403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Australian Employment Surges In February

| 116.5 | Monthly employment change

000s |

| Higher than expected |

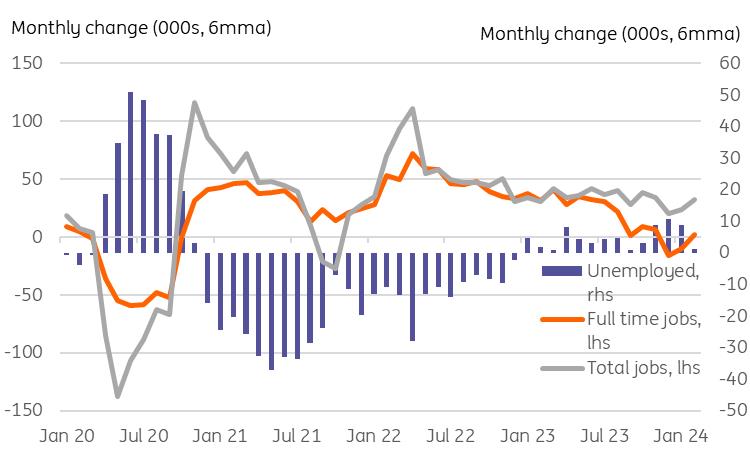

Australia's headline employment increase for February smashed through expectations, rising by 116.5 thousand from January. There were also some slight upward revisions to the January numbers, so these February figures are even better than they appear at first glance.

Not only is the scale of the increase impressive, but the majority of the increase is attributable to the 78,200 increase in full-time jobs. Part-time jobs also rose strongly but by a relatively more modest 38,300. This split is important as full-time jobs will typically be more secure, better paid, carry better perks and encourage greater household spending than part-time jobs.

There was also a big drop in the unemployment rate to 3.7% from 4.1%. This isn't all that far above the all-time low of 3.5%.

Australian employment and unemployment rate (6mma)

The RBA is keeping its options open

Employment data is always very volatile, and no single month of data should be read in isolation. However, today's figures are too strong to ignore, and even the heavily-smoothed chart above shows that total and full-time employment are trending higher again, while unemployment is trending lower.

The Reserve Bank of Australia (RBA) decided to amend its policy guidance at their meeting earlier this week, when they removed the reference to "...further tightening" and switched it to a neutral-sounding "...all rate options are open".

In light of this data, they are probably quietly relieved that they did not go further and adopt an outright easing bias this week.

Inflation, rather than labour data, will be the main determinant of RBA policy. But the two are linked, and further declines in inflation would look more probable if the labour market were weakening, not firming as today's data suggest.

We aren't forecasting any further rate hikes from the RBA, but we share their view that all rate options remain open. And while policy easing later this year remains our base assumption, we are a little less relaxed about that call than the market, and can't rule out the tail risk of a further "insurance hike" in the first half of this year.

Author:Robert Carnell

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment