403

Sorry!!

Error! We're sorry, but the page you were

looking for doesn't exist.

Egypt: Reforms Picking Up Steam

(MENAFN- ING) Central bank accelerates reform process

Source: ING, Refinitiv EGP NDF shows investors welcomed the measures

Source: ING, Refinitiv Disinflation process at risk

ING, Macrobond - Lower value implies weakening of EGP; REER data as of 5 March

Source: CBE, Macrobond, ING IMF to act as reform anchor

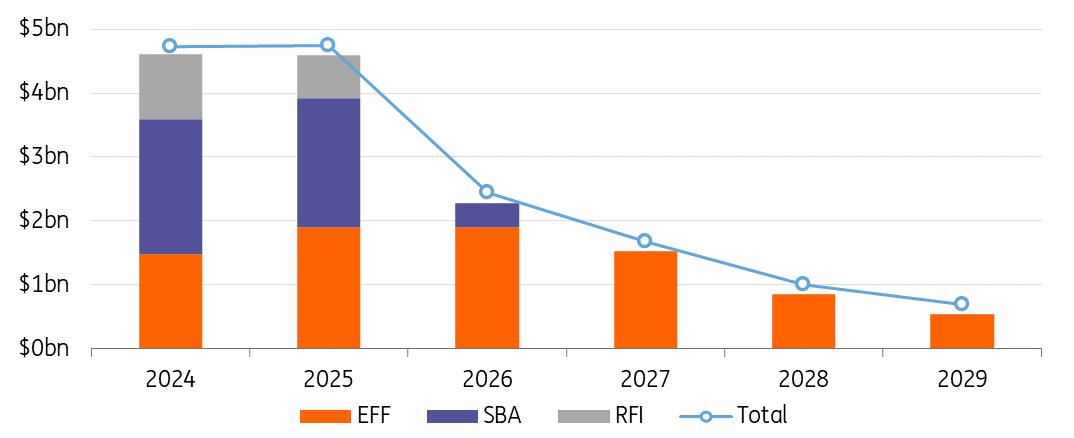

Source: IMF, Macrobond, ING; EFF = Extended Fund Facility, SBA = Stand-by Arrangement, RFI = Rapid Financing Instrument Devaluation and official flows should help correct external imbalances

Source: CBE, Macrobond, ING

Source: Egypt ministry of finance, Macrobond, ING

Source: Egypt ministry of finance, IMF, Macrobond, ING Sovereign credit spreads have rallied sharply

Source: Refinitiv, ICE, ING Our view on USD/EGP

Source: CBE, Macrobond, ING

Egypt's central bank yesterday took long-awaited measures to allow more FX flexibility, a key step in its ongoing reform process that should be seen as a positive for investors. After an unscheduled 600bp rate hike on 6 March, the authorities announced they would allow“the exchange rate to be determined by market forces”, looking to unify the official and parallel exchange rates and clear the FX backlog that has been holding back the economy. This step has been anticipated by the market for a while, but a clear trigger was the recent significant announcement of foreign investment from the UAE, including $24bn in new funds from wealth fund ADQ purchasing development rights for the region of Ras El-Hekma.

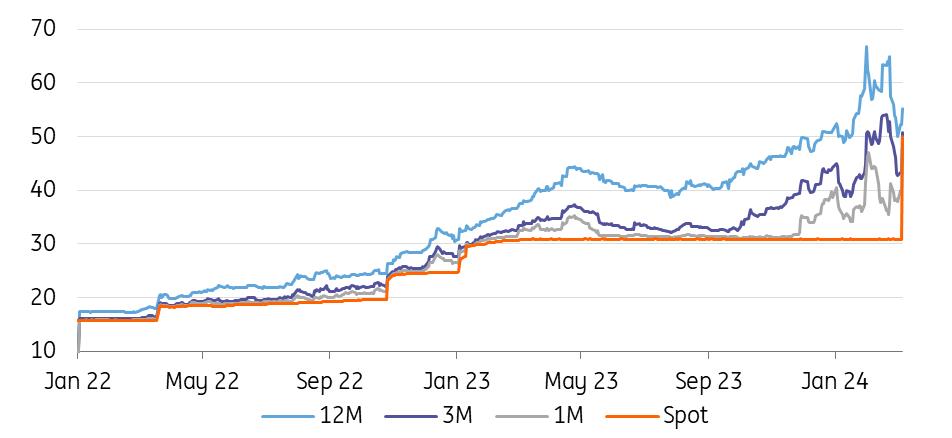

The EGP has fallen by almost 40% since the announcement versus the USD to near 50, having been held steady at around 31 since early 2023. This brings the exchange rate towards the reported parallel rate and in line with the devaluation priced in by 3-month NDF contracts, although 12-month forwards still point to investor expectations of a further weakening beyond 55 over the next year.

USD/EGP spot rate and NDFSource: ING, Refinitiv EGP NDF shows investors welcomed the measures

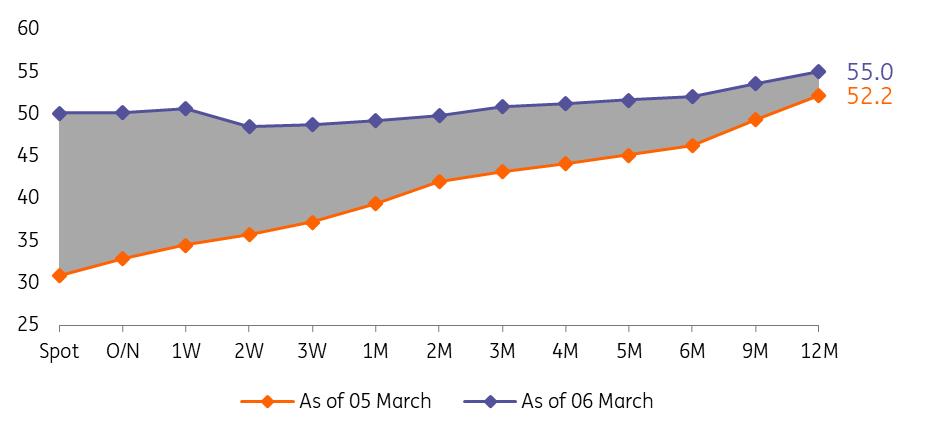

The drop in EGP to 50 against the dollar has hit global headlines, but is a mere realignment with the parallel and non-deliverable-forward market. The 12-month NDF is trading around 55, which is around 5% above its 52.2 Tuesday close and some 0% above spot, which implies relatively limited risk priced in of more sharp devaluations.

Despite the hit on the pound today, USD/EGP 12M NDF has reversed less than half of the decline (i.e. EGP appreciation) since late February, which was triggered by news of an IMF deal, and the pound is some 17% stronger than the 66.7, 31 January high in the forward tenor.

We deem markets' reaction as quite encouraging, and the EGP forward curve now signals some cautious optimism on the medium-term success of new reforms.

Investor optimism, but more work to be doneThe clear positive for investors is that there have been multiple clear and coordinated actions from Egypt to show commitment to policy orthodoxy and reform. The combination of large investment commitments from the UAE, significant interest rate hike and FX devaluation, along with an upgraded IMF agreement, could drive a virtuous cycle of improved investor sentiment and potentially more comfortable access to international bond markets. Following the central bank's policy announcement, the IMF agreed to increase Egypt's outstanding funding package from $3bn to $8bn and passed its outstanding reviews.

Yesterday's measures are far from signalling that it is job done for Egypt, however. The step FX devaluation will ideally be followed by a more free-floating exchange rate, in order to avoid Egypt getting stuck in the same cycle it has been in recent years. 2016 saw a significant devaluation and pledges to float the exchange rate, while there were also several step devaluations in 2022 before the EGP was returned to being tightly managed. This will leave some lingering scepticism for investors about a definitive shift in government policy.

USD/EGP NDF curveSource: ING, Refinitiv Disinflation process at risk

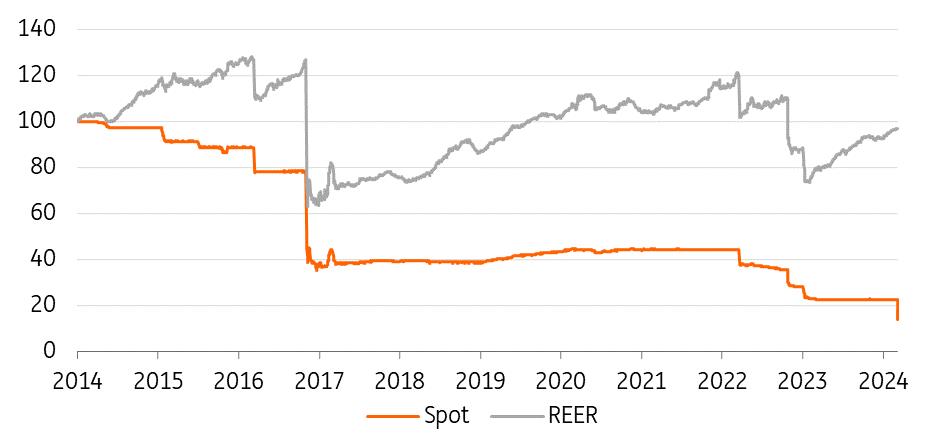

A clear issue for Egypt has been the pass-through from exchange rate weakness to spiralling inflation – this has meant that despite the significant cumulative nominal FX depreciation over the past decade, competitiveness gains as shown by the real effective exchange rate (REER) have been gradually eroded by elevated inflation.

EGP spot index and REER (Nov 2016 = 100)ING, Macrobond - Lower value implies weakening of EGP; REER data as of 5 March

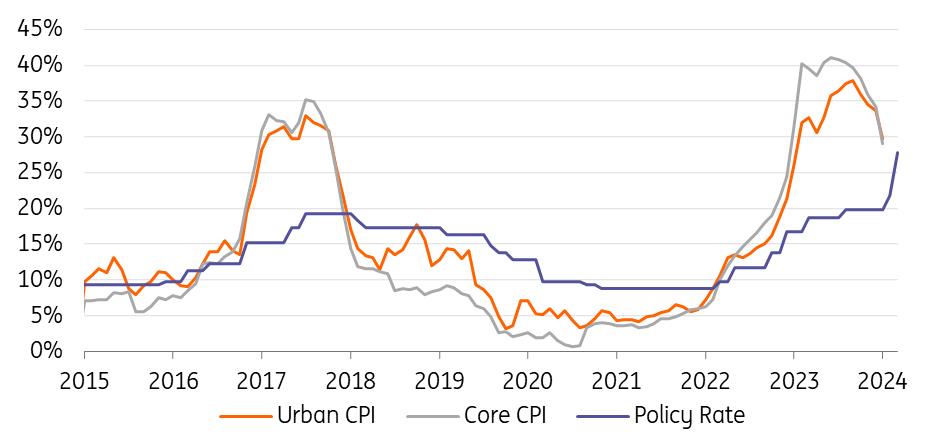

In this context, the 6 March 600bp rate hike by the central bank is a key step, and likely more aggressive than market expectations. Inflation spiked in 2017 to over 30% YoY on the back of a sharp devaluation of the EGP, while 2022 and 2023 saw an even more difficult picture, given the addition of wider global inflation pressures to the multiple step devaluations of the exchange rate. The latest FX devaluation is likely to put further inflationary pressures on Egypt, so the central bank will now be hoping for some stability in the EGP to give the chance for the cumulative effect of rate hikes to have an impact on activity and prices.

Egypt YoY inflation and policy rateSource: CBE, Macrobond, ING IMF to act as reform anchor

While the latest policy steps have been taken as a positive by investors, the IMF remains a key player for Egypt. The nation's outstanding package was marred by delays due to lack of reform progress. Egypt is already the IMF's second largest debtor, with some $15bn in repayments due over the next five years, while a $3bn agreement was reached in October 2022. Yesterday's agreed increase in the size of funding to $8bn looks important given Egypt's overall financing needs and the scale of economic challenges (including around $5 annually in Eurobond principal and interest payments over the next four years).

However, perhaps of more importance is the perception of the IMF as an anchor to keep economic reforms on track, which in turn helps to improve investor confidence, and can act as a catalyst for further foreign investment.

Egypt projected IMF repaymentsSource: IMF, Macrobond, ING; EFF = Extended Fund Facility, SBA = Stand-by Arrangement, RFI = Rapid Financing Instrument Devaluation and official flows should help correct external imbalances

Egypt's currency pressures and economic struggles were triggered by the multiple global shocks in recent years (Covid, war in Ukraine, and global interest rate hikes), but exposed some imbalances and vulnerabilities in the economy. Egypt was previously reliant on foreign investment flows into both international bonds and local currency T-bills to fund a persistent current account deficit.

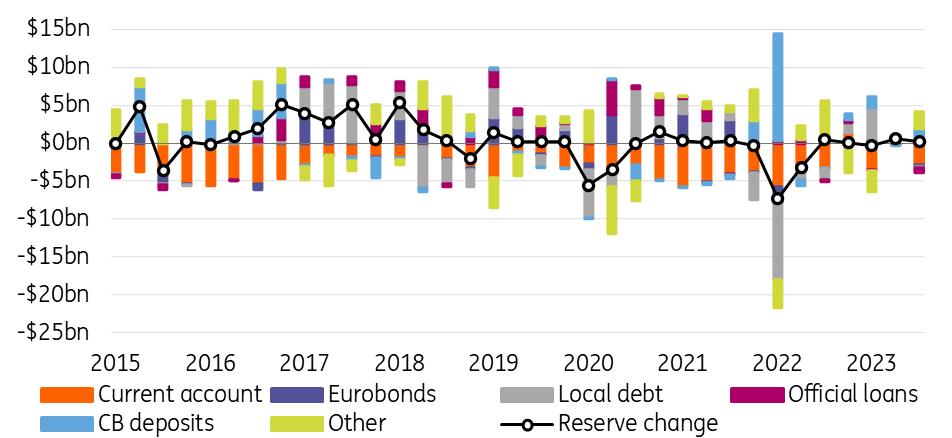

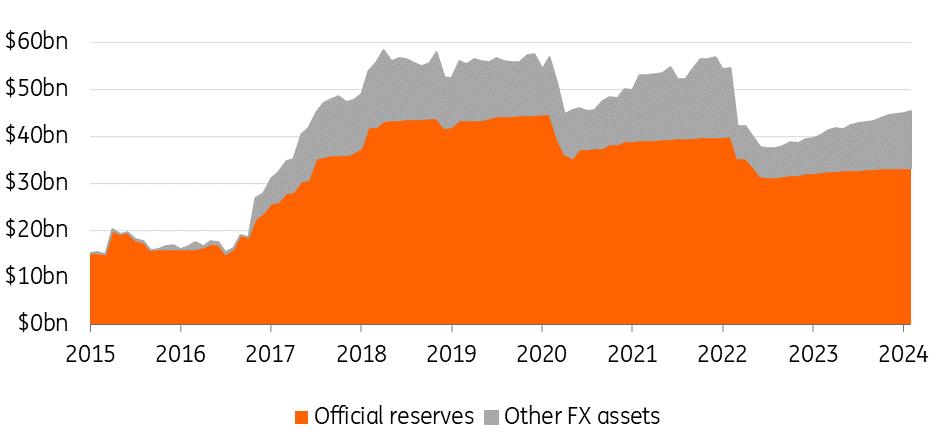

This meant that when the global risk-off environment drove investor outflows from local currency debt, and international bond markets were largely shut for issuance from riskier sovereigns, the central bank was forced to sell down a significant amount of its FX reserves to defend the currency (from a peak of $44 in February 2020 to $31 in August 2022). This raised investor concerns about the ability to continue servicing external debt and brought even sharper focus onto official flows such as IMF loans and deposits from the Gulf Cooperation Council (GCC).

Egypt quarterly balance of paymentsSource: CBE, Macrobond, ING

Egypt's current account deficit has already started to correct narrower, from 4.4% of GDP in late 2021 to nearer 1% as of third quarter 2023 as global tourism and trade and have recovered, while the latest FX devaluation is hoped to further support the adjustment in the trade balance through improved competitiveness and import compression. In this scenario, the large inflows from the IMF and UAE investment could be used to rebuild Egypt's central bank reserves and improve the nation's external balance sheet.

Geopolitical factors remain a risk for Egypt, given the reliance on transit receipts via the Red Sea and Suez Canal, along with tourism, that could be depressed by the war in Gaza. However, in this respect, Egypt's strategic importance has been reaffirmed for both regional partners such as the GCC sovereigns (especially the UAE and Saudi Arabia) and also Western nations, a clear factor in the recent commitments of support.

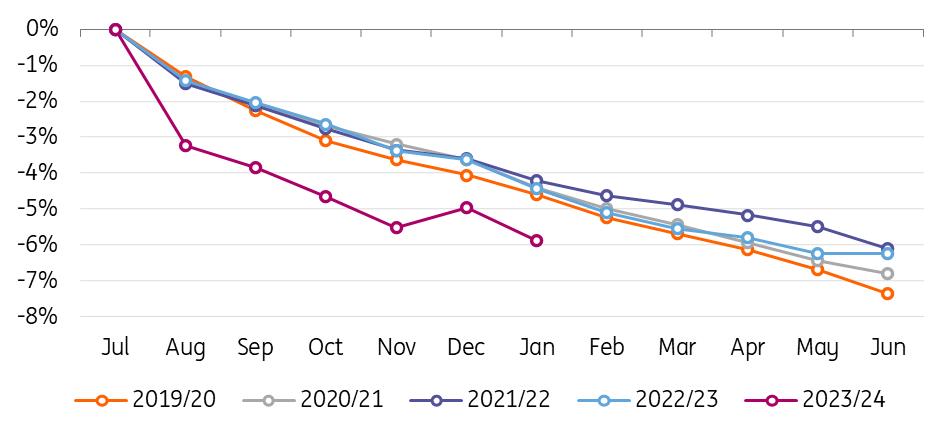

Fiscal consolidation a medium-term challengeWhile reform progress has been clear in asset privatisation, foreign investments and exchange rate policy, Egypt's fiscal situation remains difficult and could be a drag on further improvements on the nation's credit profile. The government has shown restraint in maintaining a primary surplus in recent years, but large interest payments that eat up some 40-50% of government revenues are a clear structural restraint that will be difficult to solve. The overall budget deficit is running larger on a cumulative basis this fiscal year than in previous years, touching 5.9% of GDP in January (fiscal year runs July-June).

Egypt central government cumulative budget deficit by fiscal year (% of GDP)Source: Egypt ministry of finance, Macrobond, ING

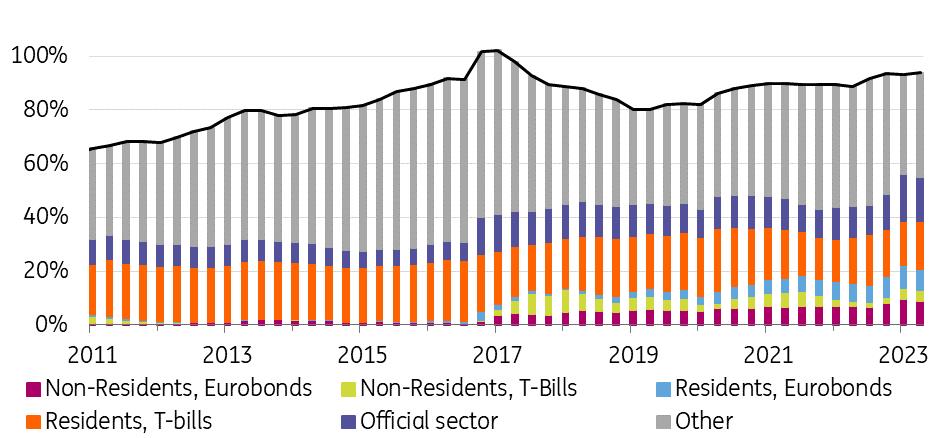

As a positive for Egypt's debt sustainability, despite a large government debt load (over 90% of GDP) and interest costs, much of this debt is held domestically, in local currency. This reduces FX risks, along with having a much more captive domestic investor base. The growing share of official sector debt will generally carry exchange rate risk, but much lower rollover risk than commercial debt. The Eurobond stock (which tends to be among the riskiest form of debt for EM sovereigns) is not insignificant, but even there a significant share is held domestically, rather than by foreign investors, which tends to mean holders are stickier, and repayment of this debt means less of a drain on FX in the system. Investors will still be looking for clear signs of fiscal consolidation and an eventual downward trend in debt-to-GDP, but near-term risks are in general lower than many high-yield sovereigns.

Egypt general government debt (% of GDP)Source: Egypt ministry of finance, IMF, Macrobond, ING Sovereign credit spreads have rallied sharply

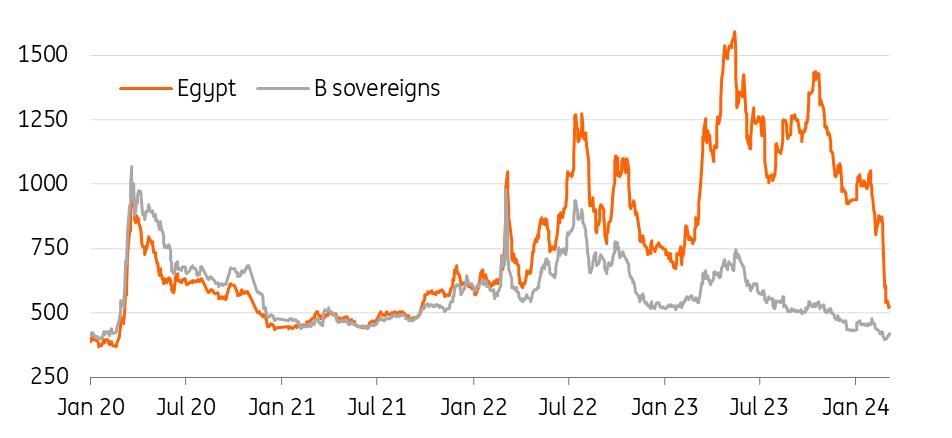

In terms of investor perception of sovereign risk, Egypt is among the top performers in the EM HC space this year, with total returns YTD over 20%, following a couple of volatile years. The recovery, in particular since late October, has seen Egypt's hard currency bonds back out of distressed territory (credit spreads over 1000bp) after serious default concerns in 2023. Current yields in the high single digits still look prohibitive to sustained Eurobond market access for the country's financing needs, so Egypt is not out of the woods yet, but the most acute phase of the crisis seems to be over.

With spread levels now compressing towards the average for single-B sovereigns and tight to some African peers, the near-term rally is likely running out of steam, in particular with most clear catalysts out of the way. For a further compression of credit spreads for Egypt, investors will likely need to see more concrete structural reforms, clearer signs of genuine FX flexibility and potential plans for future Eurobond market access.

Egypt USD sovereign bond spreads, vs single-B average (bp)Source: Refinitiv, ICE, ING Our view on USD/EGP

The situation in Egyptian markets remains volatile, although the evidence of a cautious optimism by the investors community after recent domestic developments leaves some space for USD/EGP to stabilise. The new level is significantly easier to defend by local authorities, and the short-term focus should be on stabilising around the 50 level as opposed to rushing into a further floating of the currency, especially given the ongoing risks to inflation and geopolitical events. Official reserves currently amount to USD33bn, which amounts to around four months of current account payments. We think authorities will use any appreciating pressure on the pound short-term to reinforce the reserves position.

Egypt's official reservesSource: CBE, Macrobond, ING

The transition to a more flexible market-determined exchange rate is probably on the cards later this year, but should be gradual and only occur once Egyptian authorities are comfortable this will not lead to excessive market selling pressure.

Global conditions may start to matter more once the dust has settled. Our view that the Fed will cut rates from June and for a total of 125bp this year-end implies a less stressful environment for emerging market FX and debt.

We are still far from a situation where the EGP's stellar carry is able to lure back FX flows on a sustainable basis, but we now expect Egypt to succesfully keep the currency close to the 50 mark in the coming months before a transition to free floating range potentially poses fresh downside risks on the pound.

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

- Manuka Honey Market Report 2024, Industry Growth, Size, Share, Top Compan...

- Modular Kitchen Market 2024, Industry Growth, Share, Size, Key Players An...

- Acrylamide Production Cost Analysis Report: A Comprehensive Assessment Of...

- Fish Sauce Market 2024, Industry Trends, Growth, Demand And Analysis Repo...

- Australia Foreign Exchange Market Size, Growth, Industry Demand And Forec...

- Cold Pressed Oil Market Trends 2024, Leading Companies Share, Size And Fo...

- Pasta Sauce Market 2024, Industry Growth, Share, Size, Key Players Analys...

Comments

No comment