403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

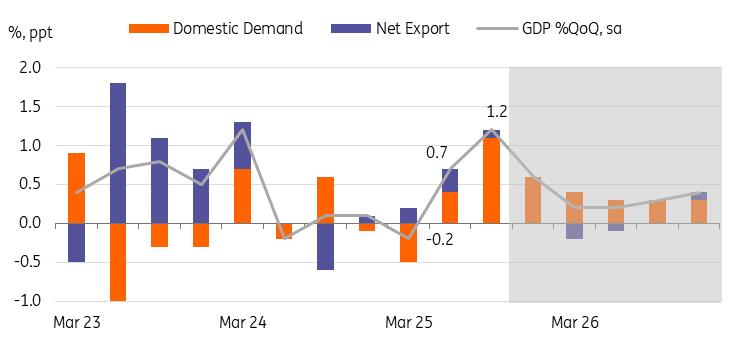

South Korean Growth Beats Expectations, Yet Fourth-Quarter Slowdown Likely

| 1.2% QoQ sa |

GDP

1.7% YoY |

| Higher than expected |

South Korean private consumption increased by 1.3% quarter-on-quarter, providing the primary driver of growth. Both goods and service consumption rose thanks to government support, strong stock market performance, and the normalisation of the political situation. However, we believe that the effects of government aid are likely to diminish. Also, recent housing market regulations may negatively affect consumption in the short term. Thus, this would weigh on overall growth in the current quarter.

Regarding investment, facility investment demonstrated a notable recovery, rising 2.4%, mainly due to increased IT investment. Construction activity contracted for the sixth consecutive quarter, but the rate of contraction showed signs of easing. We expect solid facility investment to continue as capital goods imports rose recently, while construction finally bottomed out. Thus, investment is likely to contribute positively to the current quarter.

Exports grew modestly by 1.5% thanks to strong exports of semiconductors and transportation equipment. We continue to believe robust semiconductor and vessel exports in coming quarters. But tariff headwinds and expected slowdown of US consumption should challenge overall exports going forward.

Looking ahead, GDP growth is expected to slow in the current quarter from 1.2% to 0.6%. We keep our 2025 annual GDP growth at 1.2%.

Korean GDP is expected to slow down in coming quarters

Source: CEIC Consumer sentiment edged down in October but remained above neutral level

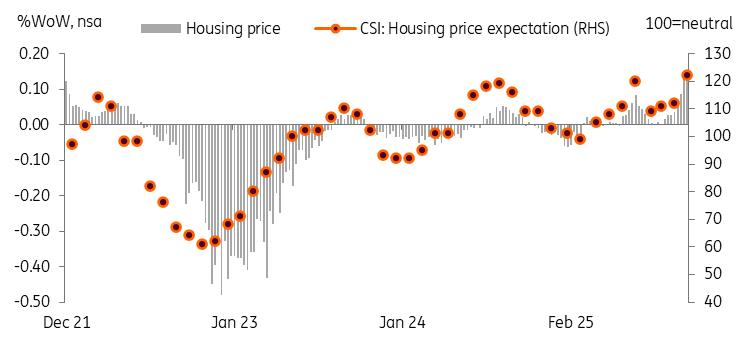

The composite consumer sentiment index edged down slightly to 109.8 from 110.1, but remains above 100, indicating continued optimism. Of the six subcomponents, expectations for the domestic economy declined; the rest were unchanged.

Also significant: a 10-point increase in consumer expectations on housing prices. Despite the implementation of recent, more stringent, measures prior to the survey, consumers continue to anticipate an upward trend in housing prices. This is expected to decrease in the coming months, while the Bank of Korea and the government are anticipated to exercise caution in policy decision-making.

That's why we believe a November rate cut is unlikely. Sentiment is a leading indicator of the actual housing market. Thus, the BoK should take a wait-and-see approach until it sees a clearer sign of stabilisation. In addition, President Lee publicly supported the BoK's on-hold decision thanks to housing market trends. So clearly, the prerequisite of a rate cut should be stabilisation of the housing market. We currently have a 25bp cut pencilled in for January, but we may push it to February or even April, depending on the housing market trend.

Housing prices are key to watch

Source: CEIC

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment