403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Alpha Emitter Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

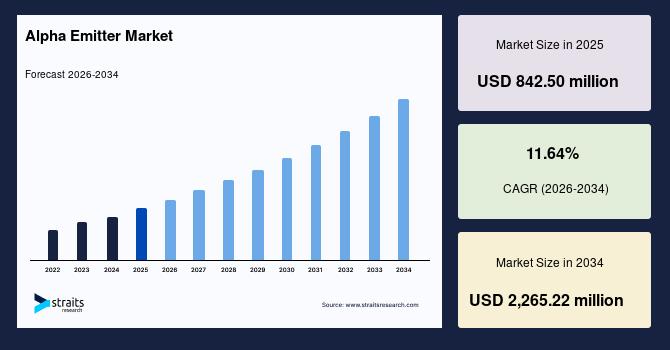

| 2025 Market Valuation | USD 842.50 million |

| Estimated 2026 Value | USD 939.06 million |

| Projected 2034 Value | USD 2,265.22 million |

| CAGR (2026-2034) | 11.64% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Bayer AG, Novartis AG, Actinium Pharmaceuticals Inc., Alpha Fusion, Fusion Pharmaceuticals Inc. |

to learn more about this report Download Free Sample Report

What are the Latest Trends in Alpha Emitter Market?Commercial adoption of accelerator and cyclotron technologies is decentralizing alpha isotope manufacturing, reducing dependence on reactor networks. This trend strengthens supply resilience, enables scalable regional output of Actinium225 and Astatine211, and reshapes upstream production economics for radiopharmaceutical developers.

Alpha emitters are combined with diagnostic imaging agents to create advanced theranostic solutions. This approach enables personalized treatment by improving patient selection, providing real-time therapy monitoring, and enhancing clinical decision-making, thereby driving wider adoption in cancer diagnostics.

Miniaturized onsite generator systems for isotopes like lead212 and astatine211 are emerging, which allow hospitals to produce shortlived alpha emitters locally. This trend reduces decayrelated losses, shortens logistics timelines, and expands treatment access beyond centralized radiopharmacies.

What are the Key Drivers in Alpha Emitter Market?The increasing incidence of metastatic cancers raises the demand for highly targeted treatment approaches capable of destroying malignant cells with minimal damage to surrounding tissues. Alpha emitters deliver high-energy radiation over very short ranges, which improves therapeutic precision and addresses limitations of conventional radiation therapies. As a result, healthcare providers show greater interest in adopting targeted alpha therapies, encouraging pharmaceutical companies and nuclear medicine suppliers to expand production and clinical development.

Continuous improvements in microdosimetry measurement techniques enable more precise evaluation of alpha particle energy deposition at the cellular level. This improves treatment planning accuracy and reduces the risk of unintended toxicity during therapy. Consequently, clinicians gain confidence in using alpha emitters for complex dosing strategies and micro-tumor environments, increasing demand for advanced alpha-based radiopharmaceuticals and supporting market growth.

What are the Restraints in Alpha Emitter Market?The production of key alpha-emitting isotopes such as Actinium-225 remains highly constrained due to scarce feedstocks, complex separation chemistry, and a small number of qualified production facilities. This limited supply creates competition for available material and delays clinical research and therapy deployment, which slows broader adoption of alpha emitter–based treatments.

During alpha decay, recoil energy can dislodge radionuclides from their targeting vectors, causing the isotopes to migrate into surrounding tissues. This instability increases the risk of unintended organ toxicity and requires sophisticated radiochemistry solutions, which complicates formulation and restricts the scalability of alpha-emitter therapies.

What are the Growth Opportunities for Players in Alpha Emitter Market?Increasing collaboration between radiochemistry specialists and biotechnology or pharmaceutical companies accelerates the discovery and development of alpha-conjugated therapies. These partnerships create opportunities to combine expertise in isotope production, molecular targeting, and clinical oncology development. Such collaboration can strengthen innovation pipelines and support the emergence of multi-modal cancer therapies that integrate targeted alpha therapy with other advanced treatment approaches.

Market participants can establish specialized manufacturing facilities designed specifically for alpha-emitter radiopharmaceuticals, including hot cell infrastructure and advanced containment technologies. This creates a growth opportunity to scale production capacity while meeting stringent regulatory and safety requirements associated with handling alpha-emitting isotopes. Companies that expand such infrastructure can support larger clinical pipelines and commercial distribution as targeted alpha therapies move toward broader clinical adoption.

Regional Analysis North America Alpha Emitter MarketNorth America held a dominating share of the market in 2025, with a 44.28% share. The region benefits from a rare concentration of medical-isotope production assets, including US national laboratories such as Oak Ridge National Laboratory that produce actinium-225 for clinical research. This localized supply chain enables isotope availability for pharmaceutical developers and hospitals. The US has numerous oncology research hospitals and nuclear medicine centers conducting targeted alpha therapy trials. This accelerates regulatory submissions of alpha-emitter treatments in this region.

Asia Pacific Alpha Emitter MarketThe Asia Pacific market is anticipated to register a CAGR of 13.06% during the forecast period. As countries in this region, such as China, India, and South Korea, are expanding cyclotron installations and medical isotope reactors to support domestic radiopharmaceutical production. This boosts the regional manufacturing of therapeutic isotopes and reduces import dependency. Multiple Asia-Pacific governments are launching structured national programs to scale nuclear medicine capabilities. For example, India's Department of Atomic Energy and related agencies are investing in isotope production, radiopharmaceutical distribution networks, and specialized treatment centers. These factors collectively drive market growth in this region.

Europe Alpha Emitter MarketThe market in Europe is growing due to the presence of alpha isotopes in Belgium, France, and the Netherlands, which support the regional supply of medical radioisotopes. Facilities such as France's lead-212 production plants and continental radiopharmaceutical manufacturing networks strengthen the supply chain and ensure consistent availability of alpha-emitting isotopes. Advanced nuclear regulatory harmonization under the Euratom framework and strong integration of radiopharmaceuticals within academic medicine programs collectively support market growth.

Middle East & Africa Alpha Emitter MarketThe Middle East & Africa market is gradually expanding as Saudi Arabia and the UAE are integrating nuclear medicine capabilities within large healthcare transformation initiatives. Programs like Saudi Arabia's Vision 2030 include plans to establish multiple nuclear medicine centers, creating infrastructure capable of supporting radiopharmaceutical therapies. Middle Eastern governments are strengthening national cancer registries and early detection programs, particularly for breast, prostate, and ovarian cancers, which, in turn, drive demand for alpha emitters.

Latin America Alpha Emitter MarketLatin America is witnessing steady market growth as the region is experiencing a rising incidence of ovarian cancers due to an aging population and improved cancer detection programs, which increases demand for alpha-emitter radiopharmaceuticals. Brazil has developed a strong domestic nuclear medicine ecosystem through institutions such as the Nuclear Energy Research Institute (IPEN), which produces medical radioisotopes for diagnostic and therapeutic use. This supports regional radiopharmaceutical availability in Brazil and other Latin American countries.

Type of Radionuclide InsightsRadium-223 dominated the type of radionuclide segment with a 39.24% share due to its chemical similarity to calcium, enabling preferential uptake in osteoblastic bone lesions at metastatic sites, allowing ultra-specific delivery of high-LET alpha radiation directly to metastatic bone microenvironments. Long-term safety data increase therapeutic adoption compared with investigational isotopes.

The Actinium-225 segment is expected to grow at a CAGR of 12.35% during the forecast period, driven by innovations in cyclotron-based manufacturing that deliver high-yield, high-purity Actinium-225 at lower cost and scalable volumes compared to Th-229 generator routes, enabling commercial supply of Actinium-225. Emerging micro-reactor and lab-scale production units for Actinium225 allow hospitals or regional production centers to generate isotopes on demand and support segment growth.

Application InsightsProstate cancer dominated the application segment with a revenue share of 56.39% in 2025. Prostate cancer has one of the highest incidences among men globally, with a significant proportion progressing to mCRPC. This patient pool creates a consistent demand for alpha-emitter therapies. Prostate-specific membrane antigen (PSMA) imaging enables precise patient selection for alpha-emitter therapy, which further supports market growth.

The ovarian cancer segment is expected to register a CAGR of 12.64% during the forecast period. This growth is supported by emerging PET/SPECT tracers that enable ovarian cancer patient stratification for alpha therapy, optimizing dosing, monitoring efficacy, and boosting physician confidence for faster market adoption. The growing need for alpha emitters in recurrent and chemo resistant ovarian disease drives segmental market growth.

End User InsightsThe hospitals segment dominated the end-user segment with a revenue share of 68.70% in 2025, as oncology hospitals maintain shielded radiopharmacies capable of isotope handling, radiolabeling, and dose preparation. Alpha-emitter therapy requires coordinated expertise from nuclear medicine specialists, oncologists, and safety officers, which large hospitals provide through integrated oncology care teams.

The diagnostic centers segment is projected to grow at a CAGR of 11.98% during the forecast period. Diagnostic centers are rapidly deploying advanced PET/SPECT imaging platforms capable of identifying molecular targets used in alpha-emitter therapies. Increasing use of radiotracer-based companion diagnostics and growth of nuclear medicine imaging networks collectively boost segment growth.

Competitive LandscapeThe alpha emitter market is moderately consolidated, featuring global pharmaceutical leaders and specialized oncology-focused firms. Companies such as Bayer AG, Novartis AG, Pfizer Inc., and Eli Lilly and Company maintain strong positions through established radiopharmaceutical portfolios, robust distribution channels, and ongoing clinical research. Smaller players and biotech firms focus on novel alpha-emitting isotopes and targeted delivery systems. Competition is primarily driven by therapeutic efficacy, safety, regulatory approvals, and manufacturing capabilities, with future growth likely fueled by next-generation alpha therapies and precision oncology applications.

List of Key and Emerging Players in Alpha Emitter Market Bayer AG Novartis AG Actinium Pharmaceuticals Inc. Alpha Fusion Fusion Pharmaceuticals Inc. Telix Pharmaceuticals Ltd Alpha Tau Medical Ltd IBA Radiopharma Solutions RadioMedix Inc. Orano Med SAS Curium Pharma BWXT Medical Ltd Cardinal Health Inc. Eckert & Ziegler ITM Isotopen Technologien Mnchen SE Nucleus RadioPharma ARTBIO Cyclotek Australia Pty Ltd SHINE Technologies LLC

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment