403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Rates: Euribor Gets An Update

(MENAFN- ING) An Updated Euribor methodology will be phased in over six months from May onwards

Source: EMMI, ING The changes in the waterfall approach – getting rid of“estimates”

Source: EMMI, ING What is the impact?

The methodology underlying Euribor is getting an update that will be phased in over six months starting mid-May, the benchmark's administrator EMMI announced this week . The benchmark had moved from a purely quote based to a hybrid methodology in 2019, anchoring submissions in actual transactions as far as possible.

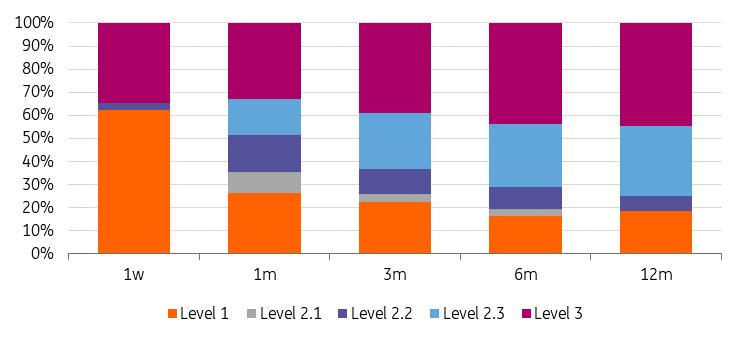

Currently panel banks make their submissions following a three-level hierarchical approach. At the bottom of this waterfall structure – the Level 3 – banks were required to make submissions based on own estimates and modelling when no transaction data is available. EMMI's transparency data for January showed that in the 6m and 12m tenors around 44% of contributions made use of Level 3.

Use of each level of the hybrid methodology (January 2024)Source: EMMI, ING The changes in the waterfall approach – getting rid of“estimates”

This Level 3 will now be scrapped. At the same time the second Level will be reformulated – to be precise Level 2.3 which relies on external input data for its calculation. Currently Level 2.3 submissions would use the most recent transaction based Level 1 submission and add a Market Adjustment Factor (MAF), which would reflect market moves since the last Level 1 rate. The MAF itself is based on Euribor Futures prices. The new formulation would also allow any prior Level 2 submissions as starting point, while the MAF would be calculated from changes in the OIS market and in Euribor-OIS spread. The OIS is based on the Efterm forward-looking €STR-based benchmark which has since been developed.

On the operational level the changes are expected to reduce the risk exposure and operational burden for panel banks and as such they are anticipated to help attract more banks to the panel and therefore increase the overall robustness of the benchmark. For the Euribor rates itself removing the reliance on Euribor Futures gets rid of the situation where the fixings change could be based on the markets expectation thereof – a bit of a catch-21 situation which had been a weak point of the current methodology. Simulations of the updated methodology that were run before the consultation was started showed that the volatility of longer tenor Euribor fixings could increase somewhat.

Volatility (in bp) of Euribor fixings under the current and updated methodologySource: EMMI, ING What is the impact?

Will this have an effect on Euribor/OIS spreads and IRS/OIS bases? All else equal the higher volatility of the fixings could entail some widening pressure on the bases, but the increases in volatility from the changes appear minor. We would think that if there were an impact on the bases from structural changes, these might come more from the direction of the ECB and its review of the operational framework. We should get more information soon with ECB's Lagarde having just indicated that details could be released on 13 March. While it is expected that there will also be a transition period of a couple of years the changes could entail a tightening of the refinancing rate – deposit facility rate corridor to make funding via ECB operations more attractive for banks. Crucial would also be any indications of what level of excess liquidity in the banking system the ECB targets in the long run and what balance it chooses between supplying liquidity via operations and via a bond portfolio.

Author:Benjamin Schroeder

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment