403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Point-Of-Care Molecular Diagnostics Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

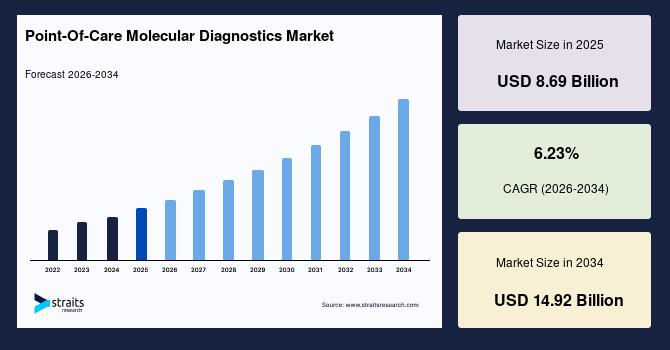

| 2025 Market Valuation | USD 8.69 Billion |

| Estimated 2026 Value | USD 9.20 Billion |

| Projected 2034 Value | USD 14.92 Billion |

| CAGR (2026-2034) | 6.23% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Abbott, Cepheid, Hemex Health, En Carta, Bayer AG |

to learn more about this report Download Free Sample Report

Emerging Trends in Point-Of-Care Molecular Diagnostics Market Increasing Use of Fully Integrated Sample-to-Answer SystemsPoint-of-care molecular diagnostics is witnessing a shift toward fully integrated sample-to-answer systems that combine nucleic acid extraction, amplification, and detection within a single portable unit while simultaneously connecting to digital health platforms. This trend is shaping the market by enabling seamless data transfer to electronic medical records and public health databases, which enhances real-time disease tracking and clinical decision-making. It is influencing manufacturers to design interoperable devices with built-in connectivity features, cybersecurity compliance, and cloud-based analytics capabilities, making products more aligned with modern healthcare IT infrastructure.

Growing Preference for Multiplex Molecular AssaysThe growing preference for multiplex molecular assays that can detect multiple pathogens from a single sample is reshaping the market landscape. This trend enhances clinical efficiency by reducing the need for multiple tests and enabling comprehensive diagnosis in a shorter time frame, particularly for respiratory and infectious diseases. It is compelling manufacturers to invest in advanced assay design and microfluidic technologies that support high-throughput, multi-target detection while maintaining sensitivity and specificity.

Market Drivers Increasing Need for Rapid Antimicrobial Stewardship and Growth of Decentralized Clinical Trials Drives MarketRising global concern around antimicrobial resistance increases demand for point-of-care molecular diagnostics that identify pathogens and resistance markers at the site of care. This demand pushes manufacturers to expand supply by developing rapid, highly sensitive assays and compact diagnostic platforms. Faster and more precise testing improves clinical decision-making and supports targeted therapy, which reduces unnecessary antibiotic use. Healthcare providers increasingly adopt these solutions as they help improve patient outcomes and align with antimicrobial stewardship goals. As a result, the market grows steadily with stronger demand for advanced diagnostics and continuous product innovation from suppliers.

The expansion of decentralized clinical trials increases demand for point-of-care molecular diagnostics that operate reliably outside traditional laboratory settings. This demand encourages manufacturers to increase the supply of portable, easy-to-use, and regulatory-compliant diagnostic devices. These tools enable real-time patient monitoring and faster data collection, which improves trial efficiency and reduces reliance on centralized labs. Clinical research organizations adopt these solutions to enhance flexibility and maintain consistent data quality across multiple locations. Thus, the market expands with increased availability of decentralized diagnostic solutions and higher adoption across clinical trial environments.

Market Restraints Inconsistent Sample Collection & Handling and Limited Reimbursement Alignment Restrains Point-of-Care Molecular Diagnostics Market GrowthInconsistency in sample collection and handling in non-laboratory settings acts as a key restraining factor in the point-of-care molecular diagnostics market. This issue reduces diagnostic accuracy and creates variability in results, which weakens trust in these solutions compared to centralized laboratory testing. Healthcare providers remain cautious in adopting such technologies due to concerns about reliability and clinical validity. As a result, market growth slows as adoption remains limited despite technological advancements.

Underdeveloped reimbursement frameworks act as another major restraining factor in the market. These frameworks do not fully cover the higher costs and clinical value of advanced point-of-care molecular diagnostics, which limits financial incentives for adoption. Healthcare facilities, especially in cost-sensitive regions, hesitate to invest in these solutions due to budget constraints and uncertain returns. This leads to restricted market expansion as adoption remains uneven across regions and healthcare settings.

Market Opportunities Emerging CRISPR-based Diagnostics and Home-based Solutions Offer Growth Opportunities for Point-of-Care Molecular Diagnostics Market PlayersThe increasing preference for home-based healthcare offers lucrative opportunities for the point-of-care molecular diagnostics market by expanding testing beyond traditional clinical environments. This trend creates growth opportunities by driving demand for simple, reliable, and user-friendly diagnostic solutions suitable for non-professionals. Manufacturers focus on intuitive designs, compact formats, and easy result interpretation to meet this demand. The market progresses toward wider consumer adoption with new revenue streams driven by at-home diagnostic use.

Emerging CRISPR-based diagnostic methods open avenues for market players to offer highly specific and rapid detection of nucleic acids without complex instrumentation. This capability creates growth opportunities by supporting the development of ultra-fast and cost-effective testing solutions, especially in resource-limited settings. Manufacturers respond by exploring innovative assay designs that leverage CRISPR systems to enhance performance. The market evolves toward more accessible and high-precision diagnostics with improved sensitivity and faster turnaround times.

Regional Insights North America: Market Leadership Driven by Advanced Healthcare Infrastructure and High Adoption of Rapid TestingNorth America accounted for a dominating share with 47.27% in 2025, supported by highly developed healthcare systems and strong integration of advanced diagnostic technologies. The region benefits from widespread adoption of decentralized and near-patient testing across hospitals, urgent care centers, and retail clinics, enabling faster clinical decision-making and improved patient outcomes. High prevalence of infectious and chronic diseases, along with a growing aging population, continues to increase demand for rapid molecular diagnostics. Strong investment in R&D and early adoption of innovative platforms such as portable PCR and multiplex testing systems further accelerate market expansion.

The US point-of-care molecular diagnostics market is influenced by the transition from centralized laboratory testing to point-of-care settings, which reduces diagnostic delays and enhances treatment efficiency. Increasing use of molecular diagnostics in primary care, emergency departments, and homecare settings is strengthening adoption. The rise in infectious diseases and chronic conditions, along with increasing acceptance of self-testing solutions, is encouraging manufacturers to develop user-friendly and portable diagnostic platforms tailored for decentralized use.

Canada's point-of-care molecular diagnostics market is driven by a focus on improving healthcare accessibility across rural and remote regions, a key growth driver promoting the adoption of point-of-care molecular diagnostics. Public healthcare initiatives are supporting the integration of rapid testing solutions to reduce diagnostic turnaround times and enhance early disease detection. Increasing emphasis on community-based care and decentralization of laboratory services is encouraging demand for compact and easy-to-use molecular diagnostic devices.

Asia Pacific: Fastest Growth Driven by Expanding Healthcare Access and Rising Disease BurdenThe Asia Pacific region is expected to register the fastest growth with a CAGR of 8.23% during the forecast period, with strong growth driven by improving healthcare infrastructure and rising awareness of early diagnosis. The region is experiencing increased demand for rapid diagnostic solutions due to a high burden of infectious diseases and a large population base. Governments are investing in strengthening healthcare systems and expanding diagnostic services in rural and underserved areas. Growing adoption of portable and cost-effective molecular diagnostic tools is enabling wider penetration of point-of-care testing across diverse healthcare settings.

India's market growth is strongly influenced by government initiatives aimed at strengthening diagnostic capabilities at the primary healthcare level. Programs focused on expanding testing infrastructure in rural and semi-urban areas are increasing the adoption of point-of-care molecular diagnostics. The high prevalence of infectious diseases such as tuberculosis and respiratory infections is creating sustained demand for rapid and accurate diagnostic solutions. The push toward affordable healthcare and indigenous manufacturing of diagnostic devices is encouraging companies to develop low-cost, scalable molecular testing platforms suitable for resource-limited settings.

The market in South Korea is driven by its strong biotechnology sector and focus on advanced diagnostic innovation. The country has established robust capabilities in molecular diagnostics, supported by continuous investment in research and development.

Emphasis on rapid response systems for infectious disease outbreaks is accelerating the adoption of point-of-care molecular technologies. Integration of digital health solutions and automation in diagnostics is enabling efficient testing workflows, which supports market growth. Local companies are actively developing high-performance diagnostic kits and portable systems, enhancing the country's competitiveness in this space.

The Japanese market growth is primarily supported by its rapidly aging population, which increases the need for early and accurate disease detection. The demand for point-of-care molecular diagnostics is rising as healthcare systems focus on managing age-related chronic and infectious conditions efficiently. The country's advanced healthcare infrastructure and strong emphasis on precision medicine are encouraging the adoption of highly sensitive molecular diagnostic technologies. Continuous innovation in compact diagnostic devices and integration with clinical workflows is enabling wider use of point-of-care testing, particularly in hospitals and outpatient care settings.

By Product TypeTest kits dominated the product type segment, accounting for a share of 42.34% in 2025 due to their ease of use, rapid turnaround time, and minimal requirement for specialized infrastructure. These kits are designed for decentralized settings where quick clinical decisions are critical, making them highly suitable for infectious disease detection in emergency and remote care environments. Their cost-effectiveness and compatibility with portable diagnostic platforms further strengthen adoption. The increasing demand for self-testing and near-patient diagnostics continues to drive manufacturers to develop highly sensitive, multiplex, and user-friendly test kits, reinforcing their dominant position.

The analyzers segment is expected to register a growth rate of 7.12% during the forecast period, as healthcare systems increasingly adopt compact and automated molecular diagnostic devices for point-of-care settings. The growth is driven by technological advancements that enable analyzers to deliver laboratory-grade accuracy with reduced manual intervention. Integration of digital connectivity, data management systems, and AI-enabled interpretation enhances their utility in clinical workflows. Rising demand for decentralized diagnostics and the need for scalable testing solutions in outbreak scenarios are encouraging manufacturers to invest in portable and high-throughput analyzers.

By TechnologyPCR technology dominated the market with a share of 66.37% due to its high sensitivity, specificity, and established clinical reliability in detecting infectious pathogens. Its widespread acceptance in clinical diagnostics and continuous innovation in real-time and rapid PCR platforms make it a preferred choice for point-of-care applications. The ability of PCR to provide accurate results within a short time frame supports its use in critical care and disease surveillance. Manufacturers continue to enhance PCR platforms by reducing processing time and improving portability, which sustains their leadership in the market.

Genetic sequencing is the fastest-growing segment, registering a CAGR of 7.45% during the forecast period, as advancements in sequencing technologies enable rapid and comprehensive pathogen identification at the point of care. The increasing focus on precision medicine and the need to detect genetic variations and emerging strains are accelerating its adoption. Miniaturization of sequencing devices and reductions in cost are making this technology more accessible for decentralized settings. Companies are investing in developing user-friendly sequencing platforms that can deliver actionable insights quickly, driving growth in this segment.

By End UserDecentralized laboratories dominated the end-user segment with a 43.14% share in 2025 as healthcare delivery shifted toward localized and rapid diagnostic solutions. These settings benefit from point-of-care molecular diagnostics by reducing dependence on centralized labs and enabling faster clinical decision-making. The increasing burden of infectious diseases and the need for immediate diagnosis in outpatient and remote settings support the expansion of decentralized laboratories. Manufacturers are focusing on developing compact, easy-to-use diagnostic systems tailored for such environments, reinforcing their dominance.

Home care represents the fastest-growing segment, expected to grow at a CAGR of 7.68% during the forecast period, as patients increasingly prefer convenient and accessible diagnostic solutions. The rise in chronic and infectious diseases, along with the growing emphasis on self-monitoring, is driving demand for home-based molecular testing. Technological advancements have enabled the development of simple, reliable, and user-friendly diagnostic kits suitable for non-professional use. The shift toward personalized healthcare and reduced hospital visits is encouraging companies to innovate in home care diagnostics, accelerating growth in this segment.

Competitive LandscapeThe point-of-care molecular diagnostics market is moderately fragmented. The competitive landscape comprises global diagnostics leaders, specialized molecular testing firms, and innovative startups focusing on cartridge-based and portable platforms. Established players primarily compete on factors such as extensive test menu breadth, integrated instrument-consumable ecosystems, pricing power through reagent cartridges, regulatory approvals, and digital connectivity features that enable workflow integration and customer lock-in. In contrast, emerging players compete on affordability, rapid innovation in microfluidics and lab-on-chip technologies, flexibility in assay development, and targeting underserved or decentralized settings such as home care and low-resource environments. The market in the future will be shaped by increasing ecosystem-based competition driven by integrated platforms, decentralized testing adoption, and continuous technological innovation in rapid molecular diagnostics.

List of Key and Emerging Players in Point-Of-Care Molecular Diagnostics Market Abbott Cepheid Hemex Health En Carta Bayer AG Hoffmann-La Roche AG Nova Biomedical QIAGEN Nipro Diagnostics Danaher Bio-Rad Laboratories, Inc. bioMérieux Agilent Technologies, Inc. Abaxis OraSure Technologies Waters Corporation Aptitude Medical Systems BD Recent Developments-

In March 2026, Abbott announced the acquisition of Exact Sciences for approximately USD 23 billion to expand its molecular diagnostics portfolio.

In February 2026, Cepheid was selected as a national collaborator under the federal diagnostic preparedness program (IDIQ contract) by the US FDA.

In February 2026, Hemex Health received FDA breakthrough device designation for the Gazelle Hb variant test.

In January 2026, En Carta Diagnostics received FDA Breakthrough Device designation for a POC molecular diagnostic platform.

In October 2025, Cepheid's Xpert MTB/XDR test received World Health Organization (WHO) prequalification.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.69 Billion |

| Market Size in 2026 | USD 9.20 Billion |

| Market Size in 2034 | USD 14.92 Billion |

| CAGR | 6.23% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product Type, By Technology, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

to learn more about this report Download Free Sample Report

Point-Of-Care Molecular Diagnostics Market Segments By Product Type-

Analyzers

Test Kits

Reagents

-

PCR

Genetic Sequencing

Hybridization

Microarray

-

Decentralized Laboratories

Hospital

Homecare

Assisted Living Healthcare Facilities

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment