403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Automotive Fault Circuit Controller Market Size, Share, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

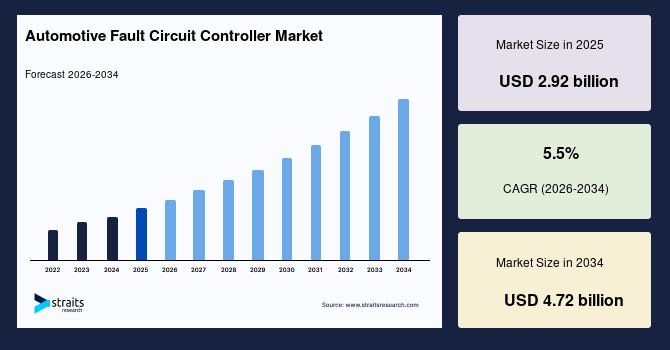

| 2025 Market Valuation | USD 2.92 billion |

| Estimated 2026 Value | USD 3.07 billion |

| Projected 2034 Value | USD 4.72 billion |

| CAGR (2026-2034) | 5.5% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Infineon, Littelfuse, TE Connectivity, Aptiv, Continental |

Download Free Sample Report to Get Detailed Insights.

Market Growth Factors Move to solid-state protection and intelligent fusesTraditional mechanical fuses and electromechanical breakers are increasingly replaced by solid-state (electronic) breakers and smart fuses that enable faster disconnect, programmable trip curves, and health telemetry. Solid-state FCCs reduce arcing and enable remote reset, which is valuable for fleet vehicles and autonomous platforms.

-

For example, in March 2025, Infineon Technologies released the Power PROFET+ 24/48V smart power switch family, designed to meet the demands of modern vehicle power systems by providing enhanced solid-state fuse functionalities for 24V and 48V applications.

This evolution elevates the market by enhancing FCC performance in high-voltage systems, supporting functional safety standards like ISO 26262, and increasing component prices through added diagnostics.

Regulatory and safety requirementsHeightened regulations on electrical safety and diagnostics mandate robust FCCs for fire prevention and fault logging, aligning with standards like ISO 26262 for functional safety. This propels market advancement by prioritizing compliant, telemetry-rich devices that reduce incidents and ease servicing, boosting OEM specifications and supplier credibility. It drives uniform adoption across segments, elevating costs but yielding long-term savings via fewer recalls. However, it burdens smaller players with certification, contributing to a more mature, safety-focused ecosystem.

Market Restraint Cost pressure and aftermarket price sensitivityAdvanced FCCs with solid-state breakers, superconducting devices, and telematics-enabled modules cost more than conventional fuses and basic breakers. In price-sensitive segments like entry passenger vehicles, many commercial fleets, OEMs, and tier-1 suppliers can oversee the perceived benefits to cut component cost and assembly complexity. Suppliers therefore face pressure to scale production, reduce BOM cost, and prove payback via warranty reduction or lighter harnesses to persuade cost-conscious programs. This constraint slows volume penetration in LCVs and lower segments until per-unit costs fall.

Market Opportunity Value in autonomous and commercial fleetsCommercial fleets and autonomous vehicles create strong opportunities for the automotive fault circuit controller (FCC) market. These platforms require maximum uptime, safe fault isolation, and remote diagnostics to avoid costly breakdowns. FCCs with intelligent monitoring, fast disconnection, and remote reset functions are especially valuable for robotaxis, delivery fleets, and electric trucks, where reliability directly affects profitability.

-

For example, in March 2025, ZF announced new smart power distribution modules for commercial EVs with embedded diagnostics designed to support fleet electrification programs

Overall, FCCs can evolve from simple safety devices into tools for predictive maintenance and fleet optimization. As autonomous and electric fleets expand, demand for advanced FCCs will accelerate.

Regional AnalysisNorth America leads the automotive fault circuit controller (FCC) market due to its advanced automotive industry and rapid adoption of electric vehicles. The region's focus on vehicle safety and smart manufacturing drives FCC demand for battery management and advanced driver-assistance systems. Strong R&D investments by automakers and suppliers enhance FCC integration in automated production lines. Government initiatives supporting EV infrastructure and Industry 4.0 adoption further boost the market. Collaborations between OEMs and technology providers ensure innovative FCC solutions, solidifying North America's dominance in the global market.

Asia PacificAsia Pacific is the fastest-growing region for the automotive FCC market, driven by high vehicle production and government-led electrification initiatives. The region's push for electric vehicles and smart manufacturing increases FCC demand for safe electrical systems and advanced driver-assistance systems. Local automakers and suppliers innovate to meet rising safety standards, while government policies promoting sustainable mobility fuel market growth. The expansion of automotive electronics and autonomous driving technologies further accelerates FCC adoption, positioning the Asia Pacific as a dynamic growth hub.

Country Insights United StatesThe U.S. market for AFCCs is driven by rapid electrification of vehicle platforms, growing fleet electrification programs, and large public investments in onshore semiconductor and power-electronics capacity. Policies and funding under the CHIPS & Science Act support local production of power semiconductors and packaging, which reduces supply-side risks for AFCC makers that rely on Si/SiC devices. OEMs and Tier-1 suppliers (electrical distribution and BMS providers) are launching platform consolidations that favor integrated AFCC solutions.

CanadaCanada's AFCC demand is supported by federal programs that expand EV infrastructure and accelerate EV uptake, because vehicle electrification increases the need for battery protection and high-voltage distribution modules. Recent federal funding rounds for EV chargers and related infrastructure reflect an ongoing national push to enable EV adoption and fleet electrification, creating fleet demand for reliable fault-isolation hardware and onboard protection. Canadian procurement and fleet-transition incentives also favour domestic supplier partnerships and aftermarket service demand.

GermanyGermany's advanced automotive and machinery base is a structural advantage for AFCC uptake. Recent fiscal measures and tax incentives in 2025 aim to accelerate corporate investment in EV production and capital equipment, which raises demand for high-voltage protection and intelligent power distribution modules. German OEMs' strong emphasis on functional safety, system reliability, and modular architectures favors AFCCs that combine rapid fault isolation with diagnostics.

ChinaChina remains a high-growth market for AFCCs because of very large NEV (new energy vehicle) production and aggressive policy support for electrification, local supplier ecosystems, and autonomous vehicle testing. Government guidance for 2025 NEV targets and regulatory activity to accelerate Level-3 approvals and EV market orderliness, sustain high volumes of battery protection and charging-safety requirements. Domestic EV OEMs and battery makers are important adopters of AFCCs, and many suppliers localize production to meet cost and timing needs.

IndiaIndia's AFCC market is expanding as national initiatives encourage EV adoption, scale up battery and component manufacturing, and seek domestic capabilities for critical parts, including rare-earth magnets and power electronics. Recent policy moves incentivize local manufacturing and critical materials reduce import dependence for EV subsystems and spur demand for AFCCs in both two-/three-wheeler electrification and passenger/LCV electrification programs. The combination of PLI-style incentives and industrial policy supports localized supplier development for protection and distribution modules.

Type InsightsSolid-state AFCCs are the dominant type of subsegment because they enable faster switching, finer control, longer lifecycle, and easier integration into software-defined architectures than electromechanical fuses and relays. Solid-state devices provide instant interruption, support electronic reclosers and selective isolation, and can be combined with diagnostics and current-limiting strategies that protect sensitive electronics. Cost reductions in power semiconductor manufacturing and increased supplier investment make solid-state solutions commercially viable across more vehicle segments.

Voltage InsightsHigh-voltage AFCCs dominate because electrified powertrains require dedicated protection equipment for voltages that are dangerous and potentially destructive if faults occur. High-voltage AFCCs address isolation monitoring, ground-fault detection, contactor control, and safe shutdown under crash or thermal events. The expanding share of BEVs (which rely on 400–800 V architectures), regulatory testing for HV safety, and OEM platform strategies that standardize HV protection modules across model families drive the segment's growth.

Vehicle Type InsightsPassenger cars are the dominant vehicle class for AFCC demand because they represent the largest global vehicle population and are the first to adopt new electrical architectures and occupant-safety features at scale. Within passenger cars, battery electric vehicles (BEVs) and plug-in hybrids require more advanced fault protection than conventional ICE vehicles because of high-voltage battery systems, bidirectional power flow, onboard chargers, and stringent isolation requirements. Consequently, AFCCs tailored for BEV battery protection, charging safety, and high-voltage distribution become indispensable.

Sales Channel InsightsOEM supply is the dominant channel because AFCCs are safety-critical components typically integrated at vehicle assembly and designed to meet OEM engineering, reliability, and homologation requirements. OEM contracts provide scale, long development cycles, and recurring volume through model lifecycles. Warranty and liability considerations make OEM selection processes rigorous, but once a controller design is qualified across a vehicle platform, the supplier secures stable revenue. Public funding that supports domestic supplier retooling for EV components further strengthens OEM supply chains.

Competitive LandscapeThe automotive FCC market is highly competitive, with key players leveraging innovation, strategic partnerships, and mergers to maintain dominance. Companies focus on developing advanced FCCs with miniaturization, AI-driven diagnostics, and EV compatibility to meet rising safety and electrification demands. The market sees intense R&D investments to integrate FCCs with ADAS and IoT, driven by regulatory mandates and consumer demand for vehicle safety.

Infineon Technologies: A Leading PlayerInfineon is a strategic supplier in FCC value chains because it supplies power semiconductors (Si, SiC), smart power switches (Power PROFET family), microcontrollers, and system IP that OEMs use for protection and zone modules. Its growth pattern mixes product innovation (SiC, e-FETs, smart power), strategic M&A, and long OEM engagements (supply agreements for traction/inverter modules and microcontrollers).

Latest News:

-

In April 2025, Infineon announced plans to acquire Marvell's automotive Ethernet business for $2.5 billion, strengthening its automotive networking and domain controller capabilities.

-

Infineon

Littelfuse

TE Connectivity

Aptiv

Continental

Bosch

Denso

Valeo

Marelli

Renesas

STMicroelectronics

NXP

ON Semiconductor

Sensata

Eaton

Bel Fuse

Vishay

Delta Electronics

Hitachi Astemo

-

March 2025 - Infineon launched a new Power PROFETTM+ family optimised for 24/48 V automotive power distribution, offering lower on-resistance and targeted use in modern vehicle domains (useful for FCCs and zone modules).

January 2025 - Infineon Technologies and Flex partnered to develop and showcase the Flex Modular Zone Controller (ZCU) design platform at CES 2025, creating a scalable, automotive-grade solution for software-defined vehicles (SDVs).

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.92 billion |

| Market Size in 2026 | USD 3.07 billion |

| Market Size in 2034 | USD 4.72 billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Voltage, By Vehicle Type, By Sales Channel |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Automotive Fault Circuit Controller Market Segments By Type-

Solid-state breakers / electronic circuit breakers

Electromechanical breakers and contactors

Pyrotechnic/one-time fuses

Hybrid solutions

-

Low-voltage systems (≤48 V)

High-voltage systems (>48 V)

-

Passenger cars

Commercial vehicles

Off-highway and specialty

Aftermarket and retrofit

-

OEM

Tier-1 suppliers/module integrators

Aftermarket/service providers

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment