403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Intensive Care Unit Equipment Market Size, Share, Report, 2034

| Company | Recent Activity | Timeline | Focus | Value |

|---|---|---|---|---|

| Clinomic | Series B Funding | April 2025 | Clinomic secured Series B funding to expand its AI-powered“Mona” platform designed for ICU workflow optimization, patient monitoring integration, and critical care data analytics across hospitals. | USD 26.6 Million |

| Premier Medical Systems | Manufacturing Investment | September 2025 | Premier Medical Systems announced investment for a new medical device manufacturing facility focused on ICU ventilators, infusion pumps, and critical care equipment production in India. | USD 6 Million |

| Market Metric | Details & Data (2025-2034) |

|---|---|

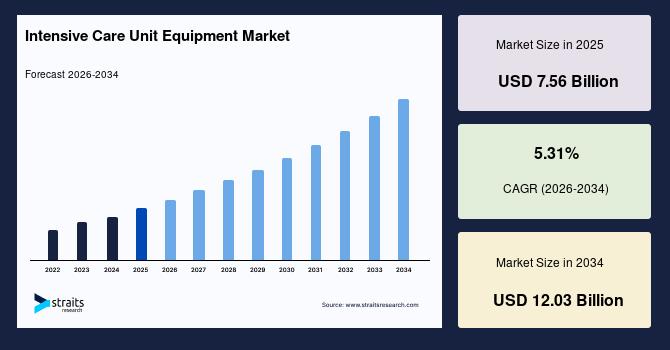

| 2025 Market Valuation | USD 7.56 Billion |

| Estimated 2026 Value | USD 7.95 Billion |

| Projected 2034 Value | USD 12.03 Billion |

| CAGR (2026-2034) | 5.31% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Medtronic (Ireland), GE HealthCare (US), Philips Healthcare (Netherlands), Dräger (Germany), Mindray Medical (China) |

Download Free Sample Report to Get Detailed Insights.

Intensive Care Unit Equipment Market Dynamics Market DriversRising Critical Care Admissions and Expansion of Advanced Hospital ICU Infrastructure Drives Market

The increasing incidence of severe respiratory disorders, cardiovascular diseases, sepsis, multi-organ failure, and trauma-related emergencies is significantly driving demand for advanced ICU equipment. Critical care units increasingly rely on ventilators, multiparameter monitoring systems, infusion pumps, and renal support equipment to manage high-acuity patient populations requiring continuous life-support intervention. For example, the World Health Organization reported that cardiovascular diseases continue to cause nearly 17.9 million deaths annually worldwide, substantially increasing ICU admissions requiring advanced hemodynamic monitoring and respiratory support systems across tertiary healthcare institutions and emergency treatment centers.

The rapid expansion of hospital ICU infrastructure and establishment of specialized critical care units are significantly increasing demand for advanced ICU equipment worldwide. Governments and healthcare providers are investing heavily in intensive care modernization, negative-pressure isolation rooms, smart monitoring integration, and high-dependency care facilities following healthcare capacity pressures observed during infectious disease outbreaks. Increasing adoption of centralized patient monitoring systems, connected ICU ecosystems, and high-acuity care models is further strengthening demand for integrated critical care technologies across developed and emerging healthcare markets globally.

Market RestraintsHigh Equipment Acquisition Costs and Electromagnetic Interference Risks Restrain Market

High acquisition and maintenance costs associated with advanced ICU equipment significantly restrain market growth, particularly across small hospitals and resource-constrained healthcare systems. Critical care technologies, including ventilators, ECMO systems, and integrated monitoring platforms, require substantial capital investment and recurring servicing expenses. For example, advanced ECMO systems from manufacturers such as Getinge and LivaNova can cost hospitals over USD 100,000 per unit, excluding disposable circuits and maintenance contracts, creating major financial barriers for ICU infrastructure modernization.

Electromagnetic interference between densely connected ICU devices acts as a significant restraint in advanced critical care environments. Intensive care units increasingly operate multiple high-frequency systems, including ventilators, infusion pumps, dialysis machine, portable imaging devices, and wireless patient monitoring platforms, within confined spaces. Signal interference and connectivity instability can affect data transmission accuracy, alarm synchronization, and device communication reliability. These technical limitations complicate integration of fully connected smart ICU ecosystems and increase operational concerns regarding patient safety and uninterrupted critical care monitoring.

Market OpportunitiesExpansion of Tele-ICU Networks and Rising Demand for AI-enabled Critical Care Solutions Offer Growth Opportunities for Market Players

The rapid expansion of tele-ICU infrastructure is creating strong growth opportunities for advanced ICU equipment integrated with remote monitoring and centralized critical care management capabilities. Healthcare systems increasingly deploy tele-intensive care platforms to address intensivist shortages, improve rural critical care access, and optimize multi-hospital ICU operations. These environments require interoperable ventilators, smart bedside monitors, and cloud-connected infusion systems capable of real-time clinical data transmission. Growing adoption of remote critical care management models continues strengthening demand for digitally connected ICU technologies.

Increasing adoption of AI-enabled clinical decision support systems is creating major growth opportunities in the ICU equipment market. Advanced patient monitoring platforms increasingly incorporate machine learning algorithms for early sepsis detection, ventilator optimization, predictive hemodynamic analysis, and automated alarm prioritization within intensive care environments. Integration of artificial intelligence with critical care equipment improves workflow efficiency, reduces alarm fatigue, and enhances rapid intervention capabilities for high-acuity patients. Growing focus on precision critical care and data-driven ICU management is accelerating investment in intelligent ICU equipment ecosystems worldwide.

Market ChallengesInteroperability Limitations and Alarm Fatigue Issues Challenges ICU Equipment Market Growth

Limited interoperability between ICU devices and hospital information systems acts as a major challenge in the ICU equipment market. Critical care environments often utilize equipment from multiple manufacturers, creating difficulties in seamless data integration, centralized monitoring, and synchronized clinical workflow management. Inconsistent communication protocols between ventilators, infusion pumps, bedside monitors, and electronic medical record systems reduce operational efficiency and increase dependency on manual data handling. These integration limitations restrict development of fully connected smart ICU ecosystems across healthcare institutions.

Alarm fatigue associated with continuous patient monitoring systems remains a significant challenge in intensive care environments. ICU clinicians are frequently exposed to excessive non-actionable alarms generated by multiparameter monitoring devices, ventilators, and infusion systems during routine patient management. High false-alarm frequency can contribute to delayed response times, desensitization, and increased cognitive workload among critical care staff. These operational challenges are increasing demand for intelligent alarm management technologies capable of improving alert prioritization and reducing unnecessary alarm burden in ICUs.

Intensive Care Unit Equipment Regional Outlook North America Intensive Care Unit Equipment MarketNorth America: Market Leadership through Deployment of Advanced Ventilators and Expansion of Tele-ICU Capabilities

The North America intensive care unit equipment market accounted for the largest regional share of 35.42% in 2025 due to widespread deployment of advanced ventilators, ECMO systems, and centralized patient monitoring infrastructure across high-acuity hospital networks in the US and Canada. The region is witnessing strong adoption of AI-enabled clinical surveillance platforms and smart ICU interoperability systems. Increasing expansion of neurocritical care units, sepsis management programs, and hospital-at-home critical monitoring models is accelerating demand for sophisticated ICU equipment across North America.

US Intensive Care Unit Equipment MarketThe US intensive care unit equipment market was valued at USD 2.43 million in 2025, driven by increasing utilization of ECMO support systems, advanced hemodynamic monitoring platforms, and AI-assisted ventilator management technologies across tertiary-care hospitals. Rising prevalence of sepsis, cardiovascular emergencies, and chronic respiratory disorders continues driving high ICU admission volumes nationwide. The market is additionally benefiting from rapid adoption of enterprise-wide remote patient monitoring infrastructure and increasing integration of predictive analytics within critical care workflows across large integrated healthcare delivery networks throughout the US.

Canada Intensive Care Unit Equipment MarketThe Canada ICU equipment market size was estimated at USD 241.25 million, driven by increasing investments in rural critical care connectivity and expansion of tele-ICU capabilities across geographically dispersed healthcare systems. Provincial hospitals are strengthening deployment of portable ventilators, transport monitoring systems, and integrated ICU command platforms to improve critical care accessibility. The market is also benefiting from growing collaborations between Canadian academic hospitals and medical technology companies.

Asia Pacific Intensive Care Unit Equipment MarketAsia Pacific: Fastest Growth Driven by Rapid Expansion of Tertiary Care Hospitals and Strong Adoption of High-precision Patient Monitoring Technologies

The Asia Pacific intensive care unit equipment market is expected to register the fastest growth with a CAGR of 7.68% during the forecast period, driven by rapid expansion of tertiary-care hospitals, increasing ICU bed installations, and rising adoption of advanced ventilation systems across India, China, and Southeast Asia. For example, India's PM Ayushman Bharat Health Infrastructure Mission continues expanding critical care hospital infrastructure nationwide. Expanding domestic manufacturing of ventilators and monitoring systems in China and Japan is further improving affordability and accelerating adoption of advanced ICU technologies.

China Intensive Care Unit Equipment MarketThe China intensive care unit equipment market was valued at USD 442.02 million in 2025, driven by the increasing establishment of hospital-based extracorporeal membrane oxygenation (ECMO) centers for severe respiratory and cardiopulmonary failure management. China has rapidly expanded ECMO adoption across large urban hospitals following national critical care capacity initiatives. Rising deployment of domestically developed AI-assisted patient monitoring platforms and increasing integration of 5G-enabled remote ICU connectivity solutions are further accelerating demand for advanced critical care equipment.

Japan Intensive Care Unit Equipment MarketThe ICU equipment market in Japan was valued at USD 336.19 million in 2025, led by increasing demand for advanced respiratory support and hemodynamic monitoring systems associated with the country's rapidly aging population. Strong adoption of high-precision patient monitoring technologies, closed-loop ventilation systems, and robotic-assisted critical care workflows across university hospitals in Tokyo and Osaka is strengthening market growth. Japan's advanced medical electronics industry and high concentration of elderly intensive care admissions are accelerating integration of intelligent ICU infrastructure.

India Intensive Care Unit Equipment MarketThe India intensive care unit equipment market was valued at USD 177.08 million in 2025 due to the rapid expansion of government-funded critical care infrastructure under Ayushman Bharat and the increasing establishment of ICU facilities across Tier-2 and Tier-3 cities. The rising prevalence of severe dengue, sepsis, antimicrobial-resistant infections, and chronic respiratory diseases is significantly increasing ICU admissions nationwide. Growing domestic manufacturing of ventilators and patient monitoring systems under the“Make in India” initiative is further improving affordability and accelerating deployment of advanced critical care equipment.

Intensive Care Unit Equipment Market Segmentation Analysis By Product TypeBy product type, respiratory support equipment accounted for a share of 31.20% in 2025 due to rising utilization of invasive ventilation in ARDS, sepsis-induced respiratory failure, and post-operative critical care management. Increasing deployment of high-flow oxygen therapy systems, ICU ventilator upgrades, and closed-loop ventilation technologies across tertiary hospitals further strengthened segment dominance.

The patient monitoring equipment segment is expected to grow at a CAGR of 6.17% during the forecast period, driven by increasing adoption of centralized ICU surveillance platforms, continuous hemodynamic monitoring, and AI-enabled early deterioration detection systems. Growing integration of multiparameter monitors with electronic medical records and smart alarm management technologies accelerated demand across high-acuity intensive care environments.

By End UseHospitals accounted for the largest end-use segment with a share of 69.31% in 2025 due to the high installation of ECMO systems, centralized ICU monitoring networks, and advanced ventilator infrastructure across tertiary-care facilities. Increasing expansion of cardiac, trauma, and neurocritical care units further accelerated procurement of sophisticated life-support and patient monitoring equipment.

The ambulatory surgical centers segment is expected to have the fastest growth in the end-use segment, registering a CAGR of 7.08% during the forecast period. This growth is driven by increasing adoption of short-stay minimally invasive surgeries requiring post-anesthesia critical monitoring and portable ventilatory support systems. Rising installation of compact patient monitoring platforms, smart infusion pumps, and rapid recovery care infrastructure within outpatient surgical facilities is further accelerating product demand.

Competitive LandscapeThe intensive care unit equipment market landscape is moderately consolidated, with major medical device companies competing across ventilators, patient monitoring systems, infusion pumps, renal support equipment, and smart ICU platforms. Established players such as Philips, GE HealthCare, Medtronic, Dräger, and Mindray dominate the market through diversified critical care portfolios, strong hospital partnerships, and global distribution capabilities. Competition in the market is driven by advancements in AI-enabled monitoring, connected ICU ecosystems, remote critical care management, and intelligent ventilation technologies. Emerging companies are focusing on interoperable monitoring platforms, portable ICU devices, and data-driven critical care automation solutions.

List of Key and Emerging Players in Intensive Care Unit Equipment Market-

Medtronic (Ireland)

GE HealthCare (US)

Philips Healthcare (Netherlands)

Dräger (Germany)

Mindray Medical (China)

Fresenius Medical Care (Germany)

Baxter International (US)

Becton Dickinson (BD) (US)

Nihon Kohden (Japan)

Stryker (US)

Getinge (Sweden)

Hamilton Medical (Switzerland)

Masimo (US)

ResMed (US)

Smiths Medical (US)

ICU Medical (US)

ZOLL Medical (US)

Teleflex (US)

February 2026: Danaher entered a definitive agreement to acquire Masimo for approximately USD 9.9 billion to expand pulse oximetry and acute-care patient monitoring capabilities.

October 2025: Hoag selected Philips for a 10-year patient monitoring collaboration to deploy IntelliVue MX750, X3 transport monitors, PIC iX, and Enterprise Monitoring as a Service across acute-care hospitals.

September 2025: Philips launched the Telemetry Monitor 5500 smart telemetry platform to support continuous enterprise-wide cardiac monitoring, alarm management, and scalable high-acuity bed surveillance.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.56 Billion |

| Market Size in 2026 | USD 7.95 Billion |

| Market Size in 2034 | USD 12.03 Billion |

| CAGR | 5.31% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product Type, End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Intensive Care Unit Equipment Market Segments By Product Type-

Patient Monitoring Equipment

-

Multiparameter Monitors

ECG Monitors

Hemodynamic Monitoring Systems

Capnography Monitors

Pulse Oximeters

Others

-

Mechanical Ventilators

CPAP/BiPAP Systems

Others

-

Hospitals

Ambulatory Surgical Centers (ASCs)

Specialty Clinics

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment