403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Aerospace Engineering Services Outsourcing Market Size, Share, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

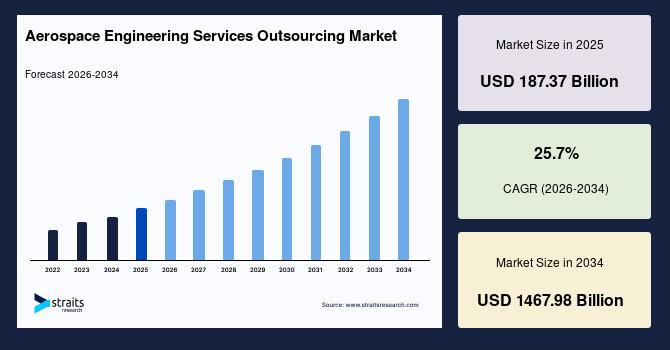

| 2025 Market Valuation | USD 187.37 Billion |

| Estimated 2026 Value | USD 235.52 Billion |

| Projected 2034 Value | USD 1467.98 Billion |

| CAGR (2026-2034) | 25.7% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Europe |

| Key Market Players | AKKA, ALTEN Group, Honeywell International, ALTRAN, Bertrandt |

Download Free Sample Report to Get Detailed Insights.

Aerospace Engineering Services Outsourcing Market Dynamics Market DriversRising Demand for Next-generation Aircraft Development and Growing Demand For Faster & Cost-efficient Aircraft Development Cycles Drives Market

Strong demand for fuel-efficient aircraft, electric propulsion systems, and advanced avionics is driving aerospace OEMs to increasingly outsource engineering services. These complex programs require specialized expertise in design, simulation, and systems integration that is often unavailable in-house at scale. As a result, demand for outsourced engineering support is rising across both commercial and defense aviation programs. This is significantly expanding opportunities for ESO providers with advanced technical capabilities.

Aerospace manufacturers are under growing demand pressure to reduce development timelines and overall R&D expenditure while maintaining high safety and performance standards. This is increasing reliance on outsourcing partners for rapid prototyping, digital simulation, and iterative engineering support. Outsourced ESO providers help accelerate design-to-certification cycles and improve project efficiency. This is steadily driving higher demand for scalable and specialized engineering service providers globally.

Market Restraints Long Project Development Cycles and Strict Regulatory & Certification Requirements Restrain Aerospace Engineering Services Outsourcing Market

Aerospace engineering services outsourcing is constrained by extremely long aircraft development and certification timelines, often spanning several years or even decades. This delays revenue realization for service providers and reduces short-term scalability of outsourced projects. It also increases dependency on long-term contracts with OEMs, making cash flow cycles slower and less flexible.

The aerospace engineering services outsourcing market is heavily restrained by stringent aviation safety regulations and certification standards imposed by authorities such as FAA and EASA. Every outsourced engineering output must undergo multiple validation, testing, and approval stages before implementation. This increases project complexity, extends delivery timelines, and limits the speed of outsourcing adoption across critical aerospace programs.

Market Opportunities Expansion of Space Exploration Programs and Growth of Defense Modernization Programs Opens New Growth Avenues for Market Players

The rapid expansion of space exploration programs, including satellite deployments, lunar missions, and commercial space travel, is creating strong demand for outsourced aerospace engineering services. These programs require advanced capabilities in spacecraft design, propulsion systems, and mission simulation, driving reliance on specialized ESO providers. This opportunity is primarily for aerospace engineering service firms, satellite manufacturers, and space-tech companies supporting mission-critical engineering work.

The growth of defense modernization programs is driving strong demand for outsourced aerospace engineering services in upgrading fighter jets, UAVs, missile systems, and defense electronics. Governments and defense contractors are increasingly relying on ESO providers for advanced design, systems integration, and simulation support. This opportunity is mainly for defense OEMs, aerospace engineering service providers, and technology contractors involved in military aviation programs. Companies such as Boeing supports defense-related engineering and modernization programs through advanced aerospace design and systems development capabilities.

Market Challenges Geopolitical & Defense Restrictions and High Dependency on OEM Approvals Challenges Aerospace Engineering Services Outsourcing Market Growth

Geopolitical tensions and defense-related regulations significantly restrict cross-border outsourcing in the aerospace engineering services market. Sensitive defense programs often require work to be executed within specific countries or approved jurisdictions, limiting global collaboration. This reduces the addressable market for ESO providers and slows international expansion.

Aerospace engineering service providers face strong dependency on OEM approvals at every stage of design, testing, and validation. Any delay in feedback or authorization from OEMs can slow project execution and extend delivery timelines. This creates operational bottlenecks and limits flexibility for outsourcing partners in managing workflows efficiently.

Regional Analysis North America Aerospace Engineering Services Outsourcing MarketNorth America is the most significant shareholder in the global aerospace engineering services outsourcing market and is anticipated to grow at a CAGR of 24.5% during the forecast period. The region is expected to dominate the industry, owing to the proliferation of new technologies at a higher rate and the vital presence of aerospace OEMs. The U.S. accounted for the most significant market share of the software segment in the component category due to continuous innovations in the IT sector and increasing deployment of IT services, data center systems, enterprise software, and communication systems in the region. In addition, the aggressive race in the aerospace ESO market of the U.S. and Canada will combine to generate a consistent revenue trend throughout the forecast period. Honeywell International Inc. and Altair Engineering, Inc. are the most dominant regional players accounting for most of the region's revenue share.

Europe is estimated to grow at a CAGR of 25.3% over the forecast period. Demand for aerospace ESO in European countries is anticipated to be sluggish because of market saturation, ferocious competition, and challenging economic conditions. Market saturation, intense competition, and challenging economic circumstances are to blame for this poor growth rate. In addition, Germany is anticipated to see significant growth within Europe during the projection period. In Europe, imminent markets for aerospace ESO such as Spain and Italy, are expected to grow considerably during the forecast period.

The Asia-Pacific region is expected to witness a significant CAGR during the projection period due to the increasing number of collaborations between aerospace OEMs and service providers, which are predicted to increase significantly due to the availability of a low-cost, highly skilled workforce. Within Asia-Pacific, China showcases the most significant market share. In contrast, India, followed by Japan, is anticipated to witness higher CAGR over the forecast period, despite the ongoing pricing pressures, due to heightened competitive intensity.

LAMEA is expected to grow steadily over the forecast period. The active competition presently seen in the Middle East and Africa and Latin America regions are expected to be the growth factor for the aerospace ESO sector. The areas are anticipated to outperform over the forecast period compared to other matured markets.

Segmental AnalysisThe global aerospace engineering services outsourcing market is segmented by service, function, location, and component.

Based on service, the global aerospace engineering services outsourcing market is segmented into mechanical engineering, electric/ electronic engineering, embedded software engineering, and others.

The mechanical engineering segment owns the highest market share and is expected to grow at a CAGR of 24.7% over the forecast period. The mechanical engineering sector accounted for the most significant revenue share of the market, and it is anticipated that it would sustain its dominance over the forecast period. This is attributable to the significant demand for structural, system, and fluids and thermal engineering in the aerospace sector.

Based on function, the global aerospace engineering services outsourcing market is divided into design, simulation and digital validation, production process, and maintenance process.

The maintenance process segment is responsible for the substantial market share and is expected to grow at a CAGR of 24.6% over the forecast period. The maintenance process segment includes the after-market functionalities and security and certification functions in the aerospace industry. The segment is gaining prominence due to increasing awareness about safety and airworthiness. Regulatory bodies and governments across the globe are continually focusing on environmental welfare and imposing stringent norms on the aerospace industry to safeguard the same.

Digitization and many connected devices have augmented the need for information assurance and cyber resilience. This has made it mandatory for the aerospace industry to ensure data security against cyber threats. Functions such as product support, predictive maintenance, and asset tracking and management have seen a surge in the aerospace sector. The increasing outsourcing of Maintenance, Repair, and Overhaul (MRO) processes will likely encourage the maintenance process segment to retain its dominance over the forecast period.

Based on location, the global aerospace engineering services outsourcing market is bifurcated into onshore and offshore outsourcing activities.

The onshore segment owns the highest market share and is anticipated to grow at a CAGR of 26.0% during the forecast period. The onshore outsourcing activity in the aerospace industry is developing rapidly owing to the security and authenticity promised. The onshore activity enables aerospace OEMs to partner with the ESP in their time zone and work in the same lawful jurisdiction. This allows easy and better-streamlined communication between the two firms, increasing the efficiency of outsourced services. In addition, the aerospace and defense sector is witnessing a Manufacturing-as-a-Service (MaaS) trend to diversify their supply chains. Onshoring MaaS can reduce delay possibilities and shipping outlays and ensure more competent designs. There has been an increase in onshoring of aerospace engineering services, especially in the Middle East and Africa region, to meet the growing demand for a reduction in transportation delays and costs.

Based on components, the global aerospace engineering services outsourcing market is divided into hardware and software.

The hardware segment is the highest contributor to the market and is projected to grow at a CAGR of 25.5% over the forecast period. The hardware segment comprising raw materials, forgings, castings, extrusions, parts, components, subassemblies, aero-structure, aero-engine, avionics, aircraft interiors, and all hardware modules required to build the aircraft and spacecraft, possesses the greatest market share and is anticipated to rule the market during the forecast period. The hardware component segment will likely hold the leading position over the forecast period owing to the rapid growth in electro-mechanical systems used in the aerospace industry.

Competitive LandscapeThe aerospace engineering services outsourcing (ESO) market landscape is moderately consolidated at the top but broadly fragmented overall, with global engineering service providers, specialized aerospace consultancies, and large IT/ER&D firms actively competing across design, simulation, testing, and lifecycle support services. Established players such as Alten Group, Capgemini Engineering, HCLTech, and L&T Technology Services compete primarily on deep aerospace domain expertise, certified engineering capabilities, long-term OEM partnerships, global delivery centers, and strong compliance with aviation safety and regulatory standards. emerging players focus on cost competitiveness, niche capabilities in areas like digital engineering or software-heavy avionics, faster scalability, and flexible offshore delivery models to win short-cycle or subcontracted engineering work.

List of Key and Emerging Players in Aerospace Engineering Services Outsourcing Market-

AKKA

ALTEN Group

Honeywell International

ALTRAN

Bertrandt

EWI

ITK Engineering GmbH

L&T Technology Services

LISI Group

December 2025: Airbus expanded its outsourcing ecosystem by awarding multi-year engineering and production contracts to Senior PLC, covering aircraft structural components for Airbus commercial programs.

December 2025: Embraer signed cooperation agreements with five companies under Poland's PGZ, covering aircraft engineering support, component manufacturing, MRO (maintenance, repair, overhaul) engineering services, and testing, certification, and industrialisation of aerospace systems.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 187.37 Billion |

| Market Size in 2026 | USD 235.52 Billion |

| Market Size in 2034 | USD 1467.98 Billion |

| CAGR | 25.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Service, By Function, By Location, By Component |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Aerospace Engineering Services Outsourcing Market Segments By Service-

Mechanical Engineering

Electric/ Electronic Engineering

Embedded Software Engineering

Others

-

Design

Simulation and Digital Validation

Production Process

Maintenance Process

-

Onshore

Offshore

-

Hardware

Software

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment