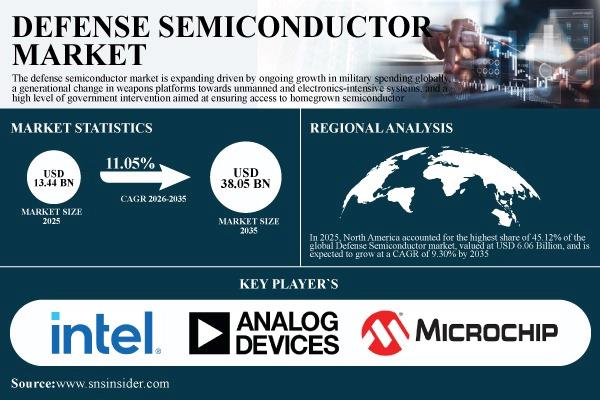

(MENAFN- GlobeNewsWire - Nasdaq) U.S. Market Expected to Reach USD 11.92 Billion by 2035; Europe Defense Semiconductor Market Projected to Hit USD 7.18 Billion Amid Defense Technology Investments.Austin, United States, June 05, 2026 (GLOBE NEWSWIRE) -- “The Defense Semiconductor Market size was valued at USD 13.44 Billion in 2025 and is projected to reach USD 38.05 Billion by 2035, expanding at a CAGR of 11.05% during 2026–2035, according to SNS Insider.”

The Defense semiconductor market is growing due to the continued growth in military spending around the world, a generational shift in weapons platforms towards unmanned and electronics-heavy systems and an elevated level of government intervention to ensure access to homegrown semiconductor supply chains for critical defense applications.

Get a Sample Report of Defense Semiconductor Market Forecast @

Rising Defense Semiconductor Demand to Boost Market Growth Globally

The global defense semiconductor market growth is still being led mainly by the concurrent ramp-up of military modernization programs by both NATO and Indo-Pacific nations in response to an increasingly deteriorating security environment since 2022. Current programs are inherently biased towards electronics-based systems such as next generation AESA radar systems, networked air defense systems, electronic warfare systems and precision guided munitions with multi-mode seekers. All these programs fundamentally depend on the performance of semiconductors.

Leading Market Players Listed in the Global Defense Semiconductor Market Report are:

Intel Corporation Texas Instruments Analog Devices AMD (Xilinx) Microchip Technology Infineon Technologies NXP Semiconductors STMicroelectronics Qualcomm Broadcom Renesas Electronics Maxim Integrated ON Semiconductor Lattice Semiconductor Vishay Intertechnology Raytheon Technologies Lockheed Martin BAE Systems Northrop Grumman Boeing

Defense Semiconductor Market Segmentation Analysis:

By Component Type

Power Semiconductors dominated with 30.68% in 2025 due to the central role of wide-bandgap GaN and SiC devices in radar transmitters globally. Power Semiconductors is also expected to grow at the fastest CAGR of 12.80% from 2026 to 2035 driven by accelerating adoption of all-electric propulsion architectures in naval vessels and armored ground vehicles.

By Application

Radar & Surveillance Systems dominated with 27.34% in 2025 as active electronically scanned array technology became the de facto standard across new-generation fighters, destroyers, and ground-based air defense batteries. Electronic Warfare is expected to grow at the fastest CAGR of 13.10% from 2026 to 2035 due to the increasing demand for adaptive, wideband RF signal processing semiconductors.

By Platform / End-Use

Aerospace (Aircraft, UAVs, Satellites) dominated with 32.45% in 2025 due to the intensive semiconductor content of modern combat aircraft avionics globally. Cybersecurity & Intelligence is expected to grow at the fastest CAGR of 12.40% from 2026 to 2035 owing to the growing military UAV fleet from strategic HALE platforms to tactical loitering munitions.

By Type / Technology

Digital Semiconductors dominated with 29.63% in 2025 driven by the growing digitization of formerly analog radar and communications globally. RF & Power Semiconductors is expected to grow at the fastest CAGR of 12.22% from 2026 to 2035 due to the adoption of FPGAs and DSPs as the standard architecture for mission computers globally.

Regional Insights:

North America held the largest share of 45.12% of the global Defense Semiconductor market, valued at USD 6.06 Billion in 2025, and is expected to grow at a CAGR of 9.30% by 2035. The growth is driven by the scale of procurement machinery at the U.S. Department of Defense, the clustering of the world's most sophisticated defense electronics primes, and the maturity of the domestic trusted foundry ecosystem enabled by the Defense Microelectronics Activity's Trusted Foundry Program.

The U.S. Defense Semiconductor Market was valued at 5.04 Billion in 2025 and is projected to reach 11.92 Billion by 2035, growing at a CAGR of 9.05% from 2026 to 2035. The U.S. market accounts for 83.14% of North America, propelled by the Trusted Foundry ecosystem of Defense Microelectronics Activity, DoD R&D investment through DARPA and Microelectronics Commons, and close ties between government laboratories and the commercial semiconductor industry.

The Europe Defense Semiconductor Market is estimated to be USD 2.75 Billion in 2025 and is projected to reach USD 7.18 Billion by 2035, growing at a CAGR of 10.07% during 2026–2035. The region's market is structurally driven by Eurofighter Typhoon avionics upgrade cycles, the KNDS MGCS next generation tank program, MBDA missile family electronics refreshes and accelerated procurement of ground-based air defense systems by the Nordic and Baltic states.

The Asia Pacific region is expected to record the highest CAGR of 13.72% in the global Defense Semiconductor market during the forecast period of 2026-2035, with the region valued at USD 3.34 Billion in 2025. The move to doubling defense spending as a share of GDP in Japan, as realized in the 2024-2025 budgets, was directly linked to the swift procurement of AESA radars, EW systems and precision-guided munitions for the nation's air and maritime self-defense forces.

Do you have any specific queries or need any customized research on Defense Semiconductor Market? Schedule a Call with Our Analyst Team @

Recent Developments:

2024-2025, Analog Devices secured design wins for its next-generation wideband radar transceiver ICs in U.S. and allied ground-based air defense upgrade programs, with production ramp anticipated through 2026-2027. In 2024, Texas Instruments expanded its HIREL product line with additional MIL-PRF-38535 Class V qualified devices targeting space and high-reliability airborne applications, specifically the next-generation satellite communications and GPS receiver market segments where the restricted field of qualified suppliers commands premium pricing.

Exclusive Sections of the Report (The USPs):

MISSION-CRITICAL PERFORMANCE METRICS – helps you evaluate semiconductor performance across processing speed, signal integrity, power efficiency, and reliability in defense-grade operating environments. DEFENSE PLATFORM DEPLOYMENT ANALYSIS – helps you understand semiconductor utilization across radar, surveillance, communications, electronic warfare, avionics, and missile guidance systems. RUGGEDIZATION & ENVIRONMENTAL RESILIENCE METRICS – helps you assess radiation resistance, thermal stability, durability, and high-frequency performance in extreme military and space-grade conditions. DEFENSE MODERNIZATION & TECHNOLOGY ADOPTION RATE – helps you identify adoption trends of advanced analog, digital, mixed-signal, RF, power, and radiation-hardened semiconductor technologies. SYSTEM INTEGRATION & OPERATIONAL EFFECTIVENESS ANALYSIS – helps you measure improvements in interoperability, mission success rates, targeting accuracy, communication reliability, and defense system efficiency. COMPETITIVE LANDSCAPE & DEFENSE SUPPLY CHAIN ANALYSIS – helps you gauge the competitive positioning of key semiconductor suppliers based on technology capabilities, defense contracts, product portfolios, innovation activities, and recent developments.

Defense Semiconductor Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 13.44 Billion |

| Market Size by 2035 | USD 41.62 Billion |

| CAGR | CAGR of 11.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Key Segments | . By Component Type (Microprocessors & Microcontrollers, Memory Devices, Analog & Mixed-Signal ICs, RF & Microwave Components, and Power Semiconductors)

. By Application (Radar & Surveillance Systems, Communication Systems, Electronic Warfare, Navigation & Avionics, and Missile Guidance & Control)

. By Platform / End-Use (Aerospace (Aircraft, UAVs, Satellites), Land Systems (Armored Vehicles, Ground Defense), Naval Systems, and Cybersecurity & Intelligence)

. By Type / Technology (Analog Semiconductors, Digital Semiconductors, Mixed-Signal Semiconductors, RF & Power Semiconductors, and Radiation-Hardened Semiconductors) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

CONTACT: Contact Us:

Rohan Jadhav - Principal Consultant

Phone: +1-315-961-9094 (US)

Email:...

Comments

No comment