Hungarian Inflation Falls Into Single Digits

| 9.9% | Headline inflation (YoY)

ING estimate 10.3% / Previous 12.2% |

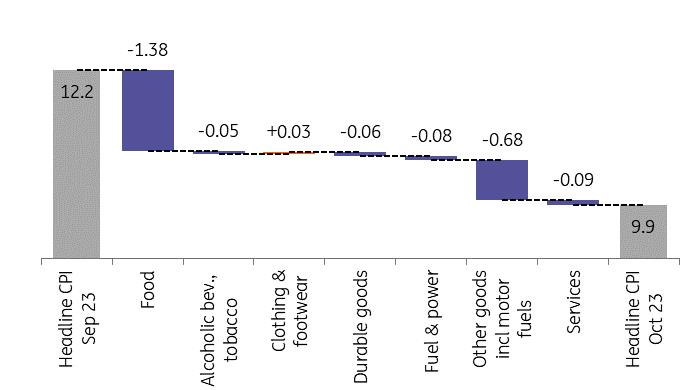

The analyst community had expected a marked easing in the annual inflation rate in October. However, almost no one was betting on a fall below 10% right now. Yet the reading was in line with the government's communication, which had gained momentum in recent weeks and months, that inflation could be in single digits as early as November. Two factors contributed to the headline inflation rate of 9.9%: last year's high base and monthly deflation. According to the Statistical Office's data collection, the average price of the consumer basket fell by 0.1% in October compared with September.

At first glance, therefore, the inflation trend is clearly positive. However, it is worth noting that core inflation rose by 0.3% on a monthly basis. This also means that the surprisingly strong disinflation and monthly deflation are clearly driven by price changes in products not included in the core inflation basket. Among these, the 3.8% fall in fuel prices stands out. In addition, unprocessed food prices also fell significantly on a monthly basis.

Main drivers of the change in headline CPI (%)

HCSO, ING The details

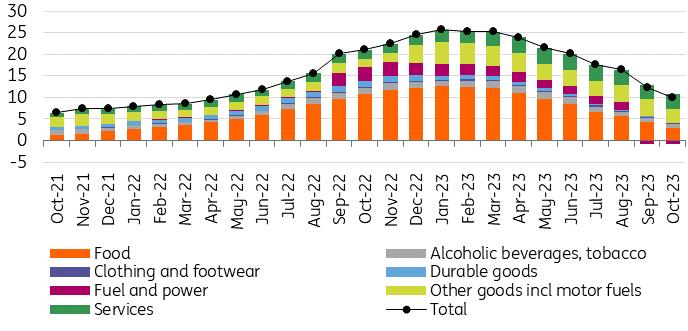

- Disinflation in food prices continued in October, helped by the base effect and the month-on-month decline in both unprocessed and processed food prices. While the year-on-year print moved lower to 10.4%, it hardly tells the full story. Compared to December 2020, food prices are still 63.2% higher while we have seen food retailing plummet. Fuel prices dropped by 3.8% on a monthly basis, causing some downside surprise compared to publicly available information. While oil prices in HUF came in lower by 2.4% in October, it seems the retail margin of fuel retailers narrowed significantly as well. The food and fuel price declines were overwhelming, responsible for 89% of the 2.3ppt disinflation compared to September. The other items show minimal disinflationary forces. All the main items – except clothing – have seen a decline in the year-on-year inflation print. Durables goods inflation slowed to only 0.7% YoY as a result of weaker inflation among the most important trade partners and a stable EUR/HUF exchange rate. The 13.2% year-on-year rate of increase in the price of services has become the second largest contributor to the headline inflation reading after fuel and should now be the focus of attention. This is especially true in light of the expected minimum wage increase of 10-15%, which implies another significant cost increase and price increase potential for labour-intensive sectors, including services.

HCSO, ING Underlying inflation also improves, but risks lurk

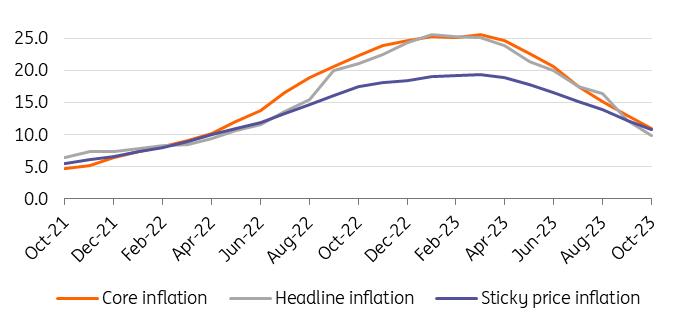

As the downward pressure on inflation in October came mainly from processed and unprocessed food, disinflation was strong in the core basket as well. The core reading fell 2.2ppt to 10.9% YoY. While the month-on-month print showed 0.3% core inflation, base effects helped a lot.

The quarter-on-quarter annualised seasonally-adjusted core inflation rate is now 2.7%, which is roughly in line with price stability. We are not saying that the job is done, but the recent underlying inflation performance is clearly encouraging. Unfortunately, we don't expect that core inflation will be able to remain that subdued during 2024 due to a lot of changes and risks which will probably translate into an uptick in monthly repricing.

Headline and underlying inflation measures (% YoY)

HCSO, NBH, ING

In terms of average inflation in 2023, we continue to expect an inflation print around 17.8%. When it comes to the year ahead, we forecast an average price increase of 5-6% next year, with risks tilted to the upside. The increase in excise duty on fuel from January, the reshuffled extended producer responsibility (EPR) scheme, the introduction of the mandatory Deposit and Return System ensuring the return of beverage packaging for recycling or reuse, the expected high minimum wage increase, significant geopolitical risks, and the fiscal situation which may justify some tax increases, all pose major inflation risks that could stop or in the worst case scenario, reverse this year's disinflationary trend in 2024.

After this inflation print, all eyes are on the forintAs far as monetary policy is concerned, we see the chances of a 100bp rate cut increasing significantly. In October, there were three options on the table when the Monetary Council decided on the size of the easing: 50, 75 or 100 basis points. The October figures for both headline and core inflation were in the more favourable, lower half of the forecast range in the September Inflation Report. As a result, we believe that the 50bp option can be taken off the table, when it comes to the November rate-setting meeting.

If EUR/HUF can hold the recent level of 377-378 (which is 1.6% stronger than around the end of October), the single-digit inflation print may be convincing enough for some members of the Monetary Council to opt for a 100bp cut instead of continuing with 75bp. Although it is too early for a high conviction call (especially after Deputy Governor Barnabás Virág's recent message stressing the need for a disciplined monetary policy), the latest price and market stability data point in the direction of a possible fine-tuning in the pace of easing.

But to be fair, it doesn't matter whether the latest inflation reading is just below or just above 10%. Politically it may matter, but from an economic policy perspective the CPI target is still 3% and there is a long way to go to get there. Today's data hasn't changed our longer-term monetary policy view, i.e. we still see a need for a +200bp real interest rate environment to keep HUF stable and achieve the inflation target over the monetary policy horizon. The only thing that can change after today's CPI result is the short-term trajectory of easing in the policy rate to the 7-8% terminal rate, in line with our expected inflation rate of 5-6% in 2024.

Author:Peter Virovacz

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

- $MBG Token Supply Reduced By 4.86M In First Buyback And Burn By Multibank Group

- Mining Chemicals Market Size, Industry Trends, Growth Factors, Opportunity And Forecast 2025-2033

- Excellion Finance Launches MAX Yield: A Multi-Chain, Actively Managed Defi Strategy

- Pluscapital Advisor Empowers Traders To Master Global Markets Around The Clock

- UK Cosmetics And Personal Care Market To Reach USD 23.2 Billion By 2033

- Nonprofit Organization Consultancy Business Plan2025: Essentials For Entrepreneurs

More Story

Comments

No comment