403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Cooling US Inflation Keeps The Fed On Track For Rate Cuts

(MENAFN- ING)

US inflation a touch softer than predicted

Source: Macrobond, ING Housing cost pressures linger

Source: Macrobond, ING The question of rate cut magnitude remains

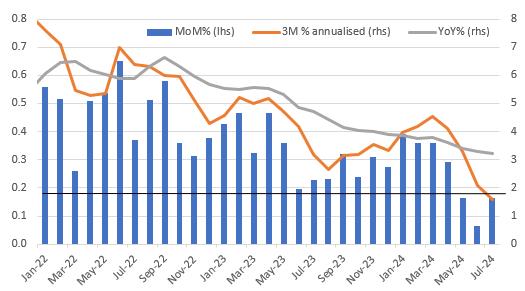

US consumer price inflation has risen 0.2% month-on-month for both headline and core, in line with expectations. However, it is slightly better than that as to 3 decimal places headline rose 0.155% and core rose 0.165%, both of which are below the 0.17% rate that over time brings us to 2% year-on-year. The chart below shows that we have had three consecutive readings below 0.17% MoM for core inflation and that the 3M annualised rate is now just 1.6%. The Fed has told us they won't wait for the YoY rate to hit 2% (currently 3.2%) before cutting interest rates, because if they do that the risk is they have left rates too high for too long. This would mean a greater chance of an undershoot in late 2025 / early 2026.

US core CPI metricsSource: Macrobond, ING Housing cost pressures linger

The details show apparel prices fell 0.4% MoM while transportation fell 0.1% thanks to falling new and used vehicle prices and a 1.6% drop in airline fares. Medical care costs also fell. Supercore (services ex food, energy and housing) rose 0.21% after two consecutive negative prints, but remember we had averaged above 0.5% MoM in the first four months of the year, so there is still a clear moderation, with this component effectively averaging 0% over the past 3M. In general the numbers can be choppy, but we don't believe we are on the cusp of a renewed pick up in prices – unit labor costs suggests the "costs" side of things looks well behaved while surveys of corporate pricing behaviour, such as the NFIB price intentions series and regional Fed surveys of prices received, continue to moderate.

The one area of real disappointment was housing with primary rents up 0.5% MoM and owners' equivalent rent up 0.4%. Recent numbers had been tracking more in line with private surveys on housing costs, so the re-acceleration today is a surprise. The market has seemingly moved to reduce the pricing of a 50bp cut in September on the back of this.

Housing costs MoM% re-accelerateSource: Macrobond, ING The question of rate cut magnitude remains

Nonetheless, this report should help to cement expectations for another 0.2% MoM and quite possibly 0.1% print for the Fed's favored inflation measure – the core PCE deflator – in a couple of weeks' time. That would ensure a Fed rate cut in September in light of the cooling jobs market and softening business surveys with it only being a question of magnitude. For now we favour a 50bp to start off as the Fed plays catch-up to the data before reverting to 25bp moves thereafter. However, the jobs report, published on 6 September is critical for this view. A soft payrolls and another move higher in the unemployment rate and then a 50bp move looks assured. A strong jobs number and perhaps a dip in the unemployment rate back to 4.2% and it will be a 25bp cut.

Author:James Knightley

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment