the pandemic. While this implies relative resilience, new home sales are running at an annualised rate of around 670,000, which is broadly in line with the average number of homes each year since 1990. This is despite the rapid growth in the US population from 250 million to 340 million over the same period.

New home sales resilient to higher rates thanks to a lack of existing homes for sale

Source: Macrobond, ING According to the S&P Case Shiller price index, house prices did fall outright in early 2023, but we have since seen a recovery and strong pricing is boosting profitability, especially given the cooling in wage pressures and commodity input costs and this is supporting home builder sentiment. That said, we are a little wary given that the price for new homes has fallen from a peak of $496,000 in October 2022 to $400,500 in February 2024, but this metric is vulnerable to changes in the size of homes constructed.

Still, the main point we would make is that we believe the Federal Reserve will be in a position to cut interest rates later this year , and we see scope for more policy easing than the market is currently discounting. Mortgage rates should follow Treasury yields lower in the second half of the year. This should provide a bit more support for demand via improved affordability in an environment where unemployment remains relatively low.

House prices (YoY%)

Source: Macrobond, ING Housing starts averaged 1554k in 2022 but slowed to 1422k in 2023. We look for them to average 1450k in 2024 and 1500k in 2025 before rising to 1600k in 2026, with upside risk given the rapid increases in population growth the US continues to experience.

Canadian homeowners more exposed to higher interest rates, but population growth is stronger

Canadian house prices have been more volatile than those of the US, falling 11% between May 2022 and February 2023. They appear to have stabilised somewhat now, but with affordability even more stretched than in America – the average house price to income ratio is just below nine times income versus a mere 5.3 times income in the US – there is a degree of vulnerability to a larger price correction in the near term.

After all, Canadian borrowers are more exposed to higher borrowing costs over a longer period of time. While the typical mortgage taken out by a US home buyer is a 30Y fixed, in Canada, it is a five-year mortgage, amortised over 25 years. That means borrowers are subject to periodic interest rate resets, so a greater proportion of homeowners have been experiencing the effects of Bank of Canada interest rate increases over time than those in the US. Note, too, that Canadian household debt is equivalent to 180% of disposable income versus 100% in the US. So, more debt exposure with more people facing higher interest rates implies a greater chance that the Canadian household sector faces stress that feeds into weaker housing transactions.

On the positive side of the equation, Canada's population growth has been rapid, rising 4.3% between 2020 and 2024, with total employment up 6.25%, while the US population has increased just 1.4% over the same period, and Mexico's has increased 2.6%. Therefore, demand for residential construction should remain firm with Canadian housing starts expected to hold steady at around 240,000 this year versus 263,000 in 2022 and 245,000 in 2023. Assuming interest rates are cut by the Bank of Canada later in the year we expect this to recover to around 265,000 units in 2025 with a positive outlook for subsequent years.

Typical mortgage rates (%)

Source: Macrobond, ING Mexico residential market less exposed to interest rates

The Mexican residential property market has been more resilient than that of the US and Canada, which likely reflects that most homes are either bought with cash, self-built, or inherited. Just 10% of homes are purchased using a conventional mortgage from a financial institution versus 70% in the US, so interest rate movements tend to have less of a bearing on the supply and demand of homes.

Moreover, nearly two-thirds of residential properties are built using homeowners' own resources, with 25% of homes built in Mexico having been partially funded by INFOAVIT – the federal institute for workers' housing. This means that the state of the jobs market and households' disposable income and savings levels are a more important driver of residential property activity than elsewhere. With unemployment likely to remain in the low 3% region and worker remittances from the US at record highs of around $16bn per quarter, we expect residential construction activity to remain robust this year and into next.

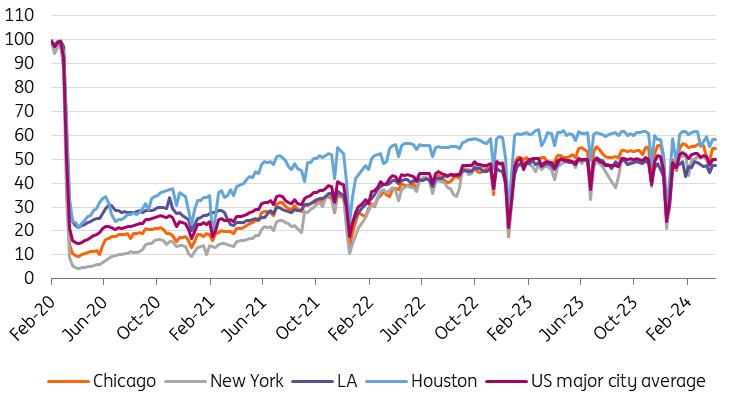

Non-residential construction faces a broader range of uncertainty

Banking stresses in early 2023, coupled with high interest rates, suggested that highly leveraged US sectors, such as construction and real estate, would struggle. That has not been the case. Even the office market, where utilisation rates remain down 50% on pre-pandemic levels, activity has held up well, with spending growth running at 5.7% YoY. Remain wary of this sector, though. We acknowledge that long lead times may be keeping the numbers supported for now, and the prospects look much less rosy for 2025 and 2026.

US office occupancy versus pre-pandemic norms (%)

Kastle systems operating offices

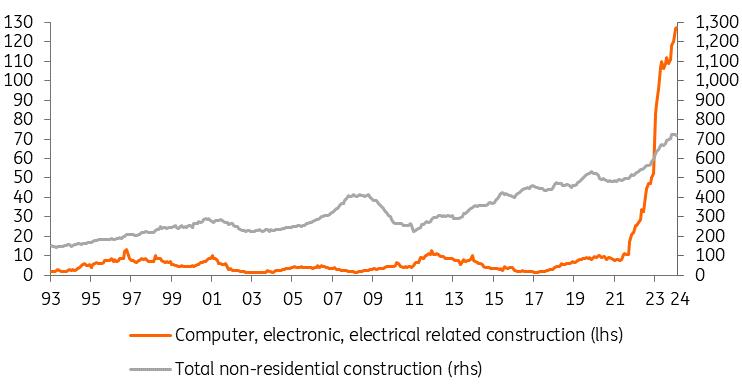

Source: Macrobond, ING The success of the US non-residential construction case could well be, in large part, attributed to the effectiveness of President Joe Biden's incentives to re-shore semiconductor manufacturing through the CHIPS Act of 2022 (Creating Helpful Incentives to Produce Semiconductors). The tax credits prompted a sharp increase in the construction of chip fabrication plants, which has been supplemented by the Innovation and Competition Act that authorised $110bn for technology research.

Government support for the sector is set to remain in place, irrespective of the outcome of the November elections. Democrats and Republicans both want to keep the US leading the world in technological innovation while also protecting national security. The chart below shows that construction spending in this sector has accounted for more than half of the increase in total non-residential construction activity. The pace will inevitably slow through 2025 and 2026.

US non-residential construction spending ($bn)

Source: Macrobond, ING President Biden's programmes to offer diminishing support

Additionally, the Infrastructure Investment and Jobs Act (IIJA) of 2021 was aimed at expanding the construction of public roads, EV infrastructure, broadband, water, and so on. However, actual spending has been increasing at a more moderate rate than that under the CHIPS Act. Nevertheless, the IIJA is expected to spur more construction activities through 2026.

However, both the IRA and the clean energy part of the IIJA risk policy disruption after the November elections. The two acts may not completely disappear even under a Republican administration because of the potential economic benefit and job creation. But their financial incentives can be scaled back, and implementation rules can get stricter. This means that the positive effect these acts would bring to the construction sector may become relatively lower in 2026 and beyond. Even if President Biden wins re-election, additional support over and above what has already been announced is likely to be limited by significant government debt levels and high borrowing costs, pressuring authorities to look at ways of saving money.

Another issue for the construction industry to potentially contend with is the threat of a re-escalation of tariffs. President Trump initiated tariffs on steel and aluminium imports in 2018 under Section 232 of the Trade Expansion Act of 1962. This law allowed the president to raise tariffs on imports that pose a threat to national security without having to win the approval of Congress. As the presumptive Republican Party candidate, Donald Trump has proposed a 10% tariff on all US imports, with 60% tariffs on Chinese imports, as part of his election campaign. The risk of reciprocal tariffs could see construction resource costs rise. Offsetting this to some extent is evidence of a cooling jobs market, with lead indicators pointing to slowing wage growth and greater availability of workers for hire.

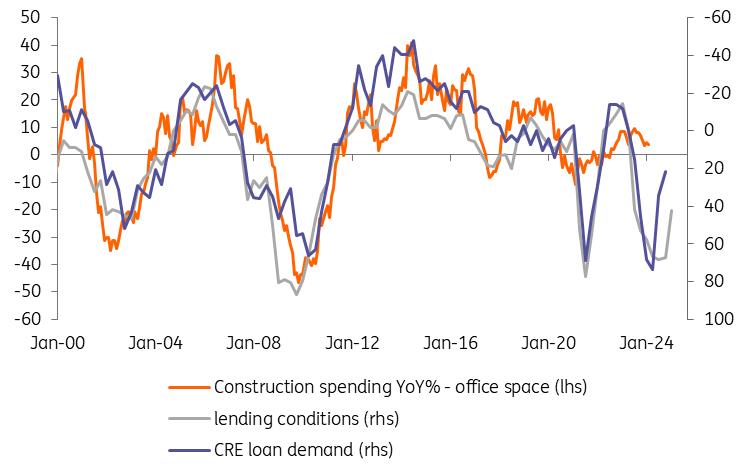

Putting it all together, we do see the risk of slower non-residential construction in 2024 and 2025. Waning fiscal support, the prospect of weaker new office construction demand, tight credit conditions, and high borrowing costs for what is typically a highly leveraged sector are reasons why we're likely to see the sector struggle to meet 2023's performance. On balance, we see the sector growing by 1% in 2024, with the prospect of a 2% decline in 2025.

Office construction fundamentals look weak

Source: Macrobond, ING Mexico construction sector to contract

Mexico's upcoming election on 2 June will potentially have an influence on the outlook for the construction sector there. The Mexican Constitution prohibits incumbent president Andrés Manuel López Obrador from seeking re-election after serving his six-year term, so this will be the first election in Mexico's history where the two leading candidates are female - Claudia Sheinbaum from the ruling collation, Sigamos Haciendo Historia – and Xóchitl Gálvez from Fuerza y Corazón por México.

That hasn't stopped the President from ramping up government spending on construction projects over the past year, leaving Mexico's budget deficit as a percentage of GDP at 5% - the highest in 40 years. The suggestion is that he wanted the landmark government projects completed as quickly as possible in order to claim responsibility for their success. The risk being that delay means his successor will gain the credit once they open.

So far, there is little information on what either candidate may mean for the construction sector specifically, but given its importance for jobs, we expect it to remain a priority. Nearly 5 million people are employed in the sector, out of Mexico's total employment of 60 million.

While Mexico's construction sector is set to remain supported to some extent by long lead times on government infrastructure projects, activity will inevitably contract markedly on last year's breakneck pace. Moreover, the election timing limits the scope for the announcements of new activities this year, which will be a headwind for late 2025 into early 2026, while high government borrowing could also mean less scope for additional projects further down the line.

Nonetheless, near-shoring exploits of US companies should also continue to bolster prospects for the sector irrespective of who wins the US presidency given President Trump was the one who signed the USMCA trade deal into law. Mexico is already in the process of lowering borrowing costs, and given low unemployment and a relatively firm economic outlook, we expect to see a contraction in 2024 before a return to modest positive growth in 2026.

We see similar constraints for Canada as we do the US, but without the tax incentives support provided to the private sector by the US government. Consequently, the risk is for continued Canadian underperformance in 2024 and 2025. There are certainly still government infrastructure plans surrounding broadband and energy infrastructure plus public transport link upgrades, but elevated government borrowing and high borrowing costs are acting as a constraint in the near term.

Longer term, the fast population growth bodes well for strong construction activity with both public sector infrastructure and private activity set to benefit, but this is more likely to be a story for 2025 and beyond. The next Canadian Federal election isn't scheduled to be held until October 2025, so the political backdrop should provide less uncertainty than in the US or Mexico.

Conclusions: More headwinds with US likely to outperform

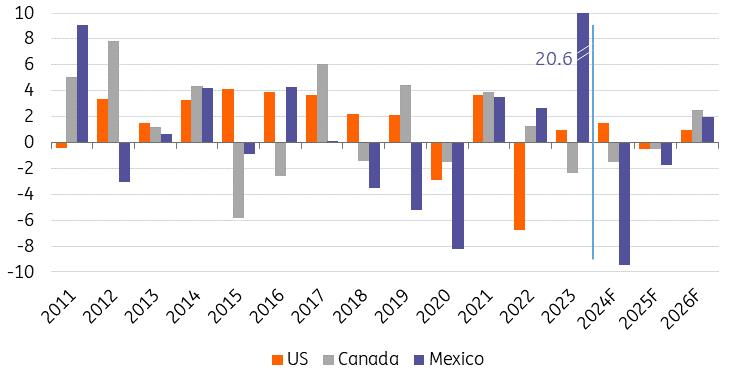

After surprising strength in the US, surging growth in Mexico, and weakness in Canada in 2023, we are likely to see another mixed performance this year. While fundamentally the situation in Mexico remains robust, it won't be enough to offset a marked downturn in public infrastructure spending. We look for Mexican construction value added to slump 9% after the 20% jump in 2023, with growth resuming in 2026.

The US story is likely to be supported in the near term by the legacy of government support to incentivise reshoring activity and a lack of existing homes for sale, boosting new home construction, but interest rate uncertainty and worries about the US office market linger. We expect value added to increase by 1.5% this year but see the potential for a modest contraction in 2025 before lower interest rates provide more support for activity in 2026.

Canada's construction sector is likely to continue struggling given the affordability challenges in the residential market and high borrowing costs cool private sector demand. Longer-term, demographics and the prospect of eventual interest rate cuts look favourable for a stronger performance for Canada's construction sector from late 2025 onwards.

Construction value added full year forecasts (YoY%)

Source: Macrobond, ING Hard landing versus soft landing would have greater ramifications

Our projections assume a relatively benign macro backdrop of a cooling economy, moderating inflation, and gradual interest rate cuts, which would take monetary policy to a more neutral footing. By mid-2025, the Fed funds target rate would be around 3.25%- 3.5%, Bank of Canada rates would be down to 3.5%, and Mexico policy rates would be down to around 8%.

A“hard landing” for the economy cannot be ruled out. One way this could happen is if the central banks, spooked by higher inflation prints and firm jobs numbers, err on the side of caution and keep interest rates higher for longer. US 10Y Treasury yields are already edging back towards 5%, pushing up borrowing costs for households and businesses. Those homebuyers that over-extended themselves, borrowing as much as they could assuming mortgage rates would fall and they could refinance, would face increasing stress while office commercial real estate refinancings would be more challenging, and we could see loan losses mount for the banking sector.

It would be a similar story in Canada, with more and more borrowers facing higher mortgage rates as their fixed rate term ends and their borrowing rate resets at a higher rate. CRE loan losses for banks would also likely rise. Mexico would be more insulated on the residential front, given the relatively low usage of mortgages.

Higher interest rates would likely dampen activity more broadly and heighten the chances that businesses become more cautious about the prospects for the economy and that unemployment starts to creep higher. This, in turn, reduces demand for property purchases and further diminishes the demand for office space. Indeed, in the US, we are already seeing loan defaults rise – credit card delinquencies have risen from 4% to 8.5% and could potentially rise to GFC levels of 12%, while car loan delinquencies are also picking up. If commercial Real Estate (CRE) loan losses mount, this could reignite concerns about small bank solvency in the US economy. Credit conditions would tighten significantly and, coupled with high borrowing costs and asset price declines, potentially resulting in the US economy falling into a recession.

This scenario would undoubtedly be very bad news for the North American construction sector. By way of reference – and very much a worst case scenario – construction sector output output fell by around a third in the US, 10% in Canada and 15% in Mexico in the wake of the Global Financial Crisis.

MENAFN23042024000222011065ID1108129284

Author:

James Knightley, Coco Zhang